lcd panel demand for sale

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report

Samsung Display, LG Display, Innolux Crop and AUO captured the top four revenue share spots in the LCD TV Panel market in 2015. Samsung Display dominated with 22.11 percent revenue share, followed by LG Display with 19.72 percent revenue share and Innolux Crop Display with 19.30 percent revenue share.

The global LCD TV Panel market is valued at 51130 million USD in 2020 is expected to reach 59640 million USD by the end of 2026, growing at a CAGR of 2.2% during 2021-2026.

Which are the prominent LCD TV Panel Market players across the Globe? ● Along with this survey you also get their Product Information Types (32"" and Below, 37"", 39"", 40""/42""/43"", 46""/47""48"", 50"", 55""/58"", 60"", 65"", 65""+), Applications (Residential, Commercial), and Specification. Detailed profiles of the Top major players in the industry:Samsung Display, LG Display, Innolux Crop., AUO, CSOT, BOE, Sharp, Panasonic, CEC-Panda

● LCD TV Panel Market research contains an in-depth analysis of report complete data on factors influencing demand, growth, opportunities, challenges, and restraints, and Analysis of Pre and Post COVID-19 Market.

What Overview LCD TV Panel Market Says? ● This Overview Includes Diligent Analysis of Scope, Types, Application, Sales by region, types and applications.

LCD TV Panel Market Manufacturing Cost Analysis ● This Analysis is done by considering prime elements like Key RAW Materials, Price Trends, Market Concentration Rate of Raw Materials, Proportion of Raw Materials and Labour Cost in Manufacturing Cost Structure.

The Global LCD TV Panel market is expected to rise at a considerable rate during the forecast period, between 2022 and LCD TV Panel. In 2021, the market is rising at a steady rate and with the expanding adoption of strategies by key players, the market is expected to rise over the projected horizon.

LCD TV Panel Market Report identifies various key players in the market and sheds light on their strategies and collaborations to combat competition. The comprehensive report provides a two-dimensional picture of the market. By knowing the global revenue of manufacturers, the global price of manufacturers, and the production by manufacturers during the forecast period of 2022 to LCD TV Panel, the reader can identify the footprints of manufacturers in the LCD TV Panel industry.

As well as providing an overview of successful marketing strategies, market contributions, and recent developments of leading companies, the report also offers a dashboard overview of leading companies" past and present performance. Several methodologies and analyses are used in the research report to provide in-depth and accurate information about the LCD TV Panel Market.

The current market dossier provides market growth potential, opportunities, drivers, industry-specific challenges and risks market share along with the growth rate of the global LCD TV Panel market. The report also covers monetary and exchange fluctuations, import-export trade, and global market

status in a smooth-tongued pattern. The SWOT analysis, compiled by industry experts, Industry Concentration Ratio and the latest developments for the global LCD TV Panel market share are covered in a statistical way in the form of tables and figures including graphs and charts for easy understanding.

LCD TV Panel Market Growth rate or CAGR exhibited by a market certain forecast period is calculate on the basic types, application, company profile and their impact on the market. Secondary Research Information is collected from a number of publicly available as well as paid databases. Public sources involve publications by different associations and governments, annual reports and statements of companies, white papers and research publications by recognized industry experts and renowned academia, etc. Paid data sources include third-party authentic industry databases.

Geographically, this report is segmented into several key regions, with sales, revenue, market share and growth Rate of LCD TV Panel in these regions, from 2015 to 2026, covering ● North America (United States, Canada and Mexico)

This LCD TV Panel Market Research/Analysis Report give Answers to following Questions: ● How Porter"s Five Forces model helps you to study LCD TV Panel Market?

● Which Manufacturing Technology is used for LCD TV Panel? What Developments Are Going On in That Technology? Which Trends Are Causing These Developments?

With tables and figures helping analyse worldwide Global LCD TV Panel market trends, this research provides key statistics on the state of the industry and is a valuable source of guidance and direction for companies and individuals interested in the market.

LCD TV Panel Market is 2022 Research Report on Global professional and comprehensive report on the LCD TV Panel Market. The report monitors the key trends and market drivers in the current scenario and offers on the ground insights. Top Key Players are – Samsung Display, LG Display, Innolux Crop., AUO, CSOT, BOE, Sharp, Panasonic, CEC-Panda.

Global “LCD TV Panel Market” (2022-2028) the report additionally centers around worldwide significant makers of the LCD TV Panel market with important data, such as, company profiles, segmentation information, challenges and limitations, driving factors, value, cost, income and contact data. Upstream primitive materials and hardware, coupled with downstream request examination is likewise completed. The Global LCD TV Panel market improvement patterns and marketing channels are breaking down. In conclusion, the attainability of new speculation ventures is surveyed and in general, the research ends advertised.

Global LCD TV Panel Market Report 2022 is spread across 117 pages and provides exclusive vital statistics, data, information, trends and competitive landscape details in this niche sector.

LCD displays utilize two sheets of polarizing material with a liquid crystal solution between them. An electric current passed through the liquid causes the crystals to align so that light cannot pass through them. Each crystal, therefore, is like a shutter, either allowing light to pass through or blocking the light. LCD panel is the key components of LCD display. And the price trends of LCD panel directly affect the price of liquid crystal displays. LCD panel consists of several components: Glass substrate, drive electronics, polarizers, color filters etc. Only LCD panel applied for TV will be counted in this report.

Due to the COVID-19 pandemic, the global LCD TV Panel market size is estimated to be worth USD 53490 million in 2021 and is forecast to a readjusted size of USD 53490 million by 2028 with a CAGR of 2.2% during the review period. Fully considering the economic change by this health crisis, by Size accounting for (%) of the LCD TV Panel global market in 2021, is projected to value USD million by 2028, growing at a revised (%) CAGR in the post-COVID-19 period. While by Size segment is altered to an (%) CAGR throughout this forecast period.

Global LCD TV Panel key players include Samsung Display, LG Display, Innolux Crop, AUO, CSOT, etc. Global top five manufacturers hold a share over 80%.

The global LCD TV Panel market is segmented by company, region (country), by Size and by Application. Players, stakeholders, and other participants in the global LCD TV Panel market will be able to gain the upper hand as they use the report as a powerful resource. The segmental analysis focuses on sales, revenue and forecast by region (country), by Size and by Application for the period 2017-2028.

Global LCD TV Panel market analysis and market size information is provided by regions (countries). Segment by Application, the LCD TV Panel market is segmented into United States, Europe, China, Japan, Southeast Asia, India and Rest of World. The report includes region-wise LCD TV Panel market forecast period from history 2017-2028. It also includes market size and forecast by players, by Type, and by Application segment in terms of sales and revenue for the period 2017-2028.

The report introduced the LCD TV Panel basics: definitions, classifications, applications and market overview; product specifications; manufacturing processes; cost structures, raw materials and so on. Then it analyzed the world’s main region market conditions, including the product price, profit, capacity, production, supply, demand and market growth rate and forecast etc. In the end, the report introduced new project SWOT analysis, investment feasibility analysis, and investment return analysis.

LCD TV Panel market size competitive landscape provides details and data information by players. The report offers comprehensive analysis and accurate statistics on revenue by the player for the period 2017-2021. It also offers detailed analysis supported by reliable statistics on revenue (global and regional level) by players for the period 2017-2021. Details included are company description, major business, company total revenue and the sales, revenue generated in LCD TV Panel business, the date to enter into the LCD TV Panel market, LCD TV Panel product introduction, recent developments, etc.

The report offers detailed coverage of LCD TV Panel industry and main market trends with impact of coronavirus. The market research includes historical and forecast market data, demand, application details, price trends, and company shares of the leading LCD TV Panel by geography. The report splits the market size, by volume and value, on the basis of application type and geography. Report covers the present status and the future prospects of the global LCD TV Panel market for 2017-2028.

Global LCD TV Panel Market report forecast to 2028 is a professional and comprehensive research report on the world’s major regional market conditions, focusing on the main regions (North America, Europe and Asia-Pacific) and the main countries (United States, Germany, United Kingdom, Japan, South Korea and China).

To Know How COVID-19 Pandemic Will Impact LCD TV Panel Market/Industry- Request a sample copy of the report-https://www.researchreportsworld.com/enquiry/request-covid19/21019731

The report offers exhaustive assessment of different region-wise and country-wise LCD TV Panel market such as U.S., Canada, Germany, France, U.K., Italy, Russia, China, Japan, South Korea, India, Australia, Taiwan, Indonesia, Thailand, Malaysia, Philippines, Vietnam, Mexico, Brazil, Turkey, Saudi Arabia, U.A.E, etc. Key regions covered in the report are North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

For the period 2017-2028, the report provides country-wise revenue and volume sales analysis and region-wise revenue and volume analysis of the global LCD TV Panel market. For the period 2017-2021, it provides sales (consumption) analysis and forecast of different regional markets by Application as well as by Type in terms of volume.

What are the market opportunities and threats faced by the vendors in the global LCD TV Panel market? What industrial trends, drivers, and challenges are manipulating its growth?

With tables and figures helping analyze worldwide Global LCD TV Panel market trends, this research provides key statistics on the state of the industry and is a valuable source of guidance and direction for companies and individuals interested in the market.

Well, I have a strong demand for a 32" 4K120+Hz OLED with VRR under 700$. Unfortunazely it does noz exist yet. Until then, I"m good with my 1440p144Hz VA... for 400$...

edit: since i replaced my CRT monitor where i had brightness knob and could turn black image into real invisible black I hated LCD so much because of this vomit gray shit glow black and i hate it so much to this day. i was thinking about LGs but burn in was way to common. if there was any availability of QD-OLEDs I would already had it. But in my country we have basically 2 sellers and they probably even don"t know QD-OLED exists and not even trying to get some inventory. other option is ebay but scalpers have it for 140% and shipping costs are 1/4 price of the product. i pray for the day i dont need to see vomit on my screen

LCD is basically dead unless they use the LCD Dual layering for monitors. I think there"s only been 1 TV by TCL that came out with the tech. I think its bad for TVs but could work for gaming monitors.

Amid the prolonged COVID-19 pandemic, we have all witnessed significant changes in the world around us. The trend of more people staying at home has driven demand for more home entertainment options – and central to home entertainment is the TV.

LG Display’s premium OLEDs are not the only display market to receive a boost. Since last year, LCD TV panels have also witnessed a surge in demand, representing a total reversal.

In fact, the pre-pandemic price of LCD panels had fallen so low that major display companies were considering withdrawing from the market altogether. As more people started buying LCD TVs again, this also created a supply shortage of the gate driver integrated circuits (driver ICs) needed to run LCD panels – and in turn, prices increased further.

To put this leap into perspective, the average price of 55-inch UHD LCD panels has more than doubled from the second quarter of 2020 to this year, reaching USD $222 in Q2

With similar sharp rises being seen across various LCD panel sizes, and the double whammy of demand and the driver IC shortage continuing, Omdia expects that LCD panel prices will continue to rise until the end of the year. LG Display is closely monitoring this market situation and maintaining flexibility by continuing its LCD TV panel production in South Korea.

Currently, LG Display is the only manufacturer of large OLED panels and is planning to increase shipments of its OLED TV panels from 7 million to 8 million this year in line with increasing demand.

Along with quality improvements, the company’s product lineup is also expanding. LG Display plans to mass produce new 83-inch and 42-inch OLED TV panels this year while adding medium-sized panels between 20-30 inches in the future.

It has been quite a journey then since 2013, when LG Display started shipping OLED TV panels. The number of panels shipped by the company leapt from 200,000 that first year to 4.5 million last year. A 22x increase over 7 years points to a bright future for OLED panels, especially in the COVID-19 era and beyond.

According to TrendForce"s latest panel price report, TV panel pricing is expected to arrest its fall in October after five consecutive quarters of decline and the prices of certain panel sizes may even be poised to move up. The price decline of IT panels, whether notebook panels or LCD monitor panels, has also begun showing signs of easing and overall pricing of large-size panels is developing towards bottoming out.

TrendForce indicates, with panel makers actively implementing production reduction plans, TV inventories have also experienced a period of adjustment, with pressure gradually being alleviated. At the same time, the arrival of peak sales season at year’s end has also boosted demand marginally. In particular, Chinese brands are still holding out hope for Double Eleven (Singles’ Day) Shopping Festival promotions and have begun to increase their stocking momentum in turn. Under the influence of strictly controlled utilization rate and marginally stronger demand, TV panel pricing, which are approaching the limit of material costs, is expected to halt its decline in October. Prices of panels below 75 inches (inclusive) are expected to cease their declines. The strength of demand for 32-inch products is the most obvious and prices are expected to increase by US$1. As for other sizes, it is currently understood that PO (Purchase Order) quotations given by panel manufacturers in October have are all increased by US$3~5. Currently China"s Golden Week holiday is ongoing but, after the holiday, panel manufacturers and brands are expected to wrestle with pricing. Based on prices stabilizing, whether pricing can actually be increased still depends on the intensity of demand generated by branded manufacturers for different sized products.

TrendForce observes that current demand for monitor panels is weak, and brands are poorly motivated to stock goods. At the same time, the implementation of production cuts by panel manufacturers has played a role and room for price negotiation has gradually narrowed. At present, the decline in panel pricing has slowed. Prices of small-size TN panels below 21.5 inches (inclusive) are expected to cease declining in October due to reduced supply and flat demand. As for mainstream sizes such as 23.8 and 27-inch, price declines are expected to be within US$1.5. The current demand for notebook panels is also weak and customers must still face high inventory issues and are relatively unwilling to buy panels. Panel makers are also trying to slow the decline in panel prices through their implementation of production reduction plans. Declining panel prices are currently expected to continue abating in October. Pricing for 14-inch and 15.6-inch HD TN panels are expected to drop by US$0.2~0.3, falling from a 1.8% drop in September to 0.7%, while pricing for 14-inch and 15.6-inch FHD IPS panels are expected to fall by US$1~1.2, falling from a 3.4% drop in September to 2.4%.

Compared with past instances when TV panels drove a supply/demand reversal through a sharp increase in demand and spiking prices, this current period of lagging TV panel pricing has been halted and reversed through active control of utilization rates by panel manufacturers and a slight increase in demand momentum. The basis for this break in decline and subsequent price increase is relatively weak. Therefore, in order to maintain the strength of this price backstop and eventual escalation and move towards a healthier supply/demand situation, panel manufacturers must continue to strictly and prudently control the utilization rate of TV production lines, in addition to observing whether sales performance from the forthcoming Chinese festivals beat expectations, allowing stocking momentum to continue, and laying a solid foundation for TV panels to completely escape sluggish market conditions.

The price of IT panels has also adhered to the effect of production reduction and the magnitude of its price drops has gradually eased. TrendForce believes, since the capacity for supplying IT panels is still expanding into the future, it is difficult to see declines in mainstream panel prices halt completely when demand remains weak. Even if new production capacity from Chinese panel factories is gradually completed starting from 2023, price competition in the IT panel market will intensify once products are verified by branded clients, so potential downward pressure in pricing still exists.

According to TrendForce"s latest panel price report, TV panel pricing is expected to arrest its fall in October after five consecutive quarters of decline and the prices of certain panel sizes may even be poised to move up. The price decline of IT panels, whether notebook panels or LCD monitor panels, has also begun showing signs of easing and overall pricing of large-size panels is developing towards bottoming out.

TrendForce indicates, with panel makers actively implementing production reduction plans, TV inventories have also experienced a period of adjustment, with pressure gradually being alleviated. At the same time, the arrival of peak sales season at year’s end has also boosted demand marginally. In particular, Chinese brands are still holding out hope for Double Eleven (Singles’ Day) Shopping Festival promotions and have begun to increase their stocking momentum in turn. Under the influence of strictly controlled utilization rate and marginally stronger demand, TV panel pricing, which are approaching the limit of material costs, is expected to halt its decline in October. Prices of panels below 75 inches (inclusive) are expected to cease their declines. The strength of demand for 32-inch products is the most obvious and prices are expected to increase by US$1. As for other sizes, it is currently understood that PO (Purchase Order) quotations given by panel manufacturers in October have are all increased by US$3~5. Currently China"s Golden Week holiday is ongoing but, after the holiday, panel manufacturers and brands are expected to wrestle with pricing. Based on prices stabilizing, whether pricing can actually be increased still depends on the intensity of demand generated by branded manufacturers for different sized products.

TrendForce observes that current demand for monitor panels is weak, and brands are poorly motivated to stock goods. At the same time, the implementation of production cuts by panel manufacturers has played a role and room for price negotiation has gradually narrowed. At present, the decline in panel pricing has slowed. Prices of small-size TN panels below 21.5 inches (inclusive) are expected to cease declining in October due to reduced supply and flat demand. As for mainstream sizes such as 23.8 and 27-inch, price declines are expected to be within US$1.5. The current demand for notebook panels is also weak and customers must still face high inventory issues and are relatively unwilling to buy panels. Panel makers are also trying to slow the decline in panel prices through their implementation of production reduction plans. Declining panel prices are currently expected to continue abating in October. Pricing for 14-inch and 15.6-inch HD TN panels are expected to drop by US$0.2~0.3, falling from a 1.8% drop in September to 0.7%, while pricing for 14-inch and 15.6-inch FHD IPS panels are expected to fall by US$1~1.2, falling from a 3.4% drop in September to 2.4%.

Compared with past instances when TV panels drove a supply/demand reversal through a sharp increase in demand and spiking prices, this current period of lagging TV panel pricing has been halted and reversed through active control of utilization rates by panel manufacturers and a slight increase in demand momentum. The basis for this break in decline and subsequent price increase is relatively weak. Therefore, in order to maintain the strength of this price backstop and eventual escalation and move towards a healthier supply/demand situation, panel manufacturers must continue to strictly and prudently control the utilization rate of TV production lines, in addition to observing whether sales performance from the forthcoming Chinese festivals beat expectations, allowing stocking momentum to continue, and laying a solid foundation for TV panels to completely escape sluggish market conditions.

The price of IT panels has also adhered to the effect of production reduction and the magnitude of its price drops has gradually eased. TrendForce believes, since the capacity for supplying IT panels is still expanding into the future, it is difficult to see declines in mainstream panel prices halt completely when demand remains weak. Even if new production capacity from Chinese panel factories is gradually completed starting from 2023, price competition in the IT panel market will intensify once products are verified by branded clients, so potential downward pressure in pricing still exists.

Large-area flat panel display prices increased by over 50% in 2020 due to increased demand from consumers, according to Omdia"s latest OLED and LCD Supply Demand & Equipment Tracker.

A combination of tight capacity for thin film transistor display screens, along with material and component supply bottlenecks, is fueling a panel shortfall, which is increasing demand further, as set manufacturers buy more panels to fulfill demand in 2021, according to a press release on the Omdia tracker results. In the second half of 2021, TFT supply/demand is forecast to trend above 10% almost reaching similar glut levels to 2019.

A string of accidents has created a historically tight glass market and caused an unusual industry average price increase of several percentage points, according to the press release. The lack of investment in polarizers and base films in 2019 caught the industry off guard when demand turned around in 2020. Aside from these three main components, many other materials are also in tight supply, which is affecting makers in different ways, supporting inflationary price trends.

"Although multiple caveats remain about how both supply and demand will trend over the coming months, the modeled glut level is a leading indicator that the next cycle is now on its way, which implies falling prices, utilization and profitability," Charles Annis, practice leader for display manufacturing, technology and cost at Omdia, said in the press release. "Industry players should consider the implications when planning business strategies for the next two years."

The statistic illustrates the global demand generated by the flat panel display (FPD) market from 2000 to 2020. In 2016, the flat panel display market is expected to generate revenues of 101 billion U.S. dollars worldwide.Read moreGlobal market demand for flat panel displays (FPD) from 2000 to 2020(in billion U.S. dollars)CharacteristicMarket demand in billion U.S. dollars--

IHS. (November 22, 2016). Global market demand for flat panel displays (FPD) from 2000 to 2020 (in billion U.S. dollars) [Graph]. In Statista. Retrieved January 19, 2023, from https://www.statista.com/statistics/530497/worldwide-flat-panel-display-market-demand/

IHS. "Global market demand for flat panel displays (FPD) from 2000 to 2020 (in billion U.S. dollars)." Chart. November 22, 2016. Statista. Accessed January 19, 2023. https://www.statista.com/statistics/530497/worldwide-flat-panel-display-market-demand/

IHS. (2016). Global market demand for flat panel displays (FPD) from 2000 to 2020 (in billion U.S. dollars). Statista. Statista Inc.. Accessed: January 19, 2023. https://www.statista.com/statistics/530497/worldwide-flat-panel-display-market-demand/

IHS. "Global Market Demand for Flat Panel Displays (Fpd) from 2000 to 2020 (in Billion U.S. Dollars)." Statista, Statista Inc., 22 Nov 2016, https://www.statista.com/statistics/530497/worldwide-flat-panel-display-market-demand/

IHS, Global market demand for flat panel displays (FPD) from 2000 to 2020 (in billion U.S. dollars) Statista, https://www.statista.com/statistics/530497/worldwide-flat-panel-display-market-demand/ (last visited January 19, 2023)

Global market demand for flat panel displays (FPD) from 2000 to 2020 (in billion U.S. dollars) [Graph], IHS, November 22, 2016. [Online]. Available: https://www.statista.com/statistics/530497/worldwide-flat-panel-display-market-demand/

A string of new LCD factories being built, combined with slow demand for notebook and desktop PC screens, caused LCD prices to fall during the first three months of the year, and the downward trend is expected to continue, vendors and analysts said.

Falling prices for LCD (liquid crystal display) screens should help ensure that users find bargains for new monitors, laptops and LCD TVs this year, since the screen is among the most-expensive components in those products. The price declines are also causing vendors to improve picture quality to catch users" eyes and draw them away from competitors.

Makers such as LG.Philips and Samsung Electronics, the world"s two largest LCD producers, are ramping up production at state-of-the-art factories, while rivals continue to add lines at existing plants. Other big players, such as AU Optronics in Taiwan, expect to add plants later this year, which should help keep LCD prices tame.

"The biggest impact from the new plants will be in the first part of this year, but there will be some impact throughout the year," said Frank Lee, an LCD industry analyst for Deutsche Securities Asia in Taipei.

The new LCD plants were built largely to keep pace with demand for LCD TVs, which have been among the hottest-selling items this year. Cutthroat competition among LCD makers also has been a boon to users, ensuring steadily falling prices for the past few years, as screen sizes increase.

For example, prices for 42-inch LCD screens that will be delivered to TV makers in the second half of April fell by $35 each since the end of March, to an average of $890, according to WitsView Technology Co., an industry researcher. Prices for 19-inch panels for PC monitors fell $5 to an average $160.

Average selling prices for LCD panels at AU Optronics fell nearly 12% quarter-on-quarter by the end of March, and the company forecast continued declines into the second quarter, according to executives at its first quarter earnings conference Thursday.

The company expects the price of screens used in desktops and laptops to drop by about 10% quarter-on-quarter during the April to June period, while LCD-TV screen prices will decline by a smaller percentage, in the mid single digits, it said.

LG.Philips said its sales declined in the first quarter compared to the fourth, because of a decline in the average selling prices in LCDs destined for laptops and desktop monitors, with an overall price decline of around 10% for all LCD screen products.

The company is increasing production at a state-of-the-art LCD factory in Korea, as is rival Samsung. AU is building a similar plant in Taiwan that it expects to be in production by the third quarter of this year. LG said it would produce mainly 42-inch and 47-inch screens at the plant, aimed at the LCD-TV market.

Other LCD industry competitors are also increasing production to keep up with demand for LCD-TVS. On Wednesday, S-LCD Corp., the LCD-panel manufacturing joint venture of Sony and Samsung, said it plans to invest $238 million to expand production at its factory in Tangjeong, South Korea.

SEOUL (Reuters) - South Korean flat-screen maker LG Display Co Ltd posted its second consecutive quarterly loss and cut its investment budget, as soaring inflation and a gloomy economic outlook dealt a further blow to demand for TVs and smartphones.

Revenue fell 6% to 6.8 trillion won, LG Display said in a regulatory filing. It plans to cut its 2022 investment budget by more than 1 trillion won and flexibly operate its OLED production lines to match demand.

Sluggish demand for liquid crystal display (LCD) and OLED panels, which dragged down shipments during the third quarter, is expected to continue until the second half of next year for some panels, the company said.

LCD panel prices stabilised in October thanks to production adjustment by panel makers, but LG Display is expected to extend losses into the current quarter because of weak demand, said Jeff Kim, an analyst at KB Securities.

"Under the conservative stance that poor management performance may be prolonged...we will accelerate our exit from the LCD TV sector," said LG Display Chief Financial Officer Sunghyun Kim told analysts on Wednesday, without providing an updated timeline.

LG Display has been in the red since the second quarter, when it logged its first quarterly operating loss in two years as a pandemic-driven demand boom for home entertainment devices ended abruptly amid rising inflation and interest rates.

That’s because manufacturers of large-format LCD panels used in television sets are now facing possible supply shortages at a time when TV manufacturers are making more aggressive panel orders in anticipation of stronger TV set demand this year and next.

According to market research firm Omdia’s latest market tracker reports, global top 10 TV manufacturers are anticipating a significant growth in consumer TV demand. As a result, Samsung, LG, TCL, Hisense, Skyworth, TPV, Changhong, Sony, Vestel and Konka are looking to purchase 200 million units of LCD TV panels in 2021, occupying 86% of panel makers’ supply, an increase from 70% in 2020 or 64% in 2018.

But the planned closure of South Korean LCD panel fabs and delays in the ramp up of new massive China-based LCD panel factories have wiped out a one-time panel glut.

At the same time, consumer demand for bigger and bigger TV screens is presenting a scenario that, depending on how things shake out, could result in higher-than-expected prices on new model TVs and even TV brand shakeouts in some markets, Omdia reported.

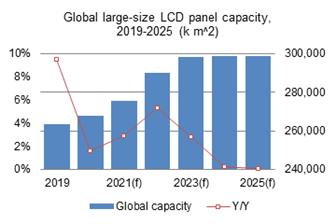

The market research firm reported demand for flat panel displays (FPDs) is set to reach 220 million meters squared in 2020, which represents more than a 4% increase in panel area demand for 2019. In Q3 2020 alone demand has risen by over 12% quarter over quarter.

Yet, delayed startups of new 8.6 and 10.5 Gen LCD fabs in China is resulting in capacity for large area FPD production only growing at a net 2% in 2020. This comes as Korean panel makers are shuttering their domestic LCD factories, reducing capacity of glass sheets produced from Gen 7 and Gen 8.5 TV panel fabs by approximately 19 million meters squared this year, the equivalent of about 31 million 43-inch TVs.

Omdia said multiple new FPD factories in China have suffered from Covid-related travel restrictions preventing foreign engineers from helping with the set-up of key equipment during the first half of 2020. Now in the fourth quarter, production is further being impacted by tight supply of Gen 10.5 glass substrates for some panel makers.

At the same time, consumer demand for larger TV screen sizes has accelerated in 2020 and is expected by the largest TV makers to continue growing after the pandemic, hopefully in 2021.

In 2020 the weighted average LCD TV size will reach 47-inches, up from 45.4-inches in 2019, Omdia said. Covid-19 has also significantly impacted FPD supply and demand in other unexpected ways throughout 2020., such as work-at-home measures resulting in stepped-up demand for tablets, notebooks, and monitors as well as TVs.

Charles Annis, displays practice leader at Omdia, commented: “Very tight supply in 3Q20 caused panel prices to rapidly rise and should help most leading FPD makers to return to profitability; a very welcome turn of the market as most have suffered consecutive losses since 1Q19.

“Currently we forecast a healthy, balanced market in 2021, where supply and demand area are both expected to grow about 6%. However, many unknowns remain on how Covid-19 will continue to impact demand, and how the improved market might encourage Korean panel makers to delay factory shutdowns and Chinese makers to expand capacity.”

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey