lcd panel price index quotation

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved January 11, 2023, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed January 11, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: January 11, 2023. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited January 11, 2023)

LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph], DSCC, January 10, 2022. [Online]. Available: https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

Recently, it was announced that the 32-inch and 43-inch panels fell by approximately USD 5 ~ USD 6 in early June, 55-inch panels fell by approximately USD 7, and 65-inch and 75-inch panels are also facing overcapacity pressure, down from USD 12 to USD 14. In order to alleviate pressure caused by price decline and inventory, panel makers are successively planning to initiate more significant production control in 3Q22. According to TrendForce’s latest research, overall LCD TV panel production capacity in 3Q22 will be reduced by 12% compared with the original planning.

As Chinese panel makers account for nearly 66% of TV panel shipments, BOE, CSOT, and HKC are industry leaders. When there is an imbalance in supply and demand, a focus on strategic direction is prioritised. According to TrendForce, TV panel production capacity of the three aforementioned companies in 3Q22 is expected to decrease by 15.8% compared with their original planning, and 2% compared with 2Q22. Taiwanese manufacturers account for nearly 20% of TV panel shipments so, under pressure from falling prices, allocation of production capacity is subject to dynamic adjustment. On the other hand, Korean factories have gradually shifted their focus to high-end products such as OLED, QDOLED, and QLED, and are backed by their own brands. However, in the face of continuing price drops, they too must maintain operations amenable to flexible production capacity adjustments.

TrendForce indicates, that in order to reflect real demand, Chinese panel makers have successively reduced production capacity. However, facing a situation in which terminal demand has not improved, it may be difficult to reverse the decline of panel pricing in June. However, as TV sizes below 55 inches (inclusive) have fallen below their cash cost in May (which is seen as the last line of defense for panel makers) and are even flirting with the cost of materials, coupled with production capacity reduction from panel makers, the price of TV panels has a chance to bottom out at the end of June and be flat in July. However, demand for large sizes above 65 inches (inclusive) originates primarily from Korean brands. Due to weak terminal demand, TV brands revising their shipment targets for this year downward, and purchase volume in 3Q22 being significantly cut down, it is difficult to see a bottom for large-size panel pricing. TrendForce expects that, optimistically, this price decline may begin to dissipate month by month starting in June but supply has yet to reach equilibrium, so the price of large sizes above 65 inches (inclusive) will continue to decline in 3Q22.

TrendForce states, as panel makers plan to reduce production significantly, the price of TV panels below 55 inches (inclusive) is expected to remain flat in 3Q22. However, panel manufacturers cutting production in the traditional peak season also means that a disappointing 2H22 peak season is a foregone conclusion and it will not be easy for panel prices to reverse. However, it cannot be ruled out, as operating pressure grows, the number and scale of manufacturers participating in production reduction will expand further and its timeframe extended, enacting more effective suppression on the supply side, so as to accumulate greater momentum for a rebound in TV panel quotations.

The service provides price quotes from market makers registered in every NASDAQ-listed and OTC Bulletin Board securities. The Level 2 window shows the bid prices and sizes on the left side and ask prices and sizes on the right side.

Level 2 provides users with depth of price information, including all the available prices that market makers and electronic communication networks (ECN) post.

Level 1 offers enough information to satisfy the needs of most investors, providing the inside or best bid and ask prices. However, active traders often prefer Level 2 because it displays the supply and demand of the price levels beyond or outside of the national best bid offer (NBBO) price. This gives the user a visual display of the price range and associated liquidity at each price level. With this information, a trader can determine entry and or exit points that assure the liquidity needed to complete the trade.

Price movement on Level 2 is not necessarily an actual reflection of the recorded trades; Level 2 is just a display of the available price and liquidity. This is an important distinction because high-frequency trading programs frequently adjust Level 2 bid and ask prices violently to shake the trees and panic onlookers despite the lack of actual executed trades. This practice is common in momentum stocks.

ECNs offer a reserve order option, which is composed of a price and display size along with the actual size. This order only shows the specific display size on Level 2 as it hides the true size of the entire order.

Hidden orders, which are an option where investors can hide large orders from the market on the ECN, function in a similar way but are invisible on Level 2. This allows for more discretion in determining prices. The best way for users to determine the status of reserve or hidden orders is to check the time and sales for trades at the indicated prices.

Important information related to market makers and institutional investors is also available in Level 2 quotes. Traders can use this information to their advantage. For example, they can gauge an institutional investor"s interest in a large stock from their order sizes and place identical orders. A similar strategy can be used with reserve orders, which are large orders broken into smaller-sized lots. Once they have identified hidden orders from L2 quotes, traders can place similar orders because institutional investor action will help support and resistance levels for that stock"s price.

There are six important columns in a Level 2 quote for a given stock. The first one is MMID. This column identifies the four-letter identification for market makers. The second column is Bid or the price that the market maker is willing to pay for that stock. The third column is Size.This column is the number of orders placed by the market maker at that size.

The remaining three columns on the right hand side are similar. The sole exception is Ask, which is the price that the market maker is willing to sell that stock price. Traders can use the difference between the bid and ask prices to determine pricing pressure and implement trading strategies.

The TFT-LCD (Flat Panel) Antitrust Litigationclass-action lawsuit regarding the worldwide conspiracy to coordinate the prices of Thin-Film Transistor-Liquid Crystal Display (TFT-LCD) panels, which are used to make laptop computers, computer monitors and televisions, between 1999 and 2006. In March 2010, Judge Susan Illston certified two nationwide classes of persons and entities that directly and indirectly purchased TFT-LCDs – for panel purchasers and purchasers of TFT-LCD integrated products; the litigation was followed by multiple suits.

TFT-LCDs are used in flat-panel televisions, laptop and computer monitors, mobile phones, personal digital assistants, semiconductors and other devices;

In mid-2006, the U.S. Department of Justice (DOJ) Antitrust Division requested FBI assistance in investigating LCD price-fixing. In December 2006, authorities in Japan, Korea, the European Union and the United States revealed a probe into alleged anti-competitive activity among LCD panel manufacturers.

The companies involved, which later became the Defendants, were Taiwanese companies AU Optronics (AUO), Chi Mei, Chunghwa Picture Tubes (Chunghwa), and HannStar; Korean companies LG Display and Samsung; and Japanese companies Hitachi, Sharp and Toshiba.cartel which took place between January 1, 1999, through December 31, 2006, and which was designed to illegally reduce competition and thus inflate prices for LCD panels. The companies exchanged information on future production planning, capacity use, pricing and other commercial conditions.European Commission concluded that the companies were aware they were violating competition rules, and took steps to conceal the venue and results of the meetings; a document by the conspirators requested everybody involved "to take care of security/confidentiality matters and to limit written communication".

This price-fixing scheme manipulated the playing field for businesses that abide by the rules, and left consumers to pay artificially higher costs for televisions, computers and other electronics.

Companies directly affected by the LCD price-fixing conspiracy, as direct victims of the cartel, were some of the largest computer, television and cellular telephone manufacturers in the world. These direct action plaintiffs included AT&T Mobility, Best Buy,Costco Wholesale Corporation, Good Guys, Kmart Corp, Motorola Mobility, Newegg, Sears, and Target Corp.Clayton Act (15 U.S.C. § 26) to prevent Defendants from violating Section 1 of the Sherman Act (15 U.S.C. § 1), as well as (b) 23 separate state-wide classes based on each state"s antitrust/consumer protection class action law.

In November 2008, LG, Chunghwa, Hitachi, Epson, and Chi Mei pleaded guilty to criminal charges of fixing prices of TFT-LCD panels sold in the U.S. and agreed to pay criminal fines (see chart).

The South Korea Fair Trade Commission launched legal proceedings as well. It concluded that the companies involved met more than once a month and more than 200 times from September 2001 to December 2006, and imposed fines on the LCD manufacturers.

Sharp Corp. pleaded guilty to three separate conspiracies to fix the prices of TFT-LCD panels sold to Dell Inc., Apple Computer Inc. and Motorola Inc., and was sentenced to pay a $120 million criminal fine,

Seven executives from Japanese and South Korean LCD companies were indicted in the U.S. Four were charged with participating as co-conspirators in the conspiracy and sentenced to prison terms – including LG"s Vice President of Monitor Sales, Chunghwa"s chairman, its chief executive officer, and its Vice President of LCD Sales – for "participating in meetings, conversations and communications in Taiwan, South Korea and the United States to discuss the prices of TFT-LCD panels; agreeing during these meetings, conversations and communications to charge prices of TFT-LCD panels at certain predetermined levels; issuing price quotations in accordance with the agreements reached; exchanging information on sales of TFT-LCD panels for the purpose of monitoring and enforcing adherence to the agreed-upon prices; and authorizing, ordering and consenting to the participation of subordinate employees in the conspiracy."

On December 8, 2010, the European Commission announced it had fined six of the LCD companies involved in a total of €648 million (Samsung Electronics received full immunity under the commission"s 2002 Leniency Notice) – LG Display, AU Optronics, Chimei, Chunghwa Picture and HannStar Display Corporation.

On July 3, 2012, a U.S. federal jury ruled that the remaining defendant, Toshiba Corporation, which denied any wrongdoing, participated in the conspiracy to fix prices of TFT-LCDs and returned a verdict in favor of the plaintiff class. Following the trial, Toshiba agreed to resolve the case by paying the class $30 million.

By default, users will receive free delayed market data for available exchanges. If needed, users can subscribe to real-time streaming market data for the prices listed in the tables below. Once a subscription is active, the delayed market data will be replaced with the real-time quotes. In addition, clients who do not need streaming real-time quotes will have the ability to request snapshot data from multiple exchanges worldwide. This request will provide a static quote for the instrument. U.S. listed equities are USD 0.01 per quote request and all other instruments are USD 0.03 per quote request. As a courtesy, accounts will receive a waiver of USD 1.00 per month for snapshot quotes. Learn more.

We provide real-time streaming market data for the prices listed in the sections below. For the exchanges which we provide, you will automatically receive free delayed market data for financial instruments for which you do not currently hold market data subscriptions.

Services are waived once the commission threshold is met for each service. Calculations for waivers are not cumulative and are applied first to the highest priced service.

The latest turn of the Crystal Cycle has been characterized by several unprecedented developments: the largest price increase from trough to peak, the longest period of rising prices and the first time TV prices increased. Now we can add another item to the list: the largest price drop in a month. LCD TV panel prices fell in September at their fastest rate ever on a percentage basis and have now lost more than half the gains that they achieved in the long up-cycle from May 2020 to June 2021.

In our summer updates, we referred to a series of events that suggested slowing demand and increasing supply, and nothing in September disrupted this outlook. The increasing panel prices have led to an unprecedented increase in TV prices in the US, which will hinder demand. After nearly a year where component shortages and logistics problems had brands and retailers scurrying to find enough supply, the brands and retailers have caught up. For developed regions, the opening of economies allows consumer spending to shift back to services, and emerging economies are still struggling with COVID and suffering an economic slowdown.

The first chart here highlights our latest TV panel price update, showing both the biggest price increases in the history of the flat panel display industry, from May 2020 to June/July 2021 and then the fastest price decreases in the industry in September 2021. While the September 2021 prices are higher than those of September 2020, they are lower than the prices of October 2020. The price increases of nine months (Oct 2020 – June 2021) have been reversed in only three.

In September, prices for all TV panel sizes fell, with the biggest percentage declines occurring for the smallest sizes. The average price decline in September across the seven sizes we track was 15.8%, and the 32” panel price declined more than 25%.

Looking at the third quarter of 2021, the average price decline is less severe than the decline at the end of the quarter would suggest. Prices declined for all panel sizes, but the biggest declines occurred for the smaller sizes. The largest size 75” LCD TV panel prices averaged over the third quarter declined by only 1.6% compared to the second quarter, but price declines for 32”, 40” and 43” exceeded 10% Q/Q.

The average for the third quarter understates the decline. Compared to prices in June 2021, all sizes of LCD TV panels have seen double-digit % declines except for 75”, which declined by “only” 9.6%. Prices of 32”, 40” and 43” panels have all fallen more than 30% from their peak.

Although we expect panel price declines to come more slowly in Q4, much of the damage has been done. Even if prices managed to stop falling and stay at September levels, the average price in Q4 would be 14% lower than the average price in Q3. With the additional price declines that we expect in Q4, we expect prices to decline by 29%, with the Q/Q price declines ranging from 19% to 37%.

As we look at pricing on an area basis, we have noted that smaller screen TVs are the most commoditized: prices for 32” panels fall the fastest during a period of oversupply and rise the fastest during a period of shortage. We see that pattern repeating again with oversupply. At the peak of the recent upswing, the smallest TV panels sold with an area premium, but the shift to oversupply has caused that pattern to flip, as shown in the next chart.

Whereas in May 2020, 75” panels sold at an area premium of $77 per square meter higher than the 32” panel price, as of July 2021, they were selling at a $56 discount on an area basis. This means that those Gen 10.5 fabs could earn higher revenues from making 32” panels than from 75” panels. The pattern for 65” is even more severe, and in June, 65” was selling at a $67 per square meter discount (alternately, a 21% area discount) compared to 32”.

In the second half of 2021, though, we are seeing 32” TV panel prices falling fastest, with a 37% decline between June and September 2021, while 75” TV panel prices have fallen only 9.6% from their mid-year peak. As of September, 32” panel prices are now at a 14% discount compared to 75”. Strangely in this period of transition, in September, the highest priced panels on an area basis were 49”/50”, priced 3% higher than 75”.

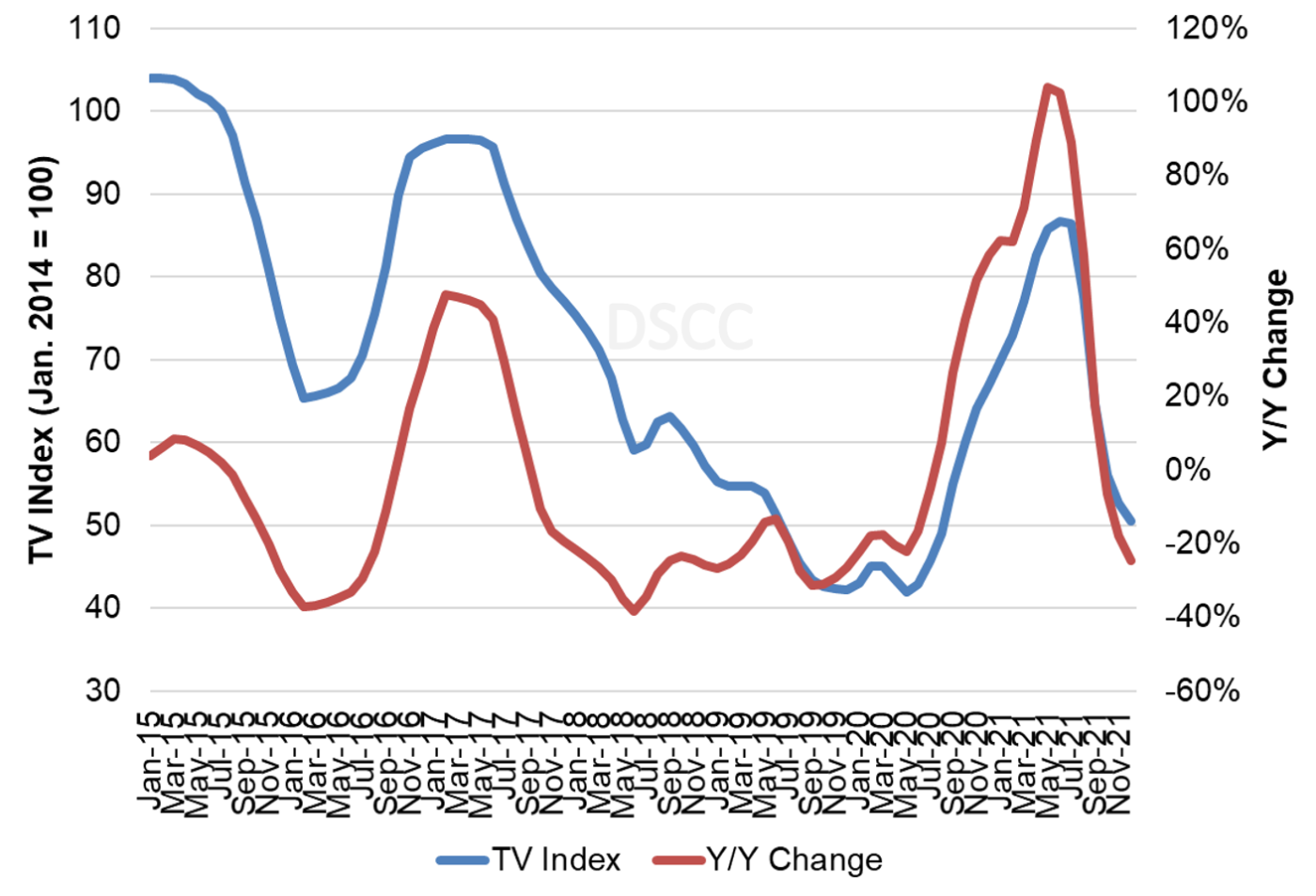

The last chart here shows our TV price index, set to 100 for prices in January 2014, and the Y/Y change of LCD TV panel prices. Our index increased from its all-time low of 42 in May 2020 to 87 in June 2021, but prices have already fallen to 65 in September. We now expect the index to decline to 50 at year-end, 25% lower than in December 2020, but still 20% higher than in May 2020. The Y/Y increase surpassed 100% in May and June 2021 but fell to +18% in September and is expected to go negative in October.

Last week, an article in Digitimesquoted Innolux President James Yang saying that LCD panel prices are expected to fall at a slower pace in the fourth quarter of 2021 and become relatively stable in the first quarter of 2022. Our forecast largely agrees with this outlook. Yang points out that power restrictions in China are likely to affect supply chains, leading to upward pressure on prices. Although our analysis of the power restrictions shows that panel makers are not directly affected (see separate article in this issue), we expect that some materials and components are likely to be constrained.

With the COVID-19 demand surge assisted by shortages in glass and DDICs, we saw a historic year of increases in panel prices, and panel makers post their most profitable quarter ever in the second quarter of 2021. The price declines in Q3 undoubtedly led to lower revenues and profit margins for flat panel display makers, but prices at their current levels remain substantially higher than costs. Even price declines in Q4 will sustain some profitability for LCD panel makers, who continue to be in line for record full-year profits.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey