lcd panel manufacturers market share 2018 factory

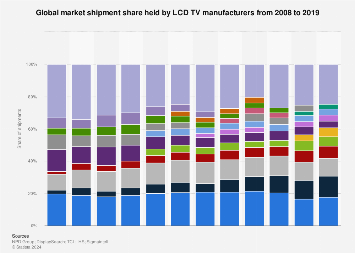

BOE Technology Group, the Chinese electronic components producer, is expected to be the leader in producing LCD display panels in the coming years, with a forecast capacity share of 24 percent by 2022. China is the country that has the largest LCD capacity, with a 56 percent share in 2020.Read moreLCD panel production capacity share from 2016 to 2022, by manufacturerCharacteristicBOEChina StarInnoluxAUOLGDHKCCEC PandaSharpSDCOther-----------

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph]. In Statista. Retrieved December 24, 2022, from https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "LCD panel production capacity share from 2016 to 2022, by manufacturer." Chart. June 8, 2020. Statista. Accessed December 24, 2022. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. (2020). LCD panel production capacity share from 2016 to 2022, by manufacturer. Statista. Statista Inc.. Accessed: December 24, 2022. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2022, by Manufacturer." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC, LCD panel production capacity share from 2016 to 2022, by manufacturer Statista, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/ (last visited December 24, 2022)

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved December 24, 2022, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed December 24, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: December 24, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited December 24, 2022)

The market for equipment to manufacture LCD and OLED displays for smartphones and TVs grew 28% in 2018 following a growth of 33% in 2017. Applied Materials" (NASDAQ:AMAT) revenues grew 36%. A key driver for AMAT"s strong performance was the sale of equipment to Chinese LCD manufacturers BOE Technology and China Star Optoelectronics Technology to manufacture 10.5G panels for the production of 75-inch LCD TVs.

While the 10.5G market will be strong again in 2019, AMAT will face headwinds in sectors that utilize equipment for the production of smaller displays, primarily smartphones.

During Applied Materials’ recent Q1 earnings call, CEO Gary Dickerson noted: "In display, weakness in emerging markets is also impacting the timing of customers’ investment plans. We see some TV factory projects pushing out of year and into 2020. As a result, we now believe our display equipment revenue in 2019 will decline by about a third from 2018"s record levels. We also expect revenue in the second fiscal quarter to be significantly lower than our average run rate for the year."

Figure 1 shows market shares among the top five equipment companies. AMAT’s market share increased from 29% to 30%. Lithography equipment supplier Nikon (OTCPK:NINOY) increased 1% while competitor Canon (CAJ) decreased 1%. The biggest gainer was deposition company Tokyo Electron (OTCPK:TOELY), which gained 4% at the expense of fellow Japanese deposition equipment supplier Ulvac, which dropped 5%.

Providing more granularity, market share growth ofAMAT and Nikon is primarily attributed to the investments by BOE in its 10.5G LCD. Both equipment companies are the only suppliers of equipment (AMAT for deposition and Nikon for lithography) that can fabricate the large 10.5G panels. So even though AMAT is a deposition company, its tool, acquired about 20 years ago from the acquisition of AKT, is the only one on the market big enough to accommodate 10.5G panels.

The display market can be segmented into three general segments – (1) LCD panels for TVs, (2) OLED panels for smartphones, and (3) LCD panels for Smartphones. Each of these has its own headwinds and tailwinds, which are impacting capital equipment expenditures. These issues I detail below. There are numerous ways to segment this industry, but I am detailing this segmentation for this article.

A driving force for 10.5G plant construction is that a 10.5G mother glass is 1.8 times larger than an 8.5G one in area and can be cut into six 75-inch panels. In comparison, a 7.5G glass substrate can be cut into only two 75-inch TV panels. Thus, there is a significant cost benefit of moving to the larger substrates.

AMAT’s deposition tools are used to form the backplane for LCD displays. The company’s deposition tools are the only ones capable of uniform coating of panels this size, which measure 3370mm x 2940mm. AMAT’s equipment can deposit various materials for the backplane.

Shown in Table 1 are the number of 10.5G panels being manufactured through 2018, with forecasts for panel production in 2019 and 2020, according to The Information Network’s report “OLED and LCD Markets: Technology, Directions and Market Analysis.”

10.5G represented a strong tailwind for AMAT and Nikon in 2018. For example, Nikon sold 13, 10.5G lithography systems in CY2018 representing 18% of systems sold. This compares to only one 10.5G system sold in CY2017.

BOE Technology’s first 10.5G fab, located in Hefei, entered volume production in the first half of 2018. China Star Optoelectronics Technology (CSOT) plans to build to kick off commercial operations of its 10.5G plant in March 2019, having installed equipment in 2018. Capex spends by these companies for these plants provided a significant portion of AMAT"s revenues for 2018.

For 2019, BOE’s second 10.5G line, to be located in Wuhan, is slated for volume production in 2020, with equipment installation in mid-2019. Sharp (OTCPK:SHCAY) will start equipment install at its new 10.5G LCD plant in Guangzhou in early 2019, with plans to kick off the first phase of the facility in Aug 2019 and to begin volume production in October 2019. LG Display (LPL) is building its 10.5G OLED P10 fab in Paju, Korea, but volume production is now scheduled at the beginning of 2021. Originally, the company planned to install equipment in 3Q 2018, but it may be pushed back to the beginning of 2020. With an oversupply of 10.5G panels as a result of BOE and CSOT production, display manufacturers are closely monitoring the market.

In addition to 10.5G mother glass for TVs, most LCD TVs are made using 8G glass. In 2018, LCD panel shipments increased 9% while TV area increased 11%, meaning that the average size of a TV is increasing. While some of the increase was due to shipments from BOE’s 10.5G plant, 8G plants were responsible for most of the growth. LG Display, for example, which makes LCD TVs from 8G mother glass, witnessed a 21% increase in area shipments, whereas Innolux, also without a 10.5G plant, reported an increase of 17% in area shipments. BOE, with both 8G and 10.5G plants, reported an area shipment increase of 17%.

I am neutral on AMAT in the OLED panel for smartphones. There are two issues. One is that AMAT’s equipment used in the production of OLEDs is being supplanted by competitor’s differentiating technology.

A second factor contributing to my neutral stance for AMAT in this OLED market is a sluggish smartphone market – the largest application for 6G OLED panels. Investment was minimal in 2018 as shown in Table 3. Also tied to sluggish smartphone sales is product distinction. Rigid OLED panels are not significantly better than lower-cost LTPS-LCD panels. With the capacity built up through 2018, utilization rates averaged 60%.

Table 4 presents The Information Network’s forecast of 6G OLED panel output to 2020. Again, panel output only increased 32,000 panels per month in 2018, but is expected to increase 138,000 panels per month in 2019, followed by a more moderate growth of 121,000 panels per month in 2020.

Flexible smartphones will drive the 6G market in 2019 and 2020. Samsung Electronics (OTCPK:SSNLF) introduced its Galaxy Fold and Huawei its Mate X in February 2018. Details of the two smartphones are described here. A significant difference between the two is the display.

In addition to the two, there are several other smartphone manufacturers that will introduce foldable models in the next two years. These include Oppo, Motorola (MSI), LG, Xiaomi (OTCPK:XIACF), and even Apple (AAPL).

I am bearish for AMAT on LCD panels for smartphones. Table 2 illustrates the drop in 6G plant expansion in 2018 showing Nikon’s lithography system sales by panel generation in 2017 and 2018. 6G systems dropped from 42 units in 2017 to 18 in 2018

Although flexible OLED has been gaining market share in the smartphone market in the last few years for its thinner form factor, higher performance, and differentiating design, the high utilization rates of 90% is minimizing the need for plant expansion and resulting in an oversupply of 20% for LCDs. Combined, these contribute to a 20% discount in LCD cost per smartphone compared to a rigid OLED display. Tianma is the top supplier of LTPS TFT-LCDs for smartphones with shipments of 149 million units in 2018, an increase of 49% YoY.

High-end smartphones like Apple"s current iPhone XS and iPhone XS Max use OLED screens to deliver better image quality, faster pixel response times. The XR uses an LCD display. It is likely we will see a similar lineup in 2019 - a continuation of both the iPhone XS and XR devices, with rumors suggesting 5.8 and 6.5-inch OLED iPhones along with a 6.1-inch LCD iPhone.

AMAT capitalized on the size of its deposition tools to generate strong revenue growth in the 10.5G market. In the other segments of the display production market (6G and 8G), its deposition tools for backplane and OLED encapsulation do not offer any advantages over competitors. In fact, the company is losing share to better technology.

The primary claim for AMAT"s display tools is its size. If 6G LCD factory expansion is dropping and 10.5G factories make panels with better economies of scale than 8G factories to make TVs, then it is only a matter of time before a competitor makes equipment that can deposit the backplanes on 10.5G panels.

The upstream materials or components of the LCD panel industry mainly include liquid crystal materials, glass substrates, polarizing lenses, and backlight LEDs (or CCFL, which accounts for less than 5% of the market).

The middle reaches is the main panel factory processing and manufacturing, through the glass substrate TFT arrays and CF substrate, CF as upper and TFT self-built perfusion liquid crystal and the lower joint, and then put a polaroid, connection driver IC and control circuit board, and a backlight module assembling, eventually forming the whole piece of LCD module. The downstream is a variety of fields of application terminal-based brand, assembly manufacturers. At present, the United States, Japan, and Germany mainly focus on upstream raw materials, while South Korea, Taiwan, and the mainland mainly seek development in mid-stream panel manufacturing.

With the successive production of the high generation line in mainland China, the panel production capacity and technology level have been steadily improved, and the industrial competitiveness has been gradually enhanced. Nowadays, the panel industry is divided into three parts: South Korea, mainland China, and Taiwan, and mainland China is expected to become the no.1 in the world in 2019.

In the past decade, China’s panel display industryhas achieved leapfrog development, and the overall size of the industry has ranked among the top three in the world. Chinese mainland panel production capacity is expanding rapidly, although Japanese panel manufacturers master a large number of key technologies, gradually lose the price competitive advantage, compression panel production capacity. Panel production is concentrated in South Korea, Taiwan, and China, which is poised to become the world’s largest producer of LCD panels.

Up to 2016, BOE‘s global market share continued to increase: smartphone LCD, tablet PC display, and laptop display accounted for the world’s first market share, and display screen increased to the world’s second, while TV LCD remained the world’s third. In LCD TV panels, Chinese panel makers have accounted for 30 percent of global shipments to 77 million units, surpassing Taiwan’s 25.5 percent market share for the first time and ranking second only to South Korea.

In terms of the area of shipment, the area of board shipment of JD accounted for only 8.3% in 2015, which has been greatly increased to 13.6% in the first half of 2016, while the area of shipment of hu xing optoelectronics in the first half of 2015 was only 5.1%, which has reached 7.8% in the first half of 2016. The panel factories in mainland China are expanding their capacity at an average rate of double-digit growth and transforming it into actual shipments and areas of shipment. On the other hand, although the market share of South Korea, Japan, and Taiwan is gradually decreasing, some South Korean and Japanese manufacturers have been inclined to the large-size HD panel and AMOLED market, and the production capacity of the high-end LCD panel is further concentrated in mainland China.

Domestic LCD panel production line capacity gradually released, overlay the decline in global economic growth, lead to panel makers from 15 in the second half began, in a low profit or loss, especially small and medium-sized production line, the South Korean manufacturers take the lead in transformation strategy, closed in medium and small size panel production line, South Korea’s 19-panel production line has shut down nine, and part of the production line is to research and development purposes. Some production lines are converted to LTPS production lines through process conversion. Korean manufacturers are turning to OLED panels in a comprehensive way, while Japanese manufacturers are basically giving up the LCD panel manufacturing business and turning to the core equipment and materials side. In addition to the technical direction of the research and judgment, more is the LCD panel business orders and profits have been severely compressed, Korean and Japanese manufacturers have no desire to fight. Since many OLED technologies are still in their infancy in mainland China, it is a priority to move to high-end panels such as OLED as soon as possible. Taiwanese manufacturers have not shut down factories on a large scale, but their advantages in LCD technology and OLED technology have been slowly eroded by the mainland.

STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.STONE provides a full range of 3.5 inches to 15.1 inches of small and medium-size standard quasi TFT LCD module, LCD display, TFT display module, display industry, industrial LCD screen, under the sunlight visually highlight TFT LCD display, industrial custom TFT screen, TFT LCD screen-wide temperature, industrial TFT LCD screen, touch screen industry. The TFT LCD module is very suitable for industrial control equipment, medical instruments, POS system, electronic consumer products, vehicles, and other products.

Flat-panel displays are thin panels of glass or plastic used for electronically displaying text, images, or video. Liquid crystal displays (LCD), OLED (organic light emitting diode) and microLED displays are not quite the same; since LCD uses a liquid crystal that reacts to an electric current blocking light or allowing it to pass through the panel, whereas OLED/microLED displays consist of electroluminescent organic/inorganic materials that generate light when a current is passed through the material. LCD, OLED and microLED displays are driven using LTPS, IGZO, LTPO, and A-Si TFT transistor technologies as their backplane using ITO to supply current to the transistors and in turn to the liquid crystal or electroluminescent material. Segment and passive OLED and LCD displays do not use a backplane but use indium tin oxide (ITO), a transparent conductive material, to pass current to the electroluminescent material or liquid crystal. In LCDs, there is an even layer of liquid crystal throughout the panel whereas an OLED display has the electroluminescent material only where it is meant to light up. OLEDs, LCDs and microLEDs can be made flexible and transparent, but LCDs require a backlight because they cannot emit light on their own like OLEDs and microLEDs.

Liquid-crystal display (or LCD) is a thin, flat panel used for electronically displaying information such as text, images, and moving pictures. They are usually made of glass but they can also be made out of plastic. Some manufacturers make transparent LCD panels and special sequential color segment LCDs that have higher than usual refresh rates and an RGB backlight. The backlight is synchronized with the display so that the colors will show up as needed. The list of LCD manufacturers:

Organic light emitting diode (or OLED displays) is a thin, flat panel made of glass or plastic used for electronically displaying information such as text, images, and moving pictures. OLED panels can also take the shape of a light panel, where red, green and blue light emitting materials are stacked to create a white light panel. OLED displays can also be made transparent and/or flexible and these transparent panels are available on the market and are widely used in smartphones with under-display optical fingerprint sensors. LCD and OLED displays are available in different shapes, the most prominent of which is a circular display, which is used in smartwatches. The list of OLED display manufacturers:

MicroLED displays is an emerging flat-panel display technology consisting of arrays of microscopic LEDs forming the individual pixel elements. Like OLED, microLED offers infinite contrast ratio, but unlike OLED, microLED is immune to screen burn-in, and consumes less power while having higher light output, as it uses LEDs instead of organic electroluminescent materials, The list of MicroLED display manufacturers:

LCDs are made in a glass substrate. For OLED, the substrate can also be plastic. The size of the substrates are specified in generations, with each generation using a larger substrate. For example, a 4th generation substrate is larger in size than a 3rd generation substrate. A larger substrate allows for more panels to be cut from a single substrate, or for larger panels to be made, akin to increasing wafer sizes in the semiconductor industry.

"Samsung Display has halted local Gen-8 LCD lines: sources". THE ELEC, Korea Electronics Industry Media. August 16, 2019. Archived from the original on April 3, 2020. Retrieved December 18, 2019.

"TCL to Build World"s Largest Gen 11 LCD Panel Factory". www.businesswire.com. May 19, 2016. Archived from the original on April 2, 2018. Retrieved April 1, 2018.

"Panel Manufacturers Start to Operate Their New 8th Generation LCD Lines". 대한민국 IT포털의 중심! 이티뉴스. June 19, 2017. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"TCL"s Panel Manufacturer CSOT Commences Production of High Generation Panel Modules". www.businesswire.com. June 14, 2018. Archived from the original on June 30, 2019. Retrieved June 30, 2019.

"Business Place Information – Global Operation | SAMSUNG DISPLAY". www.samsungdisplay.com. Archived from the original on 2018-03-26. Retrieved 2018-04-01.

"Samsung Display Considering Halting Some LCD Production Lines". 비즈니스코리아 - BusinessKorea. August 16, 2019. Archived from the original on April 5, 2020. Retrieved December 19, 2019.

Herald, The Korea (July 6, 2016). "Samsung Display accelerates transition from LCD to OLED". www.koreaherald.com. Archived from the original on April 1, 2018. Retrieved April 1, 2018.

Byeonghwa, Yeon. "Business Place Information – Global Operation – SAMSUNG DISPLAY". Samsungdisplay.com. Archived from the original on 2018-03-26. Retrieved 2018-04-01.

www.wisechip.com.tw. "WiseChip History – WiseChip Semiconductor Inc". www.wisechip.com.tw. Archived from the original on 2018-02-17. Retrieved 2018-02-17.

"China"s BOE to have world"s largest TFT-LCD+AMOLED capacity in 2019". ihsmarkit.com. 2017-03-22. Archived from the original on 2019-08-16. Retrieved 2019-08-17.

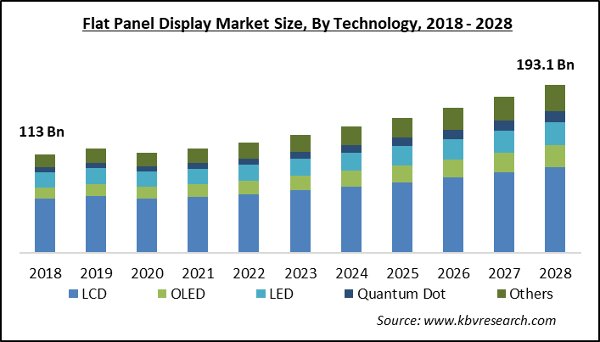

The global flat panel display market was valued at $116.80 billion in 2018, and is projected to reach $189.60 billion by 2026, registering a CAGR of 6.10% from 2019 to 2026. Flat panel display is electronics viewing technology that projects information such as images, videos, texts, or other visual material. Flat panel displays are far lighter and thinner than traditional Cathode Ray Tube (CRT) television sets. These display screens utilize numerous technologies such as Light-Emitting Diode (LED), Liquid Crystal Display (LCD), Organic Light-Emitting Diode (OLED), and others. Also, it is mostly used in consumer electronic devices such as TV, laptops, tablets, laptops, smart watches, and others.

The emergence of advanced technologies offers enhanced visualizations in several industry verticals, which include consumer electronics, retail, sports & entertainment, transportation, and others. Also, flexible flat panel display technologies witness popularity at a high pace. In addition, display technologies, such OLED, have gained increased importance in products such as televisions, smart wearables, smartphones, and other devices. Moreover, smartphone manufacturers plan to incorporate flexible OLED displays to attract consumers. Furthermore, the flat panel display market is also in the process of producing energy saving devices, primarily in wearable devices.

The major factors that drive the flat panel display market include growth in vehicle display technology in the automotive sector, increase in demand for OLED display devices in smartphones and tablets, and rise in adoption of interactive touch-based devices in the education sector. However, high cost of latest display technologies such as transparent display and quantum dot displays, and stagnant growth of desktop PCs, notebooks, and tablets hinder the flat panel display market growth. Furthermore, upcoming applications in flexible flat panel display devices are expected to create lucrative growth opportunities for the global flat panel display market.

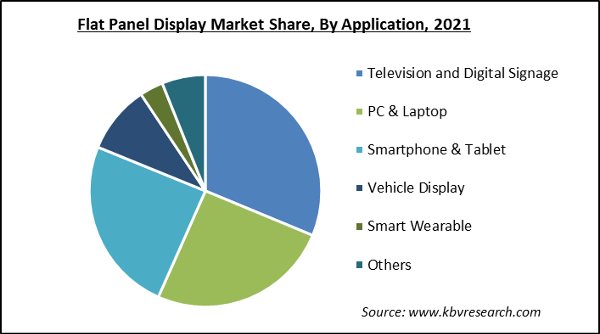

The flat panel display market is segmented into technology, application, industry vertical, and region. By technology, it is classified into OLED, quantum dots, LED, LCD, and others. By application, it is categorized into smartphone & tablet, smart wearables, television & digital signage, PC & laptop, vehicle display, and others. By industry vertical, it is divided into healthcare, retail, BFSI, military & defense, automotive, and others. Region-wise, it is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

The significant impacting factors in the global flat panel display industry include high demand for vehicle display technology in the 0automotive sector, Increase in demand for OLED display devices in smartphones and tablets, Rise in adoption of interactive touch-based devices in education sector, high cost of new display technologies, stagnant growth of desktop PCs, notebook, and tablets, surge in adoption of flexible flat panel display. Each of these factors is anticipated to have a definite impact on the flat panel display market size during the forecast period.

Organic LEDs are emerging type of display technology. This technology removes the need of separate backlighting. The display panels based on this technology are thinner than other technologies that are integrated in display devices. This technology is widely used in smartphones which boast OLED screen and are rapidly becoming more prevalent. Major player like Apple, Oppo, Vivo, LG, and Xiaomi also stared using OLED displays from last few years. In addition, when in low light ambient conditions at room, an OLED can achieve higher contrast ratio than other technology.

In recent years, the number of devices with touch sensors has risen exponentially as touch-based devices are easier to access. The touch-based devices require a display panel to operate which, in turn, helps in the growth of display devices. The demand for interactive displays in schools, institutions, and universities has increased around the world. These displays are useful for learning and teaching purposes such as efficient interaction in classrooms, student accomplishments, and overall productivity. Interactive display offers numerous advantages such as increased level of engagement between students and teachers, allowing students with physical disability learn better, bring flexibility in learning, saves teaching cost, and allows students to save lessons for further review. Also, interactive flat panel display allows teachers to share text, video, and audio files with students easily.

The latest display technologies such as transparent display and quantum dot displays are relatively high in cost due to its complex design. Hence, most of the latest display technologies are integrated in premium devices, which are not affordable. This factor is expected to restrict the flat panel display market growth.

The current flat panel display market is focused on developing new technologies and products primarily for large-sized displays and high-resolution images. The flat panel display market in future is expected to concentrate on flexible displays. Flexible displays are thin, light, and less prone to breakage compared to conventional displays. Therefore, flexible displays are expected to replace current display devices as well as create new ones. These factors are expected to create lucrative flat panel display market opportunities globally.

Key Benefits for Flat Panel Display Market:This study comprises an analytical depiction of the global flat panel display market share with current trends and future estimations to depict the imminent investment pockets.

Key Market Players AU OPTRONICS CORP., CRYSTAL DISPLAY SYSTEMS LTD, E INK HOLDINGS INC, JAPAN DISPLAY INC., LG DISPLAY, NEC CORPORATION, PANASONIC CORPORATION, SAMSUNG ELECTRONICS CO. LTD., SONY CORPORATION, SHARP CORPORATION

Westford,USA, Oct. 19, 2022 (GLOBE NEWSWIRE) -- The primary factors driving the growth of the Display Market are increasing demand from smartphone and tablet manufacturers, rising expenditure on smart Infra-Red (IR) sensors, and rapid expansion of digital media content. Smartphones are becoming more sophisticated and are using larger screens that require higher resolutions for better user experience. Tablets are also becoming increasingly popular as they offer a single device that can serve as both a computer and a mobile phone. This increase in demand for high-resolution displays is expected to drive the adoption of LED displays in the coming years.

Manufacturers in the global display market are starting to see the potential in displays as an important part of their product lines. Device manufacturers are looking for displays that can be used on a variety of devices, from laptops to smartphones and even cars. In addition, developers are creating more applications that require high-quality displays.

One key challenge facing manufacturers is making sure that their displays meet the requirements of multiple market segments. They need to make sure that their displays are suitable for usage on tablets as well as laptops, yet they also need to create displays that look good on smaller devices like smartphones and digital assistants.

The growth in demand for display market across various verticals such as healthcare, retail, automotive, appliance and others has led to an increasing demand for large sizes screens which can be cost effective owing to their mass production capabilities. Display manufacturers are also exploring new technologies such as flexible displays that can be rolled up like a traditional newspaper

Our report considers several factors such as market size estimation techniques, product segmentation analysis, expenditure Breakdown by Country and region; Porter"s Five Forces Analysis; and price trends analysis to give you a comprehensive view of the global display market.

Some of the key players in the global display market include LG Display Co., Ltd., Samsung Electronics Co., Ltd., and Sharp Corporation. These companies are focused on developing innovative products that meet the needs of various consumers in the marketplace. They also strive to improve their competitiveness by expanding their product lines into new markets and by creating partnerships with other companies to share technology and manufacturing resources.

Among global display market leaders, Samsung is presently dominating the industry with a share of 38% of the market. However, Apple is looming large as one of the largest competitors in smartphone sector. Other prominent players in this segment include LG Display, Sony Corp, and Toshiba Corporation. Among these companies, LG Display has been fastest expanding its business over recent years owing to its focus on emerging markets such as China and India.

For one, it"s heavily invested in research and development in the display market. According to analysts at SkyQuest, Samsung spends more than $13.7 billion a year on R&D, more than any other company in the world. That investment has paid off: The company"s displays are consistently among the best on the market.

Samsung also makes good use of its deep pockets. The company has poured money into forming joint ventures with major chipmakers like Qualcomm and Intel, which allows it to quickly bring new technologies to market. It doesn"t just rely on partnerships; Samsung also invests in its own technology centers, such as the foundry that produces screens for its smartphones.

One important technology that Samsung is investing in is AMOLED and QLED screens. QLEDs are generally considered to be more environmentally friendly than LCDs, since they use less power and create fewer byproducts.

The main drivers for Samsung"s strong performance in the display market are its diversification across product lines, continuous innovation across product categories, and excellent execution capabilities. The company has been able to expand into new markets such as automotive displays and smart watches, while continuing to focus on profitable core products.

Samsung has also been successful in pushing down prices for OLED displays over the past few years. This has made OLED panels more accessible to a wider range of customers, supporting growth at rival companies such as LG Electronics and Sony.

In recent years, there has been a shift in display technology as manufacturers across the global display market experiment with new and more innovative ways to create displays. The trend observed by SkyQuest worldwide is that display technologies are moving towards OLEDs and quantum dots, both of which have a number of advantages.

Quantum dots or QLED offer many advantages over traditional LCDs in the display market, such as better color reproduction, enhanced viewing angles, better response time, and lower power consumption. Their small size also makes them ideal for applications where sliding or tilting LCD panels are not possible or desirable. Quantum dot displays have already begun appearing in consumer electronics and will eventually replace traditional LCDs as the predominant type of display in devices like smartphones and tablets.

SkyQuest Technology is leading growth consulting firm providing market intelligence, commercialization and technology services. It has 450+ happy clients globally.

The global TFT-LCD display panel market attained a value of USD 181.67 billion in 2022. It is expected to grow further in the forecast period of 2023-2028 with a CAGR of 5.2% and is projected to reach a value of USD 246.25 billion by 2028.

The current global TFT-LCD display panel market is driven by the increasing demand for flat panel TVs, good quality smartphones, tablets, and vehicle monitoring systems along with the growing gaming industry. The global display market is dominated by the flat panel display with TFT-LCD display panel being the most popular flat panel type and is being driven by strong demand from emerging economies, especially those in Asia Pacific like India, China, Korea, and Taiwan, among others. The rising demand for consumer electronics like LCD TVs, PCs, laptops, SLR cameras, navigation equipment and others have been aiding the growth of the industry.

TFT-LCD display panel is a type of liquid crystal display where each pixel is attached to a thin film transistor. Since the early 2000s, all LCD computer screens are TFT as they have a better response time and improved colour quality. With favourable properties like being light weight, slim, high in resolution and low in power consumption, they are in high demand in almost all sectors where displays are needed. Even with their larger dimensions, TFT-LCD display panel are more feasible as they can be viewed from a wider angle, are not susceptible to reflection and are lighter weight than traditional CRT TVs.

The global TFT-LCD display panel market is being driven by the growing household demand for average and large-sized flat panel TVs as well as a growing demand for slim, high-resolution smart phones with large screens. The rising demand for portable and small-sized tablets in the educational and commercial sectors has also been aiding the TFT-LCD display panel market growth. Increasing demand for automotive displays, a growing gaming industry and the emerging popularity of 3D cinema, are all major drivers for the market. Despite the concerns about an over-supply in the market, the shipments of large TFT-LCD display panel again rose in 2020.

North America is the largest market for TFT-LCD display panel, with over one-third of the global share. It is followed closely by the Asia-Pacific region, where countries like India, China, Korea, and Taiwan are significant emerging market for TFT-LCD display panels. China and India are among the fastest growing markets in the region. The growth of the demand in these regions have been assisted by the growth in their economy, a rise in disposable incomes and an increasing demand for consumer electronics.

The report gives a detailed analysis of the following key players in the global TFT-LCD display panel Market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

Display glass substrate is a special glass used for supporting TFT (Thin Film Transistor), LCD (Liquid Crystal Display) and OLED panels forming display units for products including televisions, personal computers and mobile phones. Ever display panel consists of various components stacked in a number of layers, which includes a color filter, a polarizer and a liquid crystal display with the glass substrate being the most important.

In 2016, the display glass substrate market was valued at US$ 1.42 Billion and is projected to reach US$ 1.97 Billion by 2028, growing at a CAGR of 5.7%. With the expanding demand for consumer grade electronic devices such as smartphones, laptops and personal computers, the global display glass substrate market is expected to grow during the forecast period.

The expanding use of LCD’s in smart handheld devices, consumer durables, and other automotive applications is one of the most powerful factors projected to drive the growth of the display glass substrate market. Moreover, the advancements in the electronics and semiconductor industries are further projected to drive the increasing demand for display glass substrates.

The electronics industry is the largest end-using commerce segment that suitably utilizes display glass substrates and the general growth for the display glass substrate market is heavily dependent on it. Increasing in manufacturing of display devices, electronic components, semiconductor devices, MEMS (Microelectronic Mechanical System) devices, and computing & telecommunication devices is expected to drive the growth of the display glass substrate market.

However, the immense manufacturing cost of display glass substrates acts as a restraint to the expansion of the display glass substrate market. Manufacturers of display glass substrates are focusing on directing their earnings through several process control techniques with the aim of optimizing production costs to a certain level.

Asia Pacific is accredited to be the largest market for display glass substrates. The display glass substrate market in the Asia Pacific region is estimated to grow at the highest CAGR during the forecast period owing to the occupancy of numerous electronics manufacturers in this region.

China, Hong Kong and South Korea are expected to account for the largest share of the glass substrate market in the Asia Pacific region in 2028 as most of the major producers of display glass substrates such as Nippon Sheet Glass (Japan) and The Tungshu Group (China) are located in the Asia Pacific region. The Asia Pacific region accounts for over 37% of the total display glass substrate market. Other regions include North America and Europe with a market share of 8% and 3% in the global display glass substrate market.

Some of the key players in the global display glass substrate market are Corning Incorporated, LG Chem, AGC Incorporated, AvanStrate Incorporated, SCHOTT Ag, Tungshu Optoelectronics, IRICO Group New Energy Company Limited and CGC Glass.

The research report presents a comprehensive assessment of the display glass substrate market and contains thoughtful insights, facts, historical data and statistically supported and industry validated market data. It also includes projections using a suitable set of assumptions and methodologies. The research report of display glass substrate market provides analysis and information according to the different market segments such as geographies, grade type and application.

The display glass substrate market report is a compilation of first-hand information, qualitative and competitive assessment industry analysts, inputs from industry experts and industry participants across the value chain. The report for display glass substrate market provides an in depth analysis of parent market trends, macro-economic indicators and governing factors along with market attractiveness as per segments. The report also maps the qualitative impact of various market factors on market segments and geographies.

The Global Flexible Displays Market size is expected to reach $31.5 billion by 2025, rising at a market growth of 25.9% CAGR during the forecast period. Flexible displays are mainly OLED and AMOLED displays that are curved, bended, or fully foldable. Consumer electronics manufacturers have offered numerous smartphones, TV sets and other display devices in a rigid curved form factor in the current market scenario. Although these displays are curved in comparison to traditional rigid flat displays, these displays do not give the end-users true versatility.

Growth is driven by increased demand for display-based consumer electronics coupled with consumer inclination towards energy-efficient, flexible gadgets. Technological advances in display technology have resulted in the introduction of advanced flexible displays, creating opportunities for growth for the market"s key players. In terms of portability, non-fragility and weight, the superior features offered by flexible displays make them an attractive option for consumer electronics manufacturers. In addition, the adoption of flexible displays based on Organic Light Emitting Diode (OLED) is experiencing exponential growth in high-definition content and high-performance applications. In addition, market demand is propelled by high growth in the smart wearable market.

Based on Type, the market is segmented into OLED and Others. Based on Application, the market is segmented into Smartphone, Smart Wearbles, TV, E-reader, Automotive & Transportation and Others. The segment of smartphones and tablets was the largest market share in 2018. Smartphones have LED-LCD and OLED-based display panels, tablets are extended shape of smartphone and are mainly equipped with LED-LCD display panels. Due to the high demand on the consumer market, various smartphone and laptop manufacturers and suppliers have reached the tablet market. These are made more durable by using flexible displays in smartphones and tablets, as they provide sleek designs and better ergonomics to operate these devices. Based on Material Type, the market is segmented into Plastic, Glass and Others.

Based on Regions, the market is segmented into North America, Europe, Asia Pacific, and Latin America, Middle East & Africa. The presence of a large number of consumer electronics manufacturers and massive customer base is boosting the regional demand for flexible displays. Countries like Japan, South Korea, China, and India are the leaders in flexible display growth. China is the world"s largest producer of flexible OLED displays.

The major strategies followed by the market participants are Product launches and Partnerships & Collaborations. Based on the Analysis presented in the Cardinal matrix, Samsung Electronics Co., Ltd. (Samsung Group) and LG Corporation are some of the forerunners in the Flexible Display Market. The market research report covers the analysis of key stake holders of the market. Key companies profiled in the report include LG Display Co., Ltd. (LG Corporation), Samsung Electronics Co., Ltd. (Samsung Group), AU Optronics Corporation, Corning, Inc., Sharp Corporation, Kateeva, Inc., BOE Technology Group Co., Ltd., Royole Corporation, E Ink Holdings, Inc. and Visionox Technology, Inc.

Dec-2018: Royole partnered with Airbus in order to develop aircraft-cabin applications. In this partnership, both the companies will investigate the commercial opportunities and use of sensors and flexible displays on passenger aircraft.

Dec-2018: Visionox Technology and IDEX Biometrics collaborated on exploring the development of next-generation IDEX’s unique off-chip biometric sensors for smart cards that uses Visionox’s flexible LTPS TFT backplane technology. The collaboration is focused towards the development of feature-rich and cost-effective smart card systems supporting both biometric and display technologies.

Oct-2018: Visionox Technology teamed up with Hefei municipal government for constructing the factory that can produce 30,000 substrates per month. These substrates will be used in sixth-generation active matrix organic light emitting diode displays. Both are thinking of establishing a Joint Venture for building and operating the plant.

Apr-2019: LG Display acquired DuPont"s OLED business as well as its R&D and production facilities. The OLED technology uses an inkjet printing method for adding a soluble material to a panel, thus producing the high-performing displays in an economical manner and reducing the material waste.

Nov-2019: Visionox Technology announced the launch of a foldable clamshell smartphone and a rollable OLED panel hinting, two foldable clamshell prototype. The 6.47" big AMOLED display has been used for this prototype with on-cell technology.

May-2019: Corning announced the launch of Corning® Astra(TM) Glass, a new glass substrate optimized for mid-to-large size; immersive displays in notebooks, high-performance tablets, and 8K TVs. This glass has been engineered to enable the higher-pixel density of high-performance displays, which are required by panel makers in order to meet the customer demand for faster, brighter, and more lifelike images.

Apr-2019: Sharp unveiled organic light-emitting diode panels for foldable smartphones. This display has foldable 6.18-inch OLED screen, which can be folded 3, 00,000 times without any damage. The new OLED panels will be produced at Company"s display factory in Sakai.

Feb-2019: Sharp introduced four new models of its 4K Ultra-HD resolution commercial LCD display line. These displays will be ideal for business, retail, and hospitality sectors. This helps the customers to see subtler textures and finer details in photos and videos.

Jan-2019: Samsung Display introduced its first 15.6-inch OLED panel for the notebook market. This panel delivers brighter colors and deeper blacks over 4K LCD-based screens.

Oct-2018: Royole introduced the Royole FlexPai, a commercial foldable smartphone, a combination of tablet and mobile phone with flexible screen. This smartphone is based upon Royole"s Flexible+ platform; this can be easily combined into a number of products and applications across different industries.

Aug-2018: Samsung extended its curved display line-up with the launch of new CJ79 (Model name: C34J791) monitor. This monitor has the feature of Intel’s Thunderbolt™ 3 connectivity and is designed for business and creative audiences that are seeking efficient and comfortable work experience through powerful connectivity.

Sep-2018: Sharp expanded its reach to Asia Pacific region by launching 70X500E, its 8K professional display panel in India. This panel was incorporated with Sharp"s wealth of Ultra-High-Resolution Monitor technologies for high brightness and wide color gamut.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey