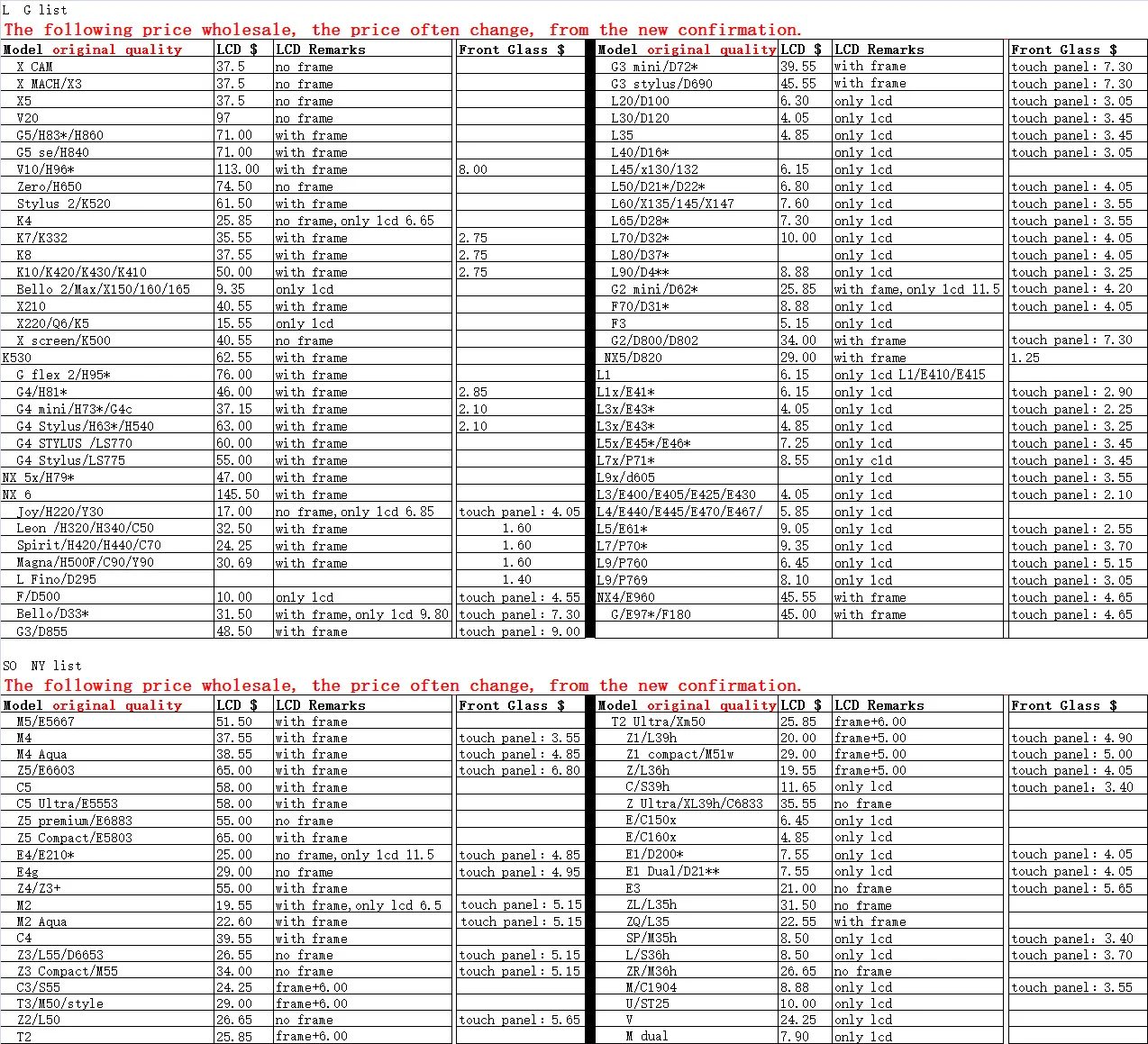

what is the lcd screen pricelist

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market has smoked. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel prices are already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

The 43 inches and 55 inches rose more than double digits in August, reaching 13.7% each, and rose another $7 and $13, respectively, to $91 and $149, respectively, in September.

For larger sizes, overseas stocks remained strong, with prices for 65 inches and 75 inches rising $10 on average to $200 and $305 respectively in September.

The price of LCDS for large-size TVs of 70 inches or more hasn’t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panels was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

This kind of price correction is in line with the law of industrial development. Only with reasonable profit space can the whole industry be stimulated to move forward.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China’s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using “dig through old bonus – selling high price – the development of new technology” the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China’s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, which more or less will cause supply imbalance, the industry needs to be cautious.

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as “upstart” flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. “LCD will still be the mainstream in this decade,” he said.

On the other hand, there is no risk of neck jam in China’s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

This website is using a security service to protect itself from online attacks. The action you just performed triggered the security solution. There are several actions that could trigger this block including submitting a certain word or phrase, a SQL command or malformed data.

This website is using a security service to protect itself from online attacks. The action you just performed triggered the security solution. There are several actions that could trigger this block including submitting a certain word or phrase, a SQL command or malformed data.

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved December 27, 2022, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed December 27, 2022. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: December 27, 2022. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited December 27, 2022)

A Grade: Fully Functional OEM screens with broken glass. Screens are previously refurbished or have light print (status bar) are still considered as A Grade

In September, area prices for all screen sizes up to 65” fell in a range from $92 to $106 per square meter, with the 65” area price tied with 32” for the lowest in the industry at $92 per square meter. The largest screen size in our survey, 75” panels, continues to have a premium but that premium has eroded steadily. In June 2022, a 75” panel was priced at $144 per square meter, a $41 or 40% premium over the 32” area price. By September, the 75” premium over 32” had dropped to $27 and 29%. While prices for 65” and smaller panels increased in October, 75” prices stayed flat, and we expect that pattern to continue through Q4 and Q1.

Throughout the many cycles in the industry, we have seen that the most commoditized screen size is 32”, because this screen size can be efficiently produced on every Gen size fab from Gen 6 through Gen 10.5. Thus, when prices go down, 32” prices go down fastest, but when prices increase, the 32” price increase fastest as well. This was true in October as 32” prices increased by $2 or 7% for the month; the area price increased from $92 per square meter in September to $99 in October.

The next chart shows our estimates of cash costs vs. panel prices for large TV panels. While 55” panels have been below cash costs for most of the year, 65” prices reached cash costs in Q2 and for the first time 75” panel prices fell below cash costs in Q3. We expect that 55” and 65” panel prices will increase in Q4 and Q1 2023 but will remain slightly below cash costs.

LCD TV panel prices have reached all-time lows but they continue to decline, and although the pace of decline is slowing in the third quarter, we now forecast that the industry will have an “L-shaped” recovery in the fourth quarter. In other words, no recovery at all until 2023. The ‘perfect storm’ of a continued oversupply, near-universally weak demand and excessive inventory throughout the supply chain has combined, and every screen size of TV panel has reached an all-time low price. Although fab utilization has slowed sharply in July, we do not see any signal to suggest that prices can increase any time soon.

![]()

A string of new LCD factories being built, combined with slow demand for notebook and desktop PC screens, caused LCD prices to fall during the first three months of the year, and the downward trend is expected to continue, vendors and analysts said.

Falling prices for LCD (liquid crystal display) screens should help ensure that users find bargains for new monitors, laptops and LCD TVs this year, since the screen is among the most-expensive components in those products. The price declines are also causing vendors to improve picture quality to catch users" eyes and draw them away from competitors.

Makers such as LG.Philips and Samsung Electronics, the world"s two largest LCD producers, are ramping up production at state-of-the-art factories, while rivals continue to add lines at existing plants. Other big players, such as AU Optronics in Taiwan, expect to add plants later this year, which should help keep LCD prices tame.

"The biggest impact from the new plants will be in the first part of this year, but there will be some impact throughout the year," said Frank Lee, an LCD industry analyst for Deutsche Securities Asia in Taipei.

The new LCD plants were built largely to keep pace with demand for LCD TVs, which have been among the hottest-selling items this year. Cutthroat competition among LCD makers also has been a boon to users, ensuring steadily falling prices for the past few years, as screen sizes increase.

For example, prices for 42-inch LCD screens that will be delivered to TV makers in the second half of April fell by $35 each since the end of March, to an average of $890, according to WitsView Technology Co., an industry researcher. Prices for 19-inch panels for PC monitors fell $5 to an average $160.

Average selling prices for LCD panels at AU Optronics fell nearly 12% quarter-on-quarter by the end of March, and the company forecast continued declines into the second quarter, according to executives at its first quarter earnings conference Thursday.

"Screen prices have remained weak in April but should stabilize in May or June," said Hsiung Hui, executive vice president of strategic planning at AU.

The company expects the price of screens used in desktops and laptops to drop by about 10% quarter-on-quarter during the April to June period, while LCD-TV screen prices will decline by a smaller percentage, in the mid single digits, it said.

LG.Philips said its sales declined in the first quarter compared to the fourth, because of a decline in the average selling prices in LCDs destined for laptops and desktop monitors, with an overall price decline of around 10% for all LCD screen products.

The South Korean company, a joint venture between LG Electronics Inc. and Koninklijke Philips Electronics, said its average selling prices in the current quarter will drop by a mid- to high-single digit percentage compared to the end of the first quarter.

The company is increasing production at a state-of-the-art LCD factory in Korea, as is rival Samsung. AU is building a similar plant in Taiwan that it expects to be in production by the third quarter of this year. LG said it would produce mainly 42-inch and 47-inch screens at the plant, aimed at the LCD-TV market.

Other LCD industry competitors are also increasing production to keep up with demand for LCD-TVS. On Wednesday, S-LCD Corp., the LCD-panel manufacturing joint venture of Sony and Samsung, said it plans to invest $238 million to expand production at its factory in Tangjeong, South Korea.

I’m hearing from some industry friends that LCD display panel prices are rising – which on the surface likely seems incongruous, given the economic slowdown and widespread indications that a lot of 2020 and 2021 display projects went on hold because of COVID-19.

On the other hand, people are watching a lot more TV, and I saw a guy at Costco the other day with two big-ass LCD TVs on his trolley. And a whole bunch of desktop monitors were in demand in 2020 to facilitate Work From Home. So demand for LCD displays is up outside of commercial purposes.

Organizations that pay attention to supply chains and pricing confirm prices ended high in 2020 and are expected to climb again this quarter and flatten out later in the year.

The Korean business portal BusinessKorea says one explanation was a power outage that shut down a big glass substrate factory in Japan, which was serious enough that the plant will only get back to normal sometime in this quarter.

Continuing strong demand and concerns about a glass shortage resulting from NEG’s power outage have led to a continuing increase in LCD TV panel prices in Q1. Announcements by the Korean panel makers that they will maintain production of LCDs and delay their planned shutdown of LCD lines has not prevented prices from continuing to rise.

Panel prices increased more than 20% for selected TV sizes in Q3 2020 compared to Q2, and by 27% in Q4 2020 compared to Q3, and we now expect that average LCD TV panel prices in Q1 2021 will increase by another 9%.

Prices for every size of TV panel will increase in Q1 at a slower rate, ranging from 4% for 75” to 13% for 43”. Although we continue to expect that the long-term downward trend will resume in the second quarter of 2021, we no longer expect that panel prices will come close to the all-time lows seen earlier this year. The situation remains dynamic, and the pandemic may continue to affect both supply and demand.

TV panel prices however, continued to rise at an ‘unprecedented’ rate again, far ahead of our expectations, and panel producers do not seem to be hesitant about continuing to push prices further.

Given that TV set demand continues to outstrip production capacity, panel producers are already expecting to raise prices again in 1Q, typically a sequentially weaker quarter. There is a breaking point at which TV set brands will forego requested panel price increases in order to preserve what is left of margins, and with the increasing cost of TV set panel inventory, we expect TV set producers to become unprofitable relatively quickly.

Does that mean they will stop buying and face losing market share to those that are willing to pay higher prices to see unit volume growth? Eventually, but heading into the holidays it doesn’t seem likely this year, so we expect TV panel prices to rise again in December.

With a lot of the buyer market for digital signage technology financial wheezing its way into 2021, rising hardware prices are likely even less welcomed than in more normal times. But the prices for display hardware, in particular, are dramatically lower they were five years ago, and even more so looking back 10-15 years.

Use our “Get an Estimate” tool to review potential costs if you get service directly from Apple. The prices shown here are only for screen repair. If your iPhone needs other service, you’ll pay additional costs.

If you go to another service provider, they can set their own fees, so ask them for an estimate. For service covered by AppleCare+, your fee per incident will be the same regardless of which service provider you choose.

Your country or region offers AppleCare+ for this product. Screen repair (front) is eligible for coverage with a fee by using an incident of accidental damage from handling that comes with your AppleCare+ plan.

The Apple Limited Warranty covers your iPhone and the Apple-branded accessories that come in the box with your product against manufacturing issues for one year from the date you bought them. Apple-branded accessories purchased separately are covered by the Apple Limited Warranty for Accessories. This includes adapters, spare cables, wireless chargers, or cases.

Depending on the issue, you might also have coverage with AppleCare+. Terms and Conditions apply, including fees. Feature availability and options may vary by country or region.

We guarantee our service, including replacement parts, for 90 days or the remaining term of your Apple warranty or AppleCare plan, whichever is longer. This is in addition to your rights provided by consumer law.

Replacement equipment that Apple provides as part of the repair or replacement service may contain new or previously used genuine Apple parts that have been tested and pass Apple functional requirements.

PSOne LCD Screen prices (Playstation) are updated daily for each source listed above. The prices shown are the lowest prices available for PSOne LCD Screen the last time we updated.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey