semiconductor materials needed to manufacture display screens made in china

Oct 10 (Reuters) - The Biden administration published a sweeping set of export controls on Friday, including a measure to cut China off from certain semiconductor chips made anywhere in the world with U.S. equipment, vastly expanding its reach in its bid to slow Beijing"s technological and military advances.

The rules, some of which take immediate effect, build on restrictions sent in letters this year to top toolmakers KLA Corp (KLAC.O), Lam Research Corp (LRCX.O) and Applied Materials Inc (AMAT.O), effectively requiring them to halt shipments of equipment to wholly Chinese-owned factories producing advanced logic chips.

The raft of measures could amount to the biggest shift in U.S. policy toward shipping technology to China since the 1990s. If effective, they could hobble China"s chip manufacturing industry by forcing American and foreign companies that use U.S. technology to cut off support for some of China"s leading factories and chip designers.

"This will set the Chinese back years," said Jim Lewis, a technology and cybersecurity expert at the Center for Strategic and International Studies (CSIS), a Washington D.C.-based think tank, who said the policies harken back to the tough regulations of the height of the Cold War.

In a briefing with reporters on Thursday previewing the rules, senior government officials said many of the measures were aimed at preventing foreign firms from selling advanced chips to China or supplying Chinese firms with tools to make their own advanced chips. They conceded, however, that they had not secured any promises that allied nations would implement similar measures and that discussions with those nations are ongoing.

"We recognize that the unilateral controls we"re putting into place will lose effectiveness over time if other countries don"t join us," one official said. "And we risk harming U.S. technology leadership if foreign competitors are not subject to similar controls."

The expansion of U.S. powers to control exports to China of chips made with U.S. tools is based on a broadening of the so-called foreign direct product rule. It was previously expanded to give the U.S. government authority to control exports of chips made overseas to Chinese telecoms giant Huawei Technologies Co Ltd (HWT.UL) and later to stop the flow of semiconductors to Russia after its invasion of Ukraine.

On Friday, the Biden administration applied the expanded restrictions to China"s IFLYTEK, Dahua Technology, and Megvii Technology, companies added to the entity list in 2019 over allegations they aided Beijing in the suppression of its Uyghur minority group.

Eric Sayers, a defense policy expert at the American Enterprise Institute, said the move reflects a new bid by the Biden administration to contain China"s advances instead of simply seeking to level the playing field.

The Semiconductor Industry Association, which represents chipmakers, said it was studying the regulations and urged the United States to "implement the rules in a targeted way - and in collaboration with international partners - to help level the playing field."

Earlier on Friday, the United States added China"s top memory chipmaker YMTC and 30 other Chinese entities to a list of companies that U.S. officials cannot inspect, ratcheting up tensions with Beijing and starting a 60 day-clock that could trigger much tougher penalties. read more

Companies are added to the unverified list when U.S. authorities cannot complete on-site visits to determine if they can be trusted to receive sensitive U.S. technology, forcing U.S. suppliers to take greater care when shipping to them.

Under a new policy announced on Friday, if a government prevents U.S. officials from conducting site checks at companies placed on the unverified list, U.S. authorities will start the process for adding them to the entity list after 60 days.

Entity listing YMTC would escalate already-rising tensions with Beijing and force its U.S. suppliers to seek difficult-to-obtain licenses from the U.S. government before shipping them even the most low-tech items.

The new regulations will also severely restrict export of U.S. equipment to Chinese memory chip makers and formalize letters sent to Nvidia Corp (NVDA.O) and Advanced Micro Devices Inc (AMD) (AMD.O) restricting shipments to China of chips used in supercomputing systems that nations around the world rely on to develop nuclear weapons and other military technologies.

Reuters was first to report key details of the new curbs on memory chip makers, including a reprieve for foreign companies operating in China and the moves to broaden restrictions on shipments to China of technologies from KLA, Lam, Applied Materials, Nvidia and AMD.

South Korea"s industry ministry said in a statement on Saturday there would be no significant disruption to equipment supply for Samsung (005930.KS) and SK Hynix"s (000660.KS) existing chip production in China.

On Saturday, China"s foreign ministry spokesperson Mao Ning called the move an abuse of trade measures designed to reinforce the United States" "technological hegemony". read more

Technology trends in backplane technology are driving higher gas demand in display manufacturing. Specific gas requirements of process blocks are discussed, and various supply modes are reviewed.

Since its initial communalization in the 1990s, active matrix thin-film-transistor (TFT) displays have become an essential and indispensable part of modern living. They are much more than just televisions and smartphones; they are the primary communication and information portals for our day-to- day life: watches (wearables), appliances, advertising, signage, automobiles and more.

There are many similarities in the display TFT manufacturing and semiconductor device manufacturing such as the process steps (deposition, etch, cleaning, and doping), the type of gases used in these steps, and the fact that both display and semiconductor manufacturing both heavily use gases.

However, there are technology drivers and manufacturing challenges that differentiate the two. For semiconductor device manufacturing, there are technology limitations in making the device increasingly smaller. For display manufacturing, the challenge is primarily maintaining the uniformity of glass as consumers drive the demand for larger and thinner displays.

While semiconductor wafer size has maxed because of the challenges of making smaller features uniformly across the surface of the wafer, the size of the display mother glass has grown from 0.1m x 0.1m with 1.1mm thickness to 3m x 3m with 0.5mm thickness over the past 20 years due to consumer demands for larger, lighter, and more cost-effective devices.

As the display mother glass area gets bigger and bigger,so does the equipment used in the display manufacturing process and the volume of gases required. In addition, the consumer’s desire for a better viewing experience such as more vivid color, higher resolution, and lower power consumption has also driven display manufacturers to develop and commercialize active matrix organic light emitting displays (AMOLED).

In general, there are two types of displays in the market today: active matrix liquid crystal display (AMLCD) and AMOLED. In its simplicity, the fundamental components required to make up the display are the same for AMLCD and AMOLED. There are four layers of a display device (FIGURE 1): a light source, switches that are the thin-film-transistor and where the gases are mainly used, a shutter to control the color selection, and the RGB (red, green, blue) color filter.

The thin-film-transistors used for display are 2D transitional transistors, which are similar to bulk CMOS before FinFET. For the active matrix display, there is one transistor for each pixel to drive the individual RGB within the pixel. As the resolution of the display grows, the transistor size also reduces, but not to the sub-micron scale of semiconductor devices. For the 325 PPI density, the transistor size is approximately 0.0001 mm2 and for the 4K TV with 80 PPI density, the transistor size is approximately 0.001 mm2.

Technology trends TFT-LCD (thin-film-transistor liquid-crystal display) is the baseline technology. MO / White OLED (organic light emitting diode) is used for larger screens. LTPS / AMOLED is used for small / medium screens. The challenges for OLED are the effect of < 1 micron particles on yield, much higher cost compared to a-Si due to increased mask steps, and moisture impact to yield for the OLED step.

Mobility limitation (FIGURE 2) is one of the key reasons for the shift to MO and LTPS to enable better viewing experience from higher resolution, etc.

The challenge to MO is the oxidation after IGZO metalization / moisture prevention after OLED step, which decreases yield. A large volume of N2O (nitrous oxide) is required for manufacturing, which means a shift in the traditional supply mode might need to be considered.

Although AMLCD displays are still dominant in the market today, AMOLED displays are growing quickly. Currently about 25% of smartphones are made with AMOLED displays and this is expected to grow to ~40% by 2021. OLED televisions are also growing rapidly, enjoying double digit growth rate year over year. Based on IHS data, the revenue for display panels with AMOLED technol- ogies is expected to have a CAGR of 18.9% in the next five years while the AMLCD display revenue will have a -2.8% CAGR for the same period with the total display panel revenue CAGR of 2.5%. With the rapid growth of AMOLED display panels, the panel makers have accel- erated their investment in the equipment to produce AMOLED panels.

There are three types of thin-film-transistor devices for display: amorphous silicon (a-Si), low temperature polysilicon (LTPS), and metal oxide (MO), also known as transparent amorphous oxide semiconductor (TAOS). AMLCD panels typically use a-Si for lower-resolution displays and TVs while high-resolution displays use LTPS transistors, but this use is mainly limited to small and medium displays due to its higher costs and scalability limitations. AMOLED panels use LTPS and MO transistors where MO devices are typically used for TV and large displays (FIGURE 3).

This shift in technology also requires a change in the gases used in production of AMOLED panels as compared with the AMLCD panels. As shown in FIGURE 4, display manufacturing today uses a wide variety of gases.

These gases can be categorized into two types: Electronic Specialty gases (ESGs) and Electronic Bulk gases (EBGs) (FIGURE 5). Electronic Specialty gases such as silane, nitrogen trifluoride, fluorine (on-site generation), sulfur hexafluoride, ammonia, and phosphine mixtures make up 52% of the gases used in the manufacture of the displays while the Electronic Bulk gases–nitrogen, hydrogen, helium, oxygen, carbon dioxide, and argon – make up the remaining 48% of the gases used in the display manufacturing.

The key ga susage driver in the manufacturing of displays is PECVD (plasma-enhanced chemical vapor deposition), which accounts for 75% of the ESG spending, while dry etch is driving helium usage. LTPS and MO transistor production is driving nitrous oxide usage. The ESG usage for MO transistor production differs from what is shown in FIGURE 4: nitrous oxide makes up 63% of gas spend, nitrogen trifluoride 26%, silane 7%, and sulfur hexafluoride and ammonia together around 4%. Laser gases are used not only for lithography, but also for excimer laser annealing application in LTPS.

Silane: SiH4 is one of the most critical molecules in display manufacturing. It is used in conjunction with ammonia (NH3) to create the silicon nitride layer for a-Si transistor, with nitrogen (N2) to form the pre excimer laser anneal a-Si for the LTPS transistor, or with nitrous oxide (N2O) to form the silicon oxide layer of MO transistor.

Nitrogen trifluoride: NF3 is the single largest electronic material from spend and volume standpoint for a-Si and LTPS display production while being surpassed by N2O for MO production. NF3 is used for cleaning the PECVD chambers. This gas requires scalability to get the cost advantage necessary for the highly competitive market.

Nitrous oxide: Used in both LTPS and MO display production, N2O has surpassed NF3 to become the largest electronic material from spend and volume standpoint for MO production. N2O is a regional and localized product due to its low cost, making long supply chains with high logistic costs unfeasible. Averaging approximately 2 kg per 5.5 m2 of mother glass area, it requires around 240 tons per month for a typical 120K per month capacity generation 8.5 MO display production. The largest N2O compressed gas trailer can only deliver six tons of N2O each time and thus it becomes both costly and risky

Nitrogen: For a typical large display fab, N2 demand can be as high as 50,000 Nm3/hour, so an on-site generator, such as the Linde SPECTRA-N® 50,000, is a cost-effective solution that has the added benefit of an 8% reduction in CO2 (carbon dioxide) footprint over conventional nitrogen plants.

Helium: H2 is used for cooling the glass during and after processing. Manufacturers are looking at ways to decrease the usage of helium because of cost and availability issues due it being a non-renewable gas.

N2 On-site generators: Nitrogen is the largest consumed gas at the fab, and is required to be available before the first tools are brought to the fab. Like major semiconductor fabs, large display fabs require very large amounts of nitrogen, which can only be economically supplied by on-site plants.

Individual packages: Specialty gases are supplied in individual packages. For higher volume materials like silane and nitrogen trifluoride, these can be supplied in large ISO packages holding up to 10 tons. Materials with smaller requirements are packaged in standard gas cylinders.

Blended gases: Laser gases and dopants are supplied as blends of several different gases. Both the accuracy and precision of the blended products are important to maintain the display device fabrication operating within acceptable parameters.

In-fab distribution: Gas supply does not end with the delivery or production of the material of the fab. Rather, the materials are further regulated with additional filtration, purification, and on-line analysis before delivery to individual production tools.

The consumer demand for displays that offer increas- ingly vivid color, higher resolution, and lower power consumption will challenge display makers to step up the technologies they employ and to develop newer displays such as flexible and transparent displays. The transistors to support these new displays will either be LTPS and / or MO, which means the gases currently being used in these processes will continue to grow. Considering the current a-Si display production, the gas consumption per area of the glass will increase by 25% for LTPS and ~ 50% for MO productions.

To facilitate these increasing demands, display manufacturers must partner with gas suppliers to identify which can meet their technology needs, globally source electronic materials to provide customers with stable and cost- effective gas solutions, develop local sources of electronic materials, improve productivity, reduce carbon footprint, and increase energy efficiency through on-site gas plants. This is particularly true for the burgeoning China display manufacturing market, which will benefit from investing in on-site bulk gas plants and collaboration with global materials suppliers with local production facilities for high-purity gas and chemical manufacturing.

TOKYO -- China is expanding its presence in the field of key components for the electronics industry, such as liquid crystal display panels and semiconductors. In China, seven state-of-the-art LCD panel factories will come onstream over the next three years, and there has emerged a plan to construct one of the world"s largest memory chip plants.

Backed by the Chinese government"s funding power, the country seems to be trying to control the global digital industry through aggressive, massive investment despite the risk of excess facilities.

Chinese scientists on Monday revealed the discovery of a room-temperature ductile inorganic semiconductor, which is expected to serve as a new material for use in manufacturing as well as further research regarding flexible displays.

According to a paper submitted to Nature Materials by scientists from the Chinese Academy of Science, the new inorganic semiconductor, α-Ag2S, exhibits extraordinary metal-like ductility with high plastic deformation strains even at room temperature. Analysis of the chemical bounding reveals that it possesses a system of planes with relatively weak atomic interactions within the crystal structure.

“In combination with irregularly distributed silver–silver and sulfur–silver bonds due to the silver diffusion, they suppress the cleavage of the material, and thus result in unprecedented ductility. Our work opens up the possibility of a new search for ductile inorganic semiconductors/ceramics for flexible electronic devices,” the paper further noted.

Due to its promising application prospects, China has been making great effort on research and manufacture of flexible displays and new semiconductors. According to Xinhua, CSOT, a subsidiary of the Chinese smart product maker TCL Corp., started building the country"s first production line for flexible displays in 2017, which will make China a key supplier of the product often used to make bracelet-shaped mobile phones and folding tablets. The production line is located in central China’s Wuhan and costs 35 billion yuan (5 billion U.S. dollars).

The technological arms race between the United States and China has cut across everything from smartphones and cellular equipment to social media and artificial intelligence. But a new battleground is emerging that goes a layer deeper: to the components that power our smartphones, computers, automobiles and home appliances.

President Joe Biden on Tuesday signed new legislation aimed at boosting the US semiconductor industry, in an attempt to address a long-running computer chip shortage and reduce reliance on other countries, such as China, for manufacturing. Dubbed the CHIPS and Science Act, it provides incentives for domestic semiconductor manufacturing as well as research and development, including more than $50 billion in funding and additional investment in the National Science Foundation, the Department of Commerce and the National Institute of Standards and Technology.

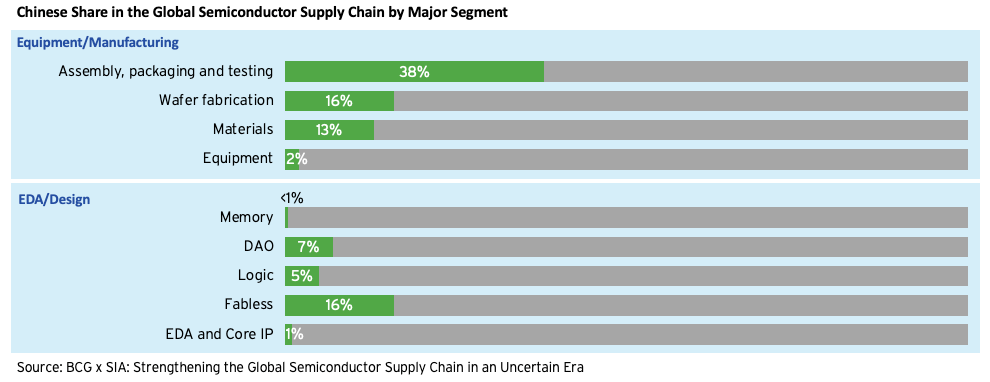

(MSFT) relying significantly on the country to make their devices and the parts that comprise them. China has also rapidlygained groundin the semiconductor market, ranking first globally in assembly, packaging and testing and fourth — ahead of the United States — in wafer fabrication, according to a recent analysis by the Center for Strategic and International Studies.

China’s increased focus on its domestic manufacturing is likely a function of US restrictions on some of its biggest semiconductor companies. China’s semiconductor sales grew more than 30% in 2020 to reach nearly $40 billion, according to figures from the Semiconductor Industry Association (SIA), a trade group whose members include IBM

But the Covid-19 pandemic caused a global shortfall in chip supply, with matters made worse this year by China’s stringent lockdowns, which stalled factories and hurt supply chains. Multiple regions are now rethinking their approach to the industry in order to become more self-sufficient and reduce exposure to Chinese manufacturing.

US Treasury Secretary Janet Yellen has repeatedly touted the importance of “friend-shoring,” or moving supply chains through US allies such as South Korea and Japan to further insulate the tech industryfrom China. European legislators, meanwhile, have proposed investments worth tens of billions of dollars over the coming years to boost the continent’s semiconductor industry.

“There’s growing global recognition that these are the technologies that will determine who ‘wins’ in the future global economy,” Kenton Thibaut, Resident China Fellow at the Atlantic Council’s Digital Forensic Research Lab in Washington DC, told CNN Business. However, she added, being completely self sufficient in chipmaking is easier said than done because of the layers of technology and specialized expertise involved. “It’s not really possible to gain a top spot in the semiconductor supply chain as a whole.”

Complicating matters further is Taiwan, the self-governed island off China’s coast that has become a diplomatic and military flashpoint between Washington and Beijing. Tensions around Taiwan, which China’s Communist Party views as its own territory despite never having controlled the island, have escalated rapidly after US Speaker of the House Nancy Pelosi’s visit there last week.

Taiwan is critical to the global semiconductor industry, with several of the world’s top manufacturers headquartered there, including Apple suppliers Foxconn and Pegatron. The biggest of those chipmakers, Taiwan Semiconductor Manufacturing Company or TSMC, accounts for an estimated 90% of the world’s super-advanced computer chips.

“Nobody can control TSMC by force,” the company’s chairman, Mark Liu, said in a recent interview with CNN. “If you take a military force or invasion, you will render TSMC factory non-operable, because this is such a sophisticated manufacturing facility [that] it depends on the real-time connection with the outside world — with Europe, with Japan, with the US.”

TSMC has already committed at least $12 billion to building a semiconductor fabrication plant in Arizona, with production expected to begin in 2024. Another Taiwanese manufacturer, GlobalWafers, recently pledged $5 billion towards building a silicon wafer plant in Texas, and South Korean conglomerates Samsung and SK Group earlier this year put forth plans to spend tens of billions of dollars to grow their US tech manufacturing presence.

TSMC’s investment predates the CHIPS and Science Act, but the legislation is likely to spur more companies to bring factories to the United States, according to Zachary Collier, an assistant professor of management at Virginia’s Radford University who specializes in risk analysis.

“It’s a very capital-intensive process to build a big manufacturing facility like this and anything that offsets some of those costs very much incentivizes the companies to bring those things onshore,” he said. The legislation earmarks nearly $53 billion over the next five years to expand US semiconductor manufacturing, including $1.5 billion for telecommunications companies that compete with Chinese firms such as Huawei. Companies that invest in semiconductor manufacturing will also get a 25% tax credit.

Even beyond the short-term incentives, companies may be keen to establish a US manufacturing presence because of the country’s relative stability, security, highly educated working class and, perhaps most importantly, sheer demand. Collier estimates that the United States accounts for a quarter of global semiconductor demand but only 12% of manufacturing. And TSMC says North America, broadly, accounts for 65% of its revenue, with China and Japan accounting for 10% and 5%, respectively.

“Right now China has an advantage in that it has a concerted strategy around pitching its technologies and supplying critical infrastructure to countries that need them,” said Thibaut. “The US and other democracies need to also develop a strategy around tech that does not just focus on competing with China, but is also proactive in providing real solutions to real needs.”

No matter how much countries try to shore up their local manufacturing bases, it will likely be virtually impossible to decouple from the global supply chain, particularly for products as integral and intricate as semiconductors. The design, fabrication, manufacturing and even raw materials for chips are distributed across several different countries and regions.

“It’s really a huge web,” said Collier, adding that no matter how much countries try to localize production, a degree of interdependence is inevitable. “It’s global, one way or the other.”

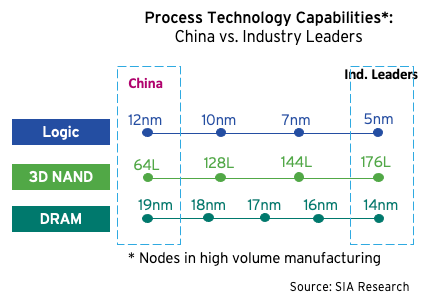

BRIEF: The Way Forward for the China Semiconductor Industry Build Out: Needs. Commitments. Collaboration. | China continues its push for mutual global collaboration in the semiconductor industry while at the same time, it will not hesitate to respond aggressively to build up its own domestic capability in response to US sanctions designed to cause economic pain and disruption to China’s efforts in the semiconductor industry worldwide. Now consuming around 70% of global semiconductor production, China is taking a lead in addressing the unprecedented pandemic-induced global shortage of chips by accelerating the development and manufacturing of 14 nm chips. At stake is enormous potential because there are huge opportunities for 14nm process chips with the rise of the 5G and AIoT arenas. Optimized chip technology within smart cities, autonomous vehicles, high-end consumer electronics, high-speed computing and remote IoT monitoring will unlock abundant long term future opportunities.

China is now ramping up mass production of 28nm chips yet late to the game and catching up fast regarding the focus and commitment to a 14nm technology rollout by 2022. And underpinning the entire effort is the need for China’s chip manufacturers to continue building up the required investment, manpower and active collaboration with its domestic semiconductor supply chain.

“Many of the technical problems associated with the development and production 14nm chipsets and which cover the entire integrated circuit industrial chain system in China, have already been overcome, and progress is clear to see.”Dr. Wen Xiaojun, Deputy Director at China’s Electronics and Information Industry Development Research Institute (CCID)

“...semiconductors are highly complex products to design and manufacture, and they require a massive investment in R&D and capital expenditure. This has resulted in a highly specialized global supply chain where every region plays a different role based on their own strengths. This collaboration has helped pave the way for nonstop innovation and lower costs, benefiting companies and consumers worldwide.”

In other words, the messaging coming from China’s ministry of communications and companies like Huawei are unsurprisingly consistent; Xi Jin Ping has made China’s intentions for mutually beneficial global cooperation crystal clear. There is no debt trap diplomacy. There is no vaccine diplomacy. There is only China’s effort and commitment in cooperating with other countries on a basis of respect and straight up reasonable bilateral economic deal-making without attaching the export of its own country’s ideologies. At the same time, there is an aggressive and much needed response to the nagging little problem of the aggressive stance and sanctions within the semiconductor industry steadily flowing outward from the current Biden administration of the United States.

Regardless of whether the aggressive U.S. position is rooted in irrefutable evidence or vacuous rhetorical allegations, the aggressive U.S. stance, messaging and sanctions are here to stay and lead to important questions.

With China ramping up its domestic semiconductor manufacturing capability, what purpose does the on-going US sanctions still serve and at what cost to stakeholders around the world including the United States itself?

Where does the current situation fit with respect to global semiconductor supply chain collaboration especially considering the EU member states who recently signed the Joint Declaration on Processors and Semiconductor Technologies?

The aggressive U.S. position in its efforts to block China’s progress and capability is unmistakable. I point it out to show the reader how the U.S. position remains in diametrically opposed contrast to the messages expressed by both the Chinese government and Huawei Technologies who remain clearly in favor of greater global collaboration amongst all nations large and small. Huawei’s message is crystal clear, reiterating the importance of global collaboration in chip manufacturing for several reasons which fit the interests of all parties involved across every region of the global supply chain to benefit both companies and consumers by paving the way for nonstop innovation and lower costs, as Chairman Xu noted.

As China moves forward to claim its self-sufficiency in the global semiconductor industry, industry analysts clearly recognize the needed technology milestones. In learning that smaller 5nm, 7nm, 10nm and 12nm chip sales are a far smaller market share, we also quickly recognize the wisdom of China’s commitment to the far more widely used 14nm chipsets. According to Christopher Taylor, Director, RF and Wireless at Strategy Analytics, more than 95% of the market is at 14nm and above. In addition, China’s commitment to self-reliance will also help address the global chip shortage and accompanying rise in prices hampering the global economy in numerous ways which is set to persist thanks to continued demand plus panic stockpiling in chipsets worldwide.

“China needs not just to fabricate the chips, but they also need to design software and equipment without having to rely on other countries for those. China has to approximately double its production of semiconductors for its own consumption from 15% of its needs to 30% to lessen the effect of supply disruptions and production of electronics,” Christopher Taylor, Director, RF and Wireless at Strategy Analytics

China currently imports $300 billion worth of semiconductor chips, clearly indicating its reliance on chip imports. Yet at the same time, let’s consider recent indicators that China is not sitting still in developing its self-sufficiency. According to SIA’s (Semiconductor Industry Association) 2021 white paper, “Earlier this year, China landed a rover on Mars. Chinese state media reported that inside both China’s space station and the Mars rover were 100% indigenously designed-and-produced semiconductors, signaling China’s increasingly sophisticated microchip capabilities. ...while China has mastered some chip technologies, its commercial semiconductor industry is still relatively nascent.” Still, the Chinese government is making serious efforts to close the gap, investing well over $150 billion from 2014 through 2030 in semiconductors.”

There is far more to the story which clearly reveals the breadth and depth of China’s commitment and wise focus on a future which is centered around the 14nm chipset. President Xi Jinping has injected billions into China"s chip industry and just in 2020, an astounding 22,000 semiconductor companies were created while in 2021, an additional 15,000 plus have registered as well. According to industry leading analyst and news provider Total Telecom, China’s “plans to mass produce 14 nm chips next year (2022) within the country is likely to make China the biggest semiconductor supplier globally.”

Further thoughts from Strategy Analytics’ Christopher Taylor indicate the road map of China’s plans will unfold in coming months and years. We begin by noting that by Q4 of this year, China’s Shanghai MicroElectronics company will have 28nm machines, the equivalent of ASML’s 1980Di machines. Taylor then surmises that with multiple patterning capability, more advanced versions of the machine capable of 7nm chips will be a reality.

While we can’t forget that the U.S. took steps to effectively shut China out of access to needed semiconductor fabrication tools, the setback has not stopped companies such as China’s SMIC to continue its development of both 14nm and 12nm process nodes based on fin field-effect transistor (FinFET) technology. This is accomplished by using mature deep ultraviolet lithography toolsets and processes used in the majority of existing semiconductor production today. That analysis is according to market intelligence provider & analyst firm CCS Insights. SMIC’s CEO Zhao Haijun has increased spending by another $1.1 billion to a total of $4.3 billion, focused on chip demand in communications and automotive applications.

"While the Chinese government support is central to driving the industry’s direction, CCS Insights has stated, “China’s ability to create a vibrant and healthy semiconductor industry is still a very tangible possibility, with or without government support.”CCS Insights

Even China Mobile, the world’s largest wireless operator, has created its own chipmaking business to address the need for chipsets related to IoT applications.

While the global semiconductor manufacturing industry has certainly split very much in line with the geopolitical influences of the day, at the root of China’s expansion plans we find economic reality; a relentless demand for 14nm chips based on existing process technologies which China is now boldly stepping into and expected to become a major player.

As is known, because of alleged concerns over China’s military gaining access to chip technology, the United States admits any ties to the Chinese government are unclear and unproven, yet persists in its aggressive position to block China’s ambitions. The majority of pundits are willing to associate this competition as competition between autocracies and democracies even including the alleged systemic degradation of human rights which will occur in China’s chip-driven data rich smart cities. The excess rhetoric of concern has gone so far as to include a recent U.S. military commander warning that China might actually invade Taiwan to gain control of Taiwan-based TSMC. Within this rather dramatic geopolitical backdrop, the United States has seen fit to implement semiconductor industry sanctions limiting China’s access to the world chip markets.

The US sanctions not only brought challenges to Chinese companies, but also caused a ripple effect on the whole ecosystem and damages throughout the supply chain, including the US semiconductor industry.

The recent EU Member States Joint Declaration on Processors and Semiconductor Technologies was created and signed by member states to bolster across Europe’s electronics and embedded systems value chain stated as, “This Declaration aims at creating synergies among national research and investment initiatives and ensuring a coherent European approach of sufficient scale. It builds on and will expand collective efforts, including the future KDT and EuroHPC Joint Undertakings, the European Processor Initiative and the existing IPCEI on microelectronics.”

Such ambitions for EU semiconductor industry self-sufficiency point to the current weaknesses in the industry foundation and immediately lead to the opportunity presented to the EU by Chinese enterprise’s call for greater collaboration together. Currently, there is a understood lack of industry foundation whereby little semiconductor industry manufacturing takes place in the EU. During a recent August 2021 Delphi Economic Forum, Remco Zwetsloot, Research Fellow with Georgetown’s Center for Security and Emerging technology expressed the narrative that there is no single EU country which could contain all the parts of the semiconductor industry supply chain efficiencies which are needed. Zwetsloot noted that while the specific strengths exist such as with Netherland’s ASML and other German wafer technology firms, the EU cannot become independent manufacturing-wise in any meaningful sense because the manufacturing foundation is simply not there.

In identifying a weakness, we also identify an opportunity. Even today, as a stand alone semiconductor market supplier, the EU is far behind China’s industry chain capability.

Collaboration between China and the EU will incubate a thriving semiconductor industry and is clearly calling for such collaboration at this time. Stepping forward together would directly address a number of pressing mutual interests and needs including effectively addressing the global chip shortage all stakeholders are impacted by. The EU’s commitment to ramp up its semiconductor manufacturing capability meets the rising demand for semiconductors in the China market with companies ready to diversify their supply chains while collaboration with Chinese enterprises will very much make it possible for the EU to better meet that demand.

At the same time, the EU member states remain side by side with China understandably wary of the current U.S. posture, knowing that new U.S. initiatives and sanctions against China further disrupting the semiconductor industry, rational or otherwise, may be suddenly made public at any moment as the battle for control continues. By collaborating with China, the EU will be protecting and building its own interests very much in line with its recent EU Member States Joint Declaration on Processors and Semiconductor Technologies

Circling back around to our question, “What purpose does the on-going US sanctions still serve and at what cost to stakeholders around the world including the United States itself?”, we must consider true underlying intent. While unsettling, there are those who suggest that the U.S. intent is pointedly to create industry disruption and chaos, creating a damaging economic disruption and technology gap so as to allow itself to sweep in and gain a grip on market share and maintain control of the US dependency within the supply chain. Ongoing U.S. sanctions continue to blunt China’s efforts yet are having the unintended impact of disrupting the industry across the entire globe.

Facing such pressures, China’s national imperative to aggressively expand its semiconductor industry will only continue and accelerate with the role of the Chinese government in supporting its domestic semiconductor industry an unmistakable force. As noted by SIA’s white paper, “In China’s newly released 14th Five-Year Plan, semiconductors were explicitly identified as a strategic technology priority requiring a whole-of-society effort.” Such initiatives include preferential tax policies valued as much as $20 billion to semiconductor manufacturers. Furthermore, a recent study indicated that the move toward decoupling would actually cause a variety of damage to US markets. How is it possible the U.S. government administration pushing China sanctions is not aware of the danger of shooting itself in the foot?

Analysts are perplexed by the absence of a more reasonable U.S. strategy leading to the threat of even further demise in the number of American chip firms. This then undoubtedly leads to significant reductions to R&D and capital expenditures, estimates of well over 100,000 additional U.S. job losses and an obvious reduction in U.S. competitiveness.

Continuing U.S. sanctions seem a paradoxically brute force replacement for working with allies and China to collaboratively develop fresh rules and standards across the global supply chain ensuring fair market access and competition for all industry players. Brute force export controls aimed at China are having the opposite effect of damaging the U.S. position rather than more targeted, reasoned multilateral export controls which do not stifle the collective innovative capabilities found and more essential than ever within the intertwined global semiconductor industry and supply chains. Ultimately, the needs of the marketplace across the globe, the commitments declared and pursued by both the EU and China to step up their semiconductor industry capability sends a clear message to the U.S. that mutual collaboration and diplomatic cooperation may be a far better choice than its current negative, aggressive stance.

China will likely take the lead in the semiconductor display sector across the world within the next three to five years, said Li Dongsheng, the founder and chairman of Chinese consumer electronics giant TCL Corp.

"China will play an active and vital role in prompting the development of the semiconductor display industry, which has a high entry threshold and needs high investment," Li said, while noting China has the best chance of making a breakthrough in this field and expressing confidence in the prospects of the high-tech industry.

Li made the remarks at the IFA, the world"s leading trade show for consumer electronics and home appliances, being held in Berlin, Germany, from Sept 6 to 11.

A traditional home appliance giant, TCL announced strategic adjustments in the company. Its consumer electronics, home appliance and terminals businesses will be split off from the listed company, as the firm shifts its focus to the semiconductor display sector.

Li noted that more than half of the display screens manufactured by Shenzhen China Star Optoelectronics Technology Co Ltd (CSOT), a subsidiary of TCL, were sold overseas.

TCL has ramped up its efforts in the research and development sector in Europe. It set up an R&D center in Poland, with a focus on artificial intelligence research, and poured resources into the next-generation semiconductor display technology such as flexible displays, Li said.

TCL Industrial Holdings Co Ltd CEO Wang Cheng said the company"s first 5G smartphone is being developed and will be launched in the first half of next year in Europe. Its foldable handset is also expected to hit the market in 2020.

"5G has many application scenarios, as we can see that 5G has big opportunities in ultra-high-definition signal transmission," Wang noted. For instance, 5G could be combined with 8K displays, virtual reality and augmented reality."

Globally, TCL posted robust growth last year. Its overall liquid crystal display or LCD TV sales volume rose 23.1 percent year-on-year to 28.61 million sets worldwide, the company said.

The company has also invested in flexible AMOLED or active matrix/organic light-emitting diode technology display panels, which are used for high-end mobile phones and wearable devices.

Liang Zhenpeng, an independent consumer electronics analyst, said TCL is among a handful of TV makers such as Samsung and LG that have mastered the key technologies in upstream display panel manufacturing. This allows it to take the initiative in a fiercely competitive market.

China is expected to replace South Korea as the world"s largest flat-panel display producer in 2019, a report from the China Video Industry Association and the China Optics and Optoelectronics Manufacturers Association said.

ACM Research was founded in 1998 by Dr. David Wang focused on developing and selling stress-free copper polishing tools which were positioned as a competitor to chemical metal planarization (CMP). ACM Research’s (advanced copper materials) initial copper polishing tool did not find any success, but the company was able to sidestep the rocky beginnings and stay afloat due to their strong backing. The firm then pivoted and shifted focus to another area of the semiconductor capital equipment market, wafer cleaning.

At first glance, the wafer cleaning market sounds relatively simple, but that is deceptive. The cleanliness and purity levels required to continue the next step of semiconductor manufacturing cannot be understated. There are dozens of different cleaning steps involved in manufacturing a wafer and the target is an extremely fragile material. Patterns and features can easily collapse. For example, in 3D NAND, holes can be less than 1/20th the thickness of a human of a human hair. These holes are etched straight down with an aspect ratio of >25:1. Cleaning everything out of these holes is incredibly difficult. As FinFET transistors are formed, the various steps in the middle are even more difficult to clean. With gate all around nanosheets, the complexity of cleaning ramps even further.

Despite this, ACM Research has been able to carve a niche in the wafer cleaning business competing with multi-billion-dollar revenue companies such as Japan’s Screen and Tokyo Electron as well as the US based Lam Research. Furthermore, they have begun to expand upstream to electro-chemical plating and etch products as well. ACM Research achieved over $250M revenue in 2021 and has guided to hit as high as $405M this year. While most these sales are in China, ACM Research also has significant sales to Korea’s SK Hynix and is even qualifying at Intel as we speak!

Back to the history of ACM Research, after continuing to be funded by their backers despite their initial misstep with copper polishing tools, they opened a research facility in Shanghai. This was the start of their overt operation in China. If we fast forward to the present day, ACM Research’s research and development as well as production are all in China. There is a tiny amount of R&D in South Korea as well and a corporate “HQ” in California. All meaningful operations related to technology development and manufacturing are in China.

ACM Research’s first major customer was SK Hynix. SK Hynix opened a DRAM fabrication facility in Wuxi City, China after being wooed by large subsidies. It was SK Hynix’s first 300mm wafer fabrication facility and the site continues to receive large investments and subsidies to this day. This facility in China began to evaluate ACM Research’s tools and eventually they began to place orders at the turn of the decade. ACM Research first struck gold at SK Hynix with their SAPS single wafer cleaning tools.

The wafer fabrication industry was transitioning from batch wafer cleaning tools to single wafer cleaning tools. Batch wafer cleaning tools would dunk many wafers into a bath of circulating water or chemicals. As feature sizes shank, this was insufficient for the increased levels of cleanliness and purity that Moore’s law demanded. Single wafer cleaning tools would instead spray fluids (acids or ultra-pure water) through nozzles directly onto the wafer as it spins at high RPM.Here’s a videofor those of you who need a visualization. Japan’s Screen first introduced rotating single wafer cleaning systems in 1983, but mass popularity of this type of tool took longer. Screen is still the leader in rotating single wafer cleaning due to their precise control and engineering around throughput, various nozzles types, chemical handling, minimization of waste chemicals, temperature uniformity, and humidity control.

The ACM Research SAPS wafer cleaning tool is a single wafer cleaning tool, but with a key innovation. It utilized megasonic acoustic vibrations through the fluid bath to produce bubble oscillations which assisted with cleaning defects. Other manufacturers had introduced megasonics in the past, but a key issue was that as bubbles collapse, the resulting energy would often damage features on the chip. ACM Research also introduced space alternate phase shift (SAPS) which alternated the phases of the megasonic waves so that the energy delivered to the wafer was uniform and caused less pattern damage. Even with these innovations, SAPS is not currently used in any leading edge FinFET process by Samsung, Intel, or TSMC due to pattern collapse. ACM Research also has a similar technology known as TEBO (Timely Energized Bubble Oscillation) which has seen success in SK Hynix and YMTC NAND processes.

The state funded and subsidizedYangtze Memory Technology Corporationis the largest customer for ACM Research, but other Chinese state enterprises such as SMIC, HLMC, and CXMT are large customers as well. All of these firms have been proven to be directly working with the CCP for funding, research, and use of their chips in military applications. Much of these firms technology comes from American based companies too. For example,YMTCrelies primarily of Lam Research tools for the fabrication of 3D NAND and San Jose based Xperi Corporation for Hybrid Bonding technology which YMTC has dubbed as “XStacking.” ACM Research has published papers with YMTC regarding wafer cleaning for hybrid bonding as well. This could be an area where ACM Research and YMTC leapfrog Korean, Japanese, and American companies.

ACM Research is not only seeing success in wafer cleaning. They also have wins at packaging firms. The most notable win is with Tongfu Microelectronics who has been purchasing electro-chemical plating tools from ACM Research. As a reminder, Tongfu has a joint venture with AMD where AMD’s Epyc datacenter CPUs as well as client CPUs are packaged by Tongfu. Chips from the AMD Tongfu joint venture have even been shipped into theworld’s fastest supercomputer, Frontier, which was built by the US Department of Energy.

The ACM Research electro chemical plating tool primarily competes withLam Research’s Sabre 3D tools.This tool could potentially cause Lam Research to lose a large amount share as a large portion of electroplating for packaging applications is done in China.

While ACM Research argues they have unique differentiated tech, the vast majority of their sales come from the Chinese domestic market. They are subsidized, preferred as a domestic supplier, and undercut the competing products of Screen, Tokyo Electron, and Lam Research on price. The assumptions of market share in China is very high as a result. As long as ACM Research’s product is even somewhat close to foreign competitors, the domestic supplier status means they will win out in share. This is further emphasized by ACM Research’s own long-term estimates forecasting little to no sales for the rest of the world outside of mainland China.

ACM Research’s own presentations showcase they believe 42% of new semiconductor production facilities are in China. This lines up with SEMI World Fab Report andour own data. The top country in semiconductors has shifted every few decades, and ACM Research, much like the CCP, believes that the next decade will be China’s turn despite renewed initiative looking to level the playing field on subsidies from Taiwan, South Korea, Japan, Europe, and the US.

We were shocked when we learned that when ACM Research says “evaluations in process with major U.S. manufacturer,” they mean Intel. The same Intel that is currently begging the United States and European governments for subsidies due to East Asian dominance in the semiconductor industry. We confirmed with multiple sources including directly with ACM Research that Intel is in the process of qualifying an ACMR tool which was made in China for the Intel Oregon campus. The Oregon campus is subsidized by Oregon tax payers, so we wonder how these tax payers would feel if they knew they were helping pay for wafer fabrication equipment from China. Once qualified, it is very possible that Intel could utilize Chips Act government subsidies to import more tools into Oregon, Arizona, and Ohio for volume production despite the existence of Japanese and American alternatives.

ACM Research is projecting as much as $405M in revenue this year and they aren’t slowing down. They have begun to introduce photoresist stripping, CVD, and ALD products to compete more with Lam Research, Tokyo Electron, and Applied Materials. If successful, this would bust open a $30B sector of the wafer fabrication equipment market.

In economic terms, this argument makes a lot of sense. But geopolitics matter, too. Political leaders in other countries have already decided to offer subsidies for semiconductor manufacturing, because they want some of this manufacturing to take place in their countries.

If the U.S. does not also offer subsidies, it may continue to struggle to attract factories. Already, the U.S. market share of all semiconductor manufacturing has fallen to about 12 percent from 37 percent three decades ago.

Pat Gelsinger, the chief executive of Intel, has said that a typical factory costs about $10 billion to build, and subsidies from some countries cover 30 percent to 50 percent of that cost. China’s subsidies cover closer to 70 percent. “It is not economically viable for us to compete in the world market if everyone else that we’re competing with is seeing 30 to 50 percent lower cost structures,” Gelsinger said.

Senator Rob Portman, an Ohio Republican who helped write the Senate bill, has acknowledged that it runs counter to the free-market philosophy he usually prefers. But, Portman explained at the Aspen Ideas Festival last month, “if we are continuing with blinders on to follow a political philosophy that seems to make sense generally but doesn’t work in the practical world, I think we end up with a much less competitive economy and a national security risk.”

Biden and his top aides agree. “We are now in a very dangerous situation in which we are utterly reliant on Taiwan for the vast, vast majority of our most advanced semiconductors, which are the exact kind of semiconductors you need for military equipment,” Commerce Secretary Gina Raimondo told me. “You cannot be a global superpower if you don’t make any of these.”

House Democrats added provisions to the Senate bill that Republicans did not like, such as additional money for worker retraining. House Democratic leaders seem willing to remove most of these from the final bill, but it remains unclear whether the two parties can agree on a compromise.

McConnell — despite being one of 19 Senate Republicans who voted for the original bill — also appears to be wavering. He sent a tweet on June 30 suggesting that he might block a semiconductor bill if Democrats continued trying to pass a separate bill, on climate change and drug prices, that Republicans oppose.

“Semiconductors are arguably humanity’s greatest achievement to date,” says Jimmy Goodrich, vice president of global policy at the Semiconductor Industry Association,a trade group based in Washington, DC. “They’re still central to everything that’s modern or electronic, whether you’re driving a car, or surfing the internet, or using a supercomputer—everything is ultimately based on a semiconductor, and lots of them.”

While we often hear about the internet or software companies that are wielding more and more influence over society, those companies make their breakthroughs off the advancements of chip makers. Simply put, innovation in semiconductors leads to innovative products.

Third, a small but critical portion of the semiconductor industry has specific applications in the defense sector, for use in things like missiles and radars. Mastery of the semiconductor technology can help ensure that a country’s military technology remains at the cutting edge.

As a result of these factors, dominance of the chip industry can give governments amazing political leverage over other countries. There’s no better example of this than when the US Department of Commerce ordered a

Mark Li, who researches China’s semiconductor industry at Sanford C. Bernstein, says that the ZTE incident likely heightened the sense of urgency felt by policy makers in Beijing to ramp up the country’s semiconductor prowess. “They need to make their own chips, so their companies can function without imported chips,” he says.

The semiconductor industry remains one of the few manufacturing-driven sectors where the US remains the global leader. After Texas Instruments’ Jack Kilby invented the integrated circuit in 1958, the US military embraced the technology as the Cold War ramped up, and consumer electronics companies later followed once the personal computer hit the market. Most of the fabrication for the country’s largest integrated circuit makers takes place within the

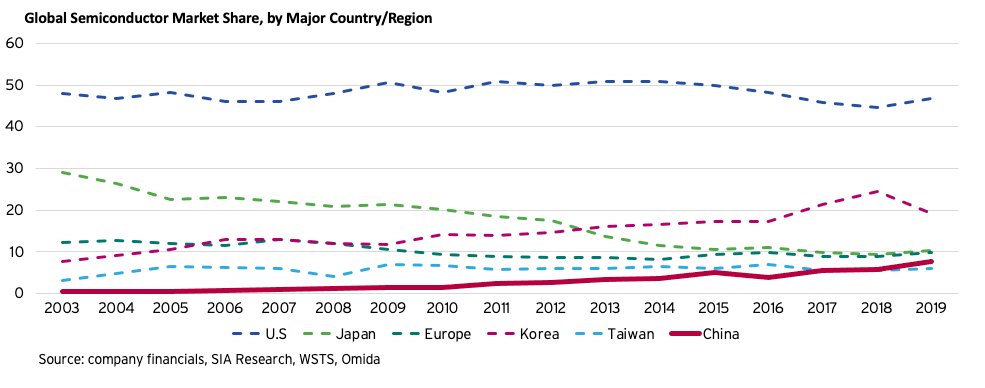

China, meanwhile, is by far the world’s largest purchaser of semiconductors—but its share of global sales still remains marginal. According to Bernstein Research, China purchased approximately $160 billion in semiconductors in 2016, but sold only $20 billion. In other words, semiconductors are China’s biggest import by value—putting it ahead

Given China’s manufacturing prowess in general—it’s the “world’s factory,” after all—its lag in semiconductors seems surprising on the surface. Three of the world’s top-five smartphone companies

For one thing, according to Goodrich, of the Semiconductor Industry Association, the R&D necessary to make advancements in chip design can span decades. There are no shortcuts to understanding the recipe of a chip. “It can take an American company years just to design one chip. Then let’s say you’ve got 5,000 engineers that can reverse engineer the chip and look at the chip layout—by the time you’ve done that, the American company’s already two generations ahead of you,” says Goodrich.

Beyond designing chips, there are also barriers to manufacturing them. Setting up a fabrication facility can cost $10 billion to $15 billion. Inside those facilities are complex machines designed to carry out etchings and moldings at a microscopic level. For Intel, TSMC, Micron, and other chip manufacturers,“their processes are highly proprietary, and you’re literally dealing with a process that is one atom at a time. That knowledge base is not something that you can just go and copy overnight,” says Puhakka.

Factories also need to crank out these chips quickly and consistently, with as few defects as possible. Making integrated circuits is “highly complex, massive scale, and high precision.” says Li. “You need to produce every day, every month, to a degree where you can support say 1.5 billion smartphones every year.”

Analysts say that China’s semiconductor makers remain broadly five to 10 years behind world-class companies in the US, Korea and Taiwan. Li, for example, says that China’s manufacturers can easily make chips that power the iPhone’s fingerprint sensor—despite being a relatively new feature, the underlying technology isn’t that different from what powers a smartphone’s camera.

However, he adds, producing systems-on-a-chip (SoCs) that power 4G connectivity inside high-end smartphones at scale—like those designed by Qualcomm– remains out of reach for most of China’s top semiconductor manufacturers.

As a result China’s telecom sector looks set to remain hugely reliant on US chips for several years—while chip makers like Qualcomm are hugely reliant on China

China’s government has also encouraged foreign chip companies to form joint ventures with domestic counterparts, in hopes that know-how and intellectual property from the overseas firms will get transferred to the Chinese ones. Earlier this year, for example, Chinese investors acquired a controlling stake in the local venture of

The third tactic is simply spending lots of money. In 2014 Beijing launched a 139 billion yuan (then $21.8 billion) fund explicitly for the chip sector, and it’s

Given that acquisitions and JVs have not been effective, moving forward, China will likely be forced to rely on self-funding R&D to improve its semiconductor industry. Can money alone change the industry? Experts are split.

Barry Naughton, an economist at the University of California, San Diego, argues that China will need more than just cash to start making competitive semiconductors—it will need better engineers, managers, and bureaucrats capable of catching up in a sector that other countries have amassed decades of knowledge in. “There are a lot of high tech areas out there, and China sort of has ambitious plans in each one,” he says. “They might think semiconductors are more important than anything else. They’re prepared to throw lots more money at it, but I don’t think the correlation with money is that strong.”

This website is using a security service to protect itself from online attacks. The action you just performed triggered the security solution. There are several actions that could trigger this block including submitting a certain word or phrase, a SQL command or malformed data.

In 1990, the US produced 37% of the world"s chip supply, according to a September 2020 report from the Semiconductor Industry Association. But now, the country is responsible for just 12% of global chip production.

Seventy-five percent of the world"s chip manufacturing comes out of Asia, per the report, and China is positioned to become the largest chip producer by 2030.

Why the decline in the US? It became cheaper to build chip facilities in countries outside of the US. Those foreign governments offer more attractive financial incentives to construct semiconductor factories, like tax breaks and grants. There"s also less regulation in places like Asia. On top of that, there aren"t as many jobs in the US created to run such high-tech factories.

Some of the country"s largest chip manufacturers are also some of the biggest in the world. Intel still produces much of its chip supply at home, as the Wall Street Journal reported. But other major US chip producers outsource manufacturing to companies in Asia due to costs. One of those foreign contract companies is Taiwan Semiconductor Manufacturing Company, which produces more than half of the world"s computer chips and is also Apple"s primary supplier.

Making computer chips is a complex process. It"s also difficult and expensive to build new facilities to manufacture the vital silicon component, which means companies have to rely on existing plants. A new semiconductor factory can cost up to $20 billion, as ON Semiconductor CEO Keith Jackson wrote in Fortune, and that price tag is much higher in the US.

President Joe Biden is aware of the issue and the threats p

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey