lcd module market outlook made in china

China accounted for 40 percent of the global display market in terms of sales in the first quarter of this year, rising to the top by beating South Korea by a margin of seven percentage points. In 2019, South Korea was 11 percentage points ahead of China. Last year and this year, however, the global display demand surged with regard to COVID-19, LCD panel prices soared as a result, and Chinese companies boosted their share in the market they are dominating.

China’s global LCD panel market share for this year is estimated at 60.7 percent. In addition, its share in the smartphone OLED panel market is likely to rise from 15 percent to 27 percent this year and next year. In this market, Samsung Display’s current share is 80 percent and the share is forecast to fall to 60 percent or so next year.

According to market research firm DSCC, BOE, the largest display panel manufacturer in China, posted US$7.7 billion in sales and US$1.4 billion in operating profit in the first quarter to exceed the sales and profits of Samsung Display and LG Display for the first time ever.

Chinese companies in the industry benefit from their huge domestic market and substantial government subsidies. The subsidies given to BOE for 10 years from 2010 exceed two trillion won and those given to the top four for eight years from 2012 are more than 5.5 trillion won, which is more than 25 percent of Samsung Display’s and LG Display’s net profit for that period.

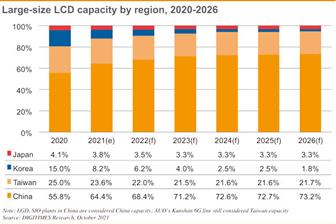

Chinese presence in the LCD panel industry continues its expansion. Samsung used to dominate in the high-end panel market but is now no longer obsessed with the business as before. Samsung has sold its panel production line to China"s CSOT. China-made panels are expected to dominate the market before OLED panel is mature enough to erode the market share of LCD panels. It is predicted China-made panels will account for over 70% of the global panel market share.

In terms of applications, cockpit dashboards and central control systems both maintain double-digit growth. Interactive digital signage displays also perform well with good sales. The market preference is tilting towards the large-sized models. After taking over Samsung"s production line, CSOT is to be a significant player and poses threats to Taiwanese firms.

Since the pandemic is waning, the global TV market as a panel end-user segment is facing a downturn in demand. Components shortage, port congestion, China"s policy on power restrictions, coupled with typhoons in Asia have exacerbated the issues. Considering quarterly output between 7-8 million units, Taiwanese TV makers like TPV and Hon Hai (Foxconn) willl report moderate sequential growths in third-quarter and fourth-quarter 2021, but will see declines of about 15% year-on-year. Apparently, the big demand cycle of panels has come to an end.

Introduction: Global LCD industry shift and automotive intelligence together to promote the rapid development of China’s LCD panel industry, which will bring a continuous increase in demand for backlight modules, China’s backlight module industry has greater potential for development.

LCD panel backlight module consists of a backlight light source, light guide, optical film, and a plastic frame, which is an important component of LCD display panel. As the backlight module has technology-intensive and labor-intensive attributes, with abundant high-skilled labor advantage China is attracting the global LCD panel industry to the domestic rapid transfer.

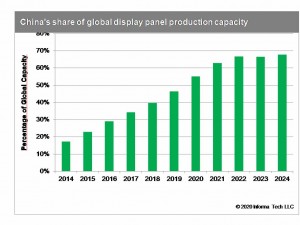

From LCD application to the present, the global LCD panel industry capacity transfer has gone through three periods, 2000 Japan dominated the global LCD industry; 2000 – 2010, Japan’s production capacity to South Korea and Taiwan; 2010 to the present, Japanese manufacturers gradually withdraw from the LCD panel industry, production capacity began to transfer to mainland China, so far, mainland China LCD production capacity has occupied the global half of the world.

In recent years, South Korea’s Samsung and LG display will shift their business focus to OLED, and will gradually shut down their LCD production lines and withdraw from the LCD panel industry; at the time of South Korean manufacturers’ withdrawal, domestic enterprises are stepping up new construction to expand LCD production capacity.

BOE, Huaxing photoelectric, Huike, CEC in 2020 – 2021, a total of eight 7 generation LCD production lines completed and put into operation, and domestic panel manufacturers have further expansion plans, the next few years domestic LCD production capacity will continue to increase.

LCD panel manufacturers tend to choose the nearby supporting module suppliers for the safety of the key component supply chain and cost reduction considerations. LCD panel production capacity transfer to China will bring opportunities to domestic backlight module manufacturers and drive the development of the domestic backlight module industry.

At the same time, there is also a huge demand for new cars in China. Although China’s car sales have reached 25 million, the current per capita car ownership in China is only a quarter of the developed countries, the future potential for new car demand is still very large. Therefore, China’s car display market growth potential is large, which will directly drive the domestic backlight module demand continues to increase.

According to the terminal application size, backlight module can be divided into large, medium, and small size, of which small size backlight module is mainly used in smartphones, wearable devices, and other terminals, the medium size used in notebook computers, tablet PCs, car screens and other terminals, the large size is mainly used in LCD TV.

From the market competition pattern, the domestic backlight module enterprises are deeply plowed in their respective competitive advantage in the field of segmentation, including Baoming technology, Longli technology mainly layout small size cell phone display field, Hanbo high-tech, Weishi electronics mainly layout in the size of car display and notebook computer field, Rui Yi photoelectric and photoelectric in each field have layout.

From the industry development trend, smartphone display is transitioning to OLED, LCD TV market is gradually saturated, the future of large size and small size backlight module market potential is relatively small; and the future of the car display market potential is huge, by the backlight module manufacturers are unanimously optimistic, are currently accelerating the layout ( see Table 2 ). Focusing on the traditional medium-sized backlight module field, Hanbo Hi-Tech and Weishi Electronics have significant advantages in core technology patents, downstream customer resources, process experience accumulation, production costs, etc., and have more development advantages in the future.

The current global LCD display panel industry is rapidly moving to China, which brings development opportunities to China’s backlight module industry. In addition, automotive intelligence will also bring a continuous increase in demand for medium-sized car displays, the first to enter the field of medium-sized backlight module manufacturers with its customer resources, core technology, scale efficiency, and other advantages will be more beneficial.

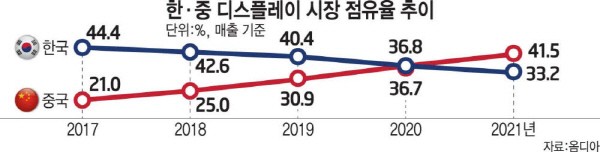

It is the first time that China took over the No. 1 spot in the display market, which Korea has always been a leader in. The title of “the strongest country in display market” is lost after 17 years. It would not be possible to reclaim the No. 1 spot if Korea cannot find a way to expand investment in next-generation displays such as organic light emitting diodes (OLED).

According to market research firm Omdia, China recorded $64.8 billion in sales including LCD and OLED in the global display market last year. China took over Korea’s No. 1 spot with a market share of 41.5%. Korea"s market share fell 8.3 points (p) to 33.2%. This is the first time since 2004, in 17 years, that Korea had to hand over the No. 1 spot. Korea had a 9.4 p advantage in market share over China up until 2019.

China overtook Korea and seized power in the LCD market by offering a low-priced products. BOE, China"s largest panel manufacturer, has become the world"s largest LCD manufacturer with help of the subsidy from the Chinese government. LCD sales was $28.6 billion last year, accounting for 26.3% of the total LCD market. The sales of Chinese companies such as BOE, CSOT, Tianma, and Visionox increased significantly as demand for TV and information technology (IT) devices increased with the prolonged COVID 19 and increased price of LCD panel.

After taken over in the LCD market, Korea is focusing on the highly-valued OLED market. Samsung Display and LG Display are transforming their LCD production lines to OLED. Korea is the No. 1 with 82.3% of the global OLED market shares according to Omdia, and China’s market share only accounts for16.6%.

China"s dominance is expected to continue for some time because the large display market such as TVs and laptops still depends on LCD. Only when Korea starts to reduce OLED panel prices by mass producing OLED, then Korea can replace the LCD market led by China.

China has also started to narrow the gap with Korea in OLED industry. BOE and other companies have commercialized OLED for small and medium-sized displays such as mobile, laptop, and tablet. Following LCD market, China is threatening Korea in OLED market as well as China expands OLED market share mainly in the Chinese smartphone market.

Critics are pointing out that Korea needs to expand in OLED market and develop new technologies in order to maintain the OLED gap with China. Korea must take control over the large TV panel market, which has a large technological gap with China, and create a new form factor with new technologies such as flexible, rollable, and bendable panels.

An official from the display industry said, “With the government-led industrial promotion policy and copious domestic market, China is making an effort to solidify its leading position in the display industry. There is a neglect on display industry in Korea since the display promotion policy is almost non-existent compared to semiconductors and batteries.”

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved December 26, 2022, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed December 26, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: December 26, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited December 26, 2022)

LCD manufacturers are mainly located in China, Taiwan, Korea, Japan. Almost all the lcd or TFT manufacturers have built or moved their lcd plants to China on the past decades. Top TFT lcd and oled display manufactuers including BOE, COST, Tianma, IVO from China mainland, and Innolux, AUO from Tianwan, but they have established factories in China mainland as well, and other small-middium sizes lcd manufacturers in China.

China flat display revenue has reached to Sixty billion US Dollars from 2020. there are 35 tft lcd lines (higher than 6 generation lines) in China,China is the best place for seeking the lcd manufacturers.

The first half of 2021, BOE revenue has been reached to twenty billion US dollars, increased more than 90% than thesame time of 2020, the main revenue is from TFT LCD, AMoled. BOE flexible amoled screens" output have been reach to 25KK pcs at the first half of 2021.the new display group Micro LED revenue has been increased to 0.25% of the total revenue as well.

Established in 1993 BOE Technology Group Co. Ltd. is the top1 tft lcd manufacturers in China, headquarter in Beijing, China, BOE has 4 lines of G6 AMOLED production lines that can make flexible OLED, BOE is the authorized screen supplier of Apple, Huawei, Xiaomi, etc,the first G10.5 TFT line is made in BOE.BOE main products is in large sizes of tft lcd panel,the maximum lcd sizes what BOE made is up to 110 inch tft panel, 8k resolution. BOE is the bigger supplier for flexible AM OLED in China.

As the market forecast of 2022, iPhone OLED purchasing quantity would reach 223 million pcs, more 40 million than 2021, the main suppliers of iPhone OLED screen are from Samsung display (61%), LG display (25%), BOE (14%). Samsung also plan to purchase 3.5 million pcs AMOLED screen from BOE for their Galaxy"s screen in 2022.

Technology Co., Ltd), established in 2009. CSOT is the company from TCL, CSOT has eight tft LCD panel plants, four tft lcd modules plants in Shenzhen, Wuhan, Huizhou, Suzhou, Guangzhou and in India. CSOTproviding panels and modules for TV and mobile

three decades.Tianma is the leader of small to medium size displays in technologyin China. Tianma have the tft panel factories in Shenzhen, Shanhai, Chendu, Xiamen city, Tianma"s Shenzhen factory could make the monochrome lcd panel and LCD module, TFT LCD module, TFT touch screen module. Tianma is top 1 manufactures in Automotive display screen and LTPS TFT panel.

Tianma and BOE are the top grade lcd manufacturers in China, because they are big lcd manufacturers, their minimum order quantity would be reached 30k pcs MOQ for small sizes lcd panel. price is also top grade, it might be more expensive 50%~80% than the market price.

Besides the lcd manufacturers from China mainland,inGreater China region,there are other lcd manufacturers in Taiwan,even they started from Taiwan, they all have built the lcd plants in China mainland as well,let"s see the lcd manufacturers in Taiwan:

Innolux"s 14 plants in Taiwan possess a complete range of 3.5G, 4G, 4.5G, 5G, 6G, 7.5G, and 8.5G-8.6G production line in Taiwan and China mainland, offering a full range of large/medium/small LCD panels and touch-control screens.including 4K2K ultra-high resolution, 3D naked eye, IGZO, LTPS, AMOLED, OLED, and touch-control solutions,full range of TFT LCD panel modules and touch panels, including TV panels, desktop monitors, notebook computer panels, small and medium-sized panels, and medical and automotive panels.

AUO is the tft lcd panel manufacturers in Taiwan,AUO has the lcd factories in Tianma and China mainland,AUOOffer the full range of display products with industry-leading display technology,such as 8K4K resolution TFT lcd panel, wide color gamut, high dynamic range, mini LED backlight, ultra high refresh rate, ultra high brightness and low power consumption. AUO is also actively developing curved, super slim, bezel-less, extreme narrow bezel and free-form technologies that boast aesthetic beauty in terms of design.Micro LED, flexible and foldable AMOLED, and fingerprint sensing technologies were also developed for people to enjoy a new smart living experience.

Hannstar was found in 1998 in Taiwan, Hannstar display hasG5.3 TFT-LCD factory in Tainan and the Nanjing LCM/Touch factories, providing various products and focus on the vertical integration of industrial resources, creating new products for future applications and business models.

driver, backlight etc ,then make it to tft lcd module. so its price is also more expensive than many other lcd module manufacturers in China mainland.

Maclight products included monochrome lcd, TFT lcd module and OLED display, touch screen module, Maclight is special in custom lcd display, Sunlight readable tft lcd module, tft lcd with capacitive touch screen. Maclight is the leader of round lcd display. Maclight is also the long term supplier for many lcd companies in USA and Europe.

If you want tobuy lcd moduleorbuy tft screenfrom China with good quality and competitive price, Maclight would be a best choice for your glowing business.

Chinese display manufacturers are chasing their South Korean rivals closely by planning to release a larger volume of liquid-crystal panels over 32 inches this year, said a market researcher Sunday.

According to a report on the 2017 shipment strategies of Chinese TV panel makers by IHS Markit, Chinese LCD panel suppliers are forecast to ship out a total of 320,000 large-size panels larger than 32 inches by the end of this year, a 33 percent surge from last year.

“By the end of 2018, China will be the largest region for TFT LCD capacity, and larger-sized products may make their factories more efficient and profitable than they have been when producing 32-inch panels,” he said.

The strategy shift of the Chinese players suggests that they might outstrip Korean display makers in the global large-size display market, the analyst said.

“The strategies of Chinese panel makers will significantly influence global supply and demand,” Wu said. “In 2015 and 2016, the Chinese companies shipped 33.2 percent of worldwide LCD TV panel, trailing only Korean panel makers at 36.4 percent.”

The competition structure has been advantageous for the Korean players, since their Chinese rivals had been focusing on small LCD panels until last year. But now the Korean firms are facing fiercer competition in prices.

Although demand for organic-light emitting diode panels in the TV market is gradually rising, dominance of LCD panels is projected to continue for the foreseeable future.

“While OLEDs are expected to post sharp growth, they will not be able to usurp LCD as the panels of choice for upper-end TVs,” another report by IHS Markit said.

According to a report released by market research firm CCID Consulting, the revenue of China"s display industry exceeded 580 billion yuan ($83.2 billion) in 2021, up 40.5 percent year-on-year, accounting for 36.9 percent of the global display market.

Sigmaintell Consulting, a Beijing-based market research firm, showed that global shipments of flexible OLED panels are expected to reach 405 million units in 2022, with Chinese display makers accounting for about 36 percent of the market share.

"The penetration rate of OLED displays in the mobile market is expected to reach 50 percent by 2024," Li said, adding that about 60 to 70 percent of sales revenue will be contributed by OLED technologies by then.

Chinese display panel makers accounted for nearly half of the share in the global liquid crystal display TV panel market in the first half of this year, dominating the industry.

Beijing-based market researcher Sigmaintell Consulting said shipments of LCD TV panels worldwide totaled 140 million pieces in the year"s first half, up 3.6 percent compared with the same period a year ago.

The shipment of BOE"s LCD TV panels stood at 27.6 million in the Jan-June period while LG Display followed with 22.7 million, down 4.5 percent year-on-year. Innolux Display Group was in third place, having shipped 21.9 million units.

Shenzhen China Star Optoelectronics Technology Co Ltd, a subsidiary of consumer electronics giant TCL Corp, ranked fourth, shipping 19.3 million pieces of TV panels. Chinese panel makers accounted for a 45.8 percent share in the global LCD TV panel market.

Sigmaintell estimated that the gap between supply and demand would widen further, and the panel market may face a long-term risk of oversupply. The industry may have to undergo a reshuffle given fierce market competition, it said.

Separately, BOE"s Gen 10.5 TFTLCD production line has entered operation in Hefei, Anhui province. The plant will produce high-definition LCD screens of 65 inches and above.

"China"s semiconductor display industry has taken large steps forward in the past decade, changing the display industry"s global competitive landscape. China has transformed into the world"s largest consumer market and manufacturing base for display terminals, with huge market potential," said BOE Vice-President Zhang Yu.

CSOT also announced in November last year that its Gen 11 TFT-LCD and active-matrix OLED production line had officially began operation. The project will produce 43-inch, 65-inch and 75-inch liquid crystal display screens.

Compared with traditional LCD display panels, OLED has a fast response rate, wide viewing angles, high-contrast images and richer colors. It is thinner and can be made flexible.

The news outlets proclaimed that South Korea"s title of "the strongest country in display market" was lost after 17 years and that it would not be possible for South Korea to reclaim the No. 1 spot if it cannot find a way to ramp up investment in next-generation displays such as organic light emitting diodes (OLED).

The year 2021 was a milestone for China"s display panel industry. Chinese display panel makers, led by companies such as BOE Technology Group Co, Shenzhen China Star Optoelectronics Technology Co, Tianma, and Visionox, accounted a combined 40.4 percent of global market share in turnover, outstripping South Korea"s 36.3 percent, data from Beijing-based market research provider Sigmaintell revealed.

It is the first time that Chinese companies held a larger market share that their South Korean rivals, mainly Samsung Display and LG Display, as in 2020, South Korean companies led with 39.8 percent of market share, 4.8 percentage points higher than China.

A different set of data published by market research firm Omdia showed the same pattern. China recorded $64.8 billion in sales including liquid crystal display (LCD) and OLED in the global display market in 2021. China overtook South Korea"s No. 1 spot with a market share of 41.5 percent while South Korea"s market share fell to 33.2 percent.

Market competition in display panel, an indispensable part for consumer electronics, is fierce. And the competing relations between Chinese and South Korean companies exist in display panels for smartphones, televisions, monitors, among other product segments.

In terms of LCD, Chinese companies have long surpassed their South Korean counterparts in shipments, and in recent years Chinese companies also invested heavily in advanced production lines for small-size OLED screens that is used in smartphones.

Etnews suggested South Koran companies reduce OLED panel prices by mass producing OLED, which requires substantial investment in production capacity, only then can South Korea replace the LCD market led by China. The battlefield of choice for South Korean firms would be in large TV panel market, in which they still enjoy large technological gap with China.

Even as South Korean companies seek to entrench their lead position in large-size OLED, their efforts may not turn out to be as effective as imagined, Lee said, as large OLED may not prove to be a worthy barrier behind which South Korean companies could fall back upon as it does not have unique functions that could not be fulfilled by LCD.

In 2021, shipments of large-size OLED display panels were just 6.7 million units while in the same period the shipments of LCD reached 210 million units.

"Back in the days of LCD phasing out cathode ray tube and plasma display panel, LCD could fulfill unique functions the other two types could not. That is something we don"t see in OLED. The things OLED can do, LCD can also do and are being constantly perfected," Lee said. "That means fall back behind the OLED castles may not be enough to fend off challenges lurched out by Chinese players."

South Korean companies would be increasingly willing to export their advanced technology once they realized they are losing market shares, according to Lee.

With the evolutionary changes in consumer electronics from past few years, the demand for the electronic parts is increasing rapidly. LCD display modules are electronically modulated optical device or flat-panel display and use the light-modulating properties of liquid crystals.

LCD display modules display arbitrary image or fixed images and low content information. The information can be displayed or kept hidden including digits, preset words, and seven-segment displays, as in a digital clock.

Increasing production of electronic devices such as aircraft cockpit displays, computer monitors, LCD televisions, indoor and outdoor signage and instrument panels is responsible for the increasing demand for the LCD display module. Manufacturers of the LCD display modules are focusing on developing innovative products to attract more customers to increase the revenue generation by sales of displays.

Manufacturers of the LCD display modules are coming up with the product innovations such as background display colors, character sizes, number of rows, and others and these features are fueling the increasing integration of the LCD display modules.

Constant advancements in the LCD display modules and improvement in the functionality of displays is the primary factor driving the growth of the LCD display module market.

The manufacturers are also focusing on the delivering a LCD display modules are per the end user requirements as these displays are primarily used for the consumer electronic devices which are produced in bulk quantity.

The increasing production of small electronic devices such as cameras, watches, calculators, clocks, mobile telephones, DVD players, clocks, and other devices is creating a huge demand from manufacturers of these products for the LCD display modules as per their product requirements.

On the other hand, availability of LCD display modules at low prices due to the entry of new players from developing countries, shortage of electronic components is a significant challenge for the established players in this market.

The global vendors for LCD Display Module include RAYSTAR OPTRONICS, INC., WINSTAR Display Co., Ltd., Newhaven Display International, Inc., Sharp Microelectronics, 4D Systems, ELECTRONIC ASSEMBLY GmbH, Kyocera International, Inc., Displaytech, and others. LCD display manufacturers are coming up with the new features and more advanced functionalities of the displays for sustaining in the global competition.

In February 2018, Displaytech, LCD display module manufacturer released DT070CTFT, a 7 inch 800 x 480 TFT display. The company is offering LCD displays with a resistive touch as well as a capacitive touch panel.

The global market for LCD Display Module is divided on the basis of regions into North America, Latin America, Western Europe, Eastern Europe, the Asia Pacific Excluding Japan, Japan, China, and Middle East & Africa. Among these regions, the countries such as Taiwan, South Korea, and China holds major market share in terms of revenue generation from the sale of LCD display module because of the higher presence of manufacturers for these displays as well as the dense presence of the consumer electronics manufacturers.

North America, Western Europe is the second largest market for the LCD display module due to increasing demand from consumer electronics manufacturers. MEA region is expected to grow at moderate CAGR.

The report provides in-depth analysis of parent market trends, macro-economic indicators and governing factors along with market attractiveness as per segments. The report also maps the qualitative impact of various market factors on market segments and geographies.

In the first half of 2019, affected by the overall macroeconomic and investment environment, the overall size of China"s commercial led display market only achieved a small increase. According to relevant data, the market scale of the commercial led display market in China in 2019H1 reached 4.5 billion USD, a year-on-year increase of 3.7%. Compared with the overall market, the growth of the large led screen splicing market is at a high level. The data shows that the sales of the 2019H1 China"s large-screen splicing market (including DLP, LCD, and LED small pitch) have reached 1.05 billion USD, a year-on-year increase. 23.7%. In this three-pronged situation, what is the performance of small pixel pitch

According to the survey, China"s large led screen splicing market can account for 61% of the world, LED display products can account for 57% in the Chinese market, and the global competitiveness of LED companies is also strengthening. In recent years, the competition in the large led screen splicing market has become more and more fierce. At present, the domestic large led screen splicing industry still presents three technologies of LCD, DLP and LED small pixel pitch. It is worth mentioning that LCD is currently at low price competition. DLP is facing internal and external problems, including cost and external pressure. In contrast, the small pixel pitch spacing of LEDs has been continually leaping forward. LEDs have a small gap and grow at a high speed. The development momentum is fierce. There are relatively large threats to LCD and DLP. From the perspective of existing product layout, small pixel pitch led display is more balanced and comprehensive development. The situation has accelerated the popularity of the market.

The small pixel pitch LED display market has formed a pattern of P1.2 leading high-end, P1.5 main performance card and P1.8 leading price market. In particular, further market price wars have made the P1.8-class products almost become the “super-economic large led screen technology” acceptable to the third- and fourth-line markets, and have become a weapon for the continuous increase of the small pixel pitch LED display market. At the same time, COB technology"s small pixel pitch LED product market has further increased brand participation, supply richness and product quality, and market awareness has also been greatly improved. As one of the next-generation small pixel pitch LED technology routes, COB technology brings internal competition and vitality to the small pixel pitch LED display market, which is beneficial to the healthy development of the entire industry and provides sufficient “technical stamina” for the future market.

The essence of the high-end market reflects the technical and service strength of LED display manufacturers, and it also puts more demanding "task" requirements to LED display manufacturers. With the rapid development of big data information, the large led screen splicing products carry not only the function of the display terminal, but also the high-efficiency analysis of massive data information, and then display the analysis results, effectively assisting management decisions. Based on the needs of these markets, in order to facilitate the operation and management of the system, the small pixel pitch led display will be more technology integrated into the future. At the same time, with the continuous advancement of display technology, the high-definition display requirements in the high-end display field will be more The higher the distance, the smaller the spacing will be.

In addition, the development of traditional small pixel pitch LED display has its inherent “progressive” features: that is, most brands in the market are gradually transitioning from outdoor LED display to large pixel pitch LED display technology to smaller pixel pitch products, and then enter P2.5. The "small pixel pitch" and "micro pixel pitch" markets below the pitch, and gradually become more widely used in the field of indoor display. Different from the development of traditional LED display, the field of large-screen splicing is an application-oriented field, not a technical field. This makes the concept of integrated display services more and more emerging. LED display companies to develop product layout based on customer resource advantages, is a good strategy. For example, many security-initiated brands have established product solutions covering all display technology categories, while companies with small-pitch LEDs can also participate in display panels such as LCD and DLP to realize the role of integrated display service providers.

In any industry, the survival of the fittest is the inevitable development. The large-screen splicing market will continue to flourish, and more and more LED small-pitch manufacturers will gradually enter this ranks. Whoever can make rapid progress will be able to live longer in the market. From the perspective of long-term development, in the face of market competition, LED display companies maintain technological innovation, products continue to improve and continue to innovate and develop. The large-screen splicing market is bound to win, and in view of its ever-increasing market threshold, it is obviously not all enterprises. Can be divided. Therefore, the expansion of large-screen splicing will become the touchstone of the market competitiveness of small-pitch LED display enterprises. The gains and losses will directly affect the long-term development of enterprises.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey