lcd panel market share 2017 made in china

Download "Maeil Business Pulse" from Google Play or App Store for access to up-to-the-minute and around-the-clock news on Korean economy, business, finances, and market-moving topics.

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved December 22, 2022, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed December 22, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: December 22, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited December 22, 2022)

This statistic shows the sales volume share of the TV manufacturers in China from 2017 to 2019. During the measured time period, the market leading Xiaomi held a shipment share of 19.3 percent in China, ahead of more traditional TV makers such as Hisense and Skyworth.Read moreTV sales volume market share in China from 2017 to 2019, by manufacturerCharacteristicXiaomiHisenseSkyworthTCLChanghongHaierKonkaSonyCoocaaSharpPhilipsSamsungOthers--------------

In 2017, Samsung was the market leader of LCD TV manufacturing in terms of its share of global shipments. The South Korean company held over 20 percent of worldwide LCD shipments in 2017, eight percent more than the share of its closest competitor, LG Electronics. As a result of Samsung’s continued success in this market, as well as its significant share in the smartphone market, the company’s global revenue exceeded 200 billion U.S. dollars for the first time in 2013.

Although Sony remains one of the largest LCD manufacturers, it has lost its market share more than halve from 13.7 percent in 2008 to 5.6 percent in 2017. Yet LCD TVs remain a key segment, which was the second largest sector for Sony in its consumer electronics business segment.

Sales of LCD TVs worldwide were worth 106 billion U.S. dollars in 2016 and projected to fall to 102 billion dollars by 2017. Asia/Pacific was the largest market for LCDs as over 74 million units were expected to be sold in the region in 2013 in which China alone accounted for 42.5 million of these units. This means that almost 20 percent of LCD TVs sold worldwide throughout the year took place in China. North America was the second largest market for LCDs as 41.8 million units were sold there in 2013, 33.7 million of which were purchased in the United States.

TCL. (May 4, 2020). TV sales volume market share in China from 2017 to 2019, by manufacturer [Graph]. In Statista. Retrieved December 22, 2022, from https://www.statista.com/statistics/858405/china-market-share-of-lcd-tv-brands/

TCL. "TV sales volume market share in China from 2017 to 2019, by manufacturer." Chart. May 4, 2020. Statista. Accessed December 22, 2022. https://www.statista.com/statistics/858405/china-market-share-of-lcd-tv-brands/

TCL. (2020). TV sales volume market share in China from 2017 to 2019, by manufacturer. Statista. Statista Inc.. Accessed: December 22, 2022. https://www.statista.com/statistics/858405/china-market-share-of-lcd-tv-brands/

TCL. "Tv Sales Volume Market Share in China from 2017 to 2019, by Manufacturer." Statista, Statista Inc., 4 May 2020, https://www.statista.com/statistics/858405/china-market-share-of-lcd-tv-brands/

TCL, TV sales volume market share in China from 2017 to 2019, by manufacturer Statista, https://www.statista.com/statistics/858405/china-market-share-of-lcd-tv-brands/ (last visited December 22, 2022)

LG Display and Samsung Display are struggling to find their ways out of the deterioration of their performance even after withdrawing from production of liquid crystal display (LCD) panels. The high-priced organic light emitting diode (OLED) panel sector regarded as a future growth engine is not growing fast due to the economic downturn. Even in the OLED panel sector, Chinese display makers are within striking distance of Korean display makers, experts say.

On Aug. 30, Display Supply Chain Consultants (DSCC), a market research company, predicted that LCD TV panel prices hit an all-time low in August and that an L-shaped recession will continue in the fourth quarter. According to DSCC, the average price of a 65-inch ultra-high-definition (UHD) panel in August was only US$109, a 62 percent drop from the highest price of US$288 recorded in July in 2021. The average price of a 75-inch UHD panel was only US$218, which was only about half of the highest price of US$410 in July last year. DSCC predicted that the average panel price in the third quarter will fall by 15.7 percent. As Chinese companies’ price war and the effect of stagnation in consumption overlapped, the more LCD panels display makers produce, the more loss they suffer.

As panel prices fell, manufacturers responded by lowering facility utilization rates. DSCC said that the LCD factory utilization rate descended from 87 percent in April to 83 percent in May, 73 percent in June, and 70 percent in July.

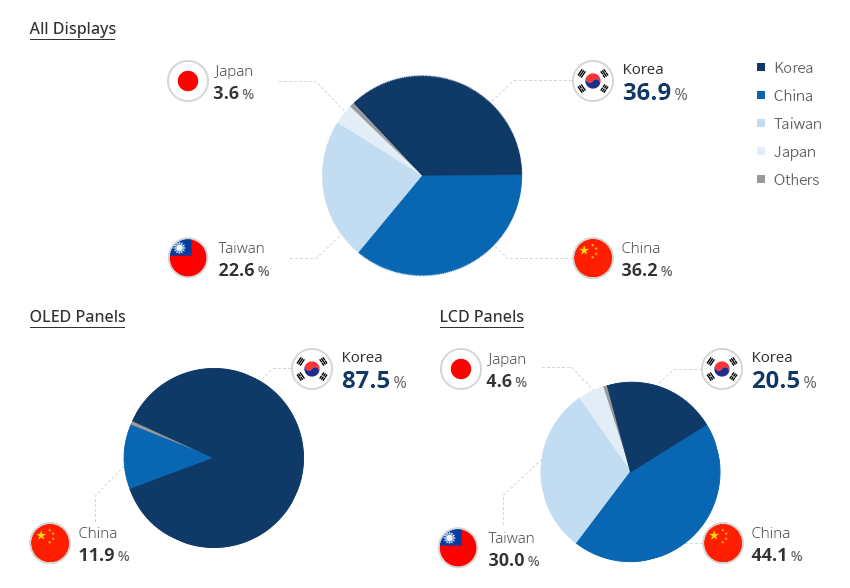

Now that the LCD panel business has become no longer lucrative, Korean display makers have shut down their LCD business or shrunk their sizes. In the LCD sector, China has outpaced Korea since 2018. China’s LCD market share reached 50.9 percent in 2021, while that of Korea dropped to 14.4 percent, lower than Taiwan’s 31.6 percent.

Samsung Display already announced its withdrawal from the LCD business in June. Only 10 years have passed since the company was spun off from Samsung Electronics in 2012. LG Display has decided to halt domestic LCD TV panel production until 2023 and reorganize its business structure centering on OLED panels. Its Chinese LCD production line will be gradually converted to produce LCD panels for IT or commercial products. TrendForce predicted that LG Display will stop operating its P7 Plant in the first quarter of next year.

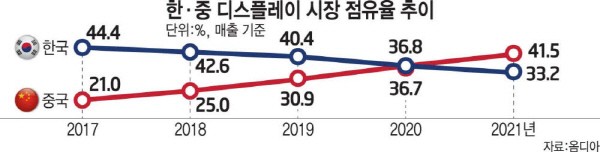

Korean display makers’ waning LCD business led to a situation in which Korea even lost first place in the display industry. Korea with a display market share of 33.2 percent was already overtaken by China with 41.5 percent) in 2021 according to market researcher Omdia and the Korea Display Industry Association. Korea’s market share has never rebounded in for five years since 2017 amid the Korean government’s neglect. Seventeen years have passed since 2004 when Korea overtook Japan to rise to the top of the world in the LCD industry. Korea’s LCD exports amounted to more than US$30 billion in 2014, but fell to US$21.4 billion last year.

A bigger problem is that Korean display makers may lose its leadership in the OLED panel sector although it is still standing at the top spot. While Korea’s OLED market share fell from 98.1 percent in 2016 to 82.8 percent last year, that of China rose from 1.1 percent to 16.6 percent. Considering that the high-end TV market is highly likely to shrink for the time being due to a full-fledged global consumption contraction, some analysts say that the technology gap between Korea and China can be sharply narrowed through this looming TV market slump. According to industry sources, the Chinese government is now focusing on giving subsidies to the development of OLED panel technology rather LCD technology. On the other hand, in Korea, displays were also wiped out from national strategic technology industry items under the Restriction of Special Taxation Act which can receive tax benefits for R&D activities on displays.

TOKYO -- In the past two years, eight plants have been set up in China to produce smartphone panels. Five more are scheduled to start operating in the next two years.

Backed by massive state funding, Chinese panel makers are taking a bigger bite of the market for smartphone display panels, which has so far been dominated by Japanese and South Koreans makers.

It is the first time that China took over the No. 1 spot in the display market, which Korea has always been a leader in. The title of “the strongest country in display market” is lost after 17 years. It would not be possible to reclaim the No. 1 spot if Korea cannot find a way to expand investment in next-generation displays such as organic light emitting diodes (OLED).

According to market research firm Omdia, China recorded $64.8 billion in sales including LCD and OLED in the global display market last year. China took over Korea’s No. 1 spot with a market share of 41.5%. Korea"s market share fell 8.3 points (p) to 33.2%. This is the first time since 2004, in 17 years, that Korea had to hand over the No. 1 spot. Korea had a 9.4 p advantage in market share over China up until 2019.

China overtook Korea and seized power in the LCD market by offering a low-priced products. BOE, China"s largest panel manufacturer, has become the world"s largest LCD manufacturer with help of the subsidy from the Chinese government. LCD sales was $28.6 billion last year, accounting for 26.3% of the total LCD market. The sales of Chinese companies such as BOE, CSOT, Tianma, and Visionox increased significantly as demand for TV and information technology (IT) devices increased with the prolonged COVID 19 and increased price of LCD panel.

After taken over in the LCD market, Korea is focusing on the highly-valued OLED market. Samsung Display and LG Display are transforming their LCD production lines to OLED. Korea is the No. 1 with 82.3% of the global OLED market shares according to Omdia, and China’s market share only accounts for16.6%.

China"s dominance is expected to continue for some time because the large display market such as TVs and laptops still depends on LCD. Only when Korea starts to reduce OLED panel prices by mass producing OLED, then Korea can replace the LCD market led by China.

China has also started to narrow the gap with Korea in OLED industry. BOE and other companies have commercialized OLED for small and medium-sized displays such as mobile, laptop, and tablet. Following LCD market, China is threatening Korea in OLED market as well as China expands OLED market share mainly in the Chinese smartphone market.

Critics are pointing out that Korea needs to expand in OLED market and develop new technologies in order to maintain the OLED gap with China. Korea must take control over the large TV panel market, which has a large technological gap with China, and create a new form factor with new technologies such as flexible, rollable, and bendable panels.

An official from the display industry said, “With the government-led industrial promotion policy and copious domestic market, China is making an effort to solidify its leading position in the display industry. There is a neglect on display industry in Korea since the display promotion policy is almost non-existent compared to semiconductors and batteries.”

Chinese display manufacturers are chasing their South Korean rivals closely by planning to release a larger volume of liquid-crystal panels over 32 inches this year, said a market researcher Sunday.

According to a report on the 2017 shipment strategies of Chinese TV panel makers by IHS Markit, Chinese LCD panel suppliers are forecast to ship out a total of 320,000 large-size panels larger than 32 inches by the end of this year, a 33 percent surge from last year.

In the report, Wu mentioned the plans of major Chinese panel firms such as BOE, CSOT, CEC-Panda and HKC to focus on expanding production of 43, 55 and 58-inch panels, adding that demand for 32-inch panels will gradually decrease.

“By the end of 2018, China will be the largest region for TFT LCD capacity, and larger-sized products may make their factories more efficient and profitable than they have been when producing 32-inch panels,” he said.

The strategy shift of the Chinese players suggests that they might outstrip Korean display makers in the global large-size display market, the analyst said.

“The strategies of Chinese panel makers will significantly influence global supply and demand,” Wu said. “In 2015 and 2016, the Chinese companies shipped 33.2 percent of worldwide LCD TV panel, trailing only Korean panel makers at 36.4 percent.”

The competition structure has been advantageous for the Korean players, since their Chinese rivals had been focusing on small LCD panels until last year. But now the Korean firms are facing fiercer competition in prices.

Although demand for organic-light emitting diode panels in the TV market is gradually rising, dominance of LCD panels is projected to continue for the foreseeable future.

“While OLEDs are expected to post sharp growth, they will not be able to usurp LCD as the panels of choice for upper-end TVs,” another report by IHS Markit said.

[Introduction]: This paper analyzes the competitive pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes.

Since April 2020, the display device sector rose 4.81%, ranking 11th in the electronic subsectors, 3.39 percentage points behind the SW electronic sector, 0.65 percentage points ahead of the Shanghai and Shenzhen 300 Index. Of the top two domestic panel display companies, TCL Technology is up 11.35 percent in April and BOE is up 4.85 percent.

Specific to the panel display plate, we still do the analysis from both ends of supply and demand: supply-side: February operating rate is insufficient, especially panel display module segment grain rate is not good, limited capacity to boost the panel display price. Since March, effective progress has been made in the prevention and control of the epidemic in China. Except for some production lines in Wuhan that have been delayed, other domestic panels show that the production lines have returned to normal. In South Korea, Samsung announced recently that it would accelerate its withdrawal from all LCD production lines. This round of output withdrawal exceeded market expectations both in terms of pace and amplitude. We will make a detailed analysis of it in Chapter 2.

Demand-side: We believe that people spend more time at home under the epidemic situation, and TV, as an important facility for family entertainment, has strong demand resilience. In our preliminary report, we have interpreted the pick-up trend of domestic TV market demand in February, which also showed a good performance in March. At present, the online market in China maintains a year-on-year growth of about 30% every week, while the offline market is still weak, but its proportion has been greatly reduced. At present, people are more concerned about the impact of the epidemic overseas. According to the research of Cinda Electronics Industry Chain, in the first week, after Italy was closed down, local TV sales dropped by about 45% from the previous week. In addition, Media Markt, Europe’s largest offline consumer electronics chain, also closed in mid-March, which will affect terminal sales to some extent, and panel display prices will continue to be under pressure in April and May. However, we believe that as the epidemic is brought under control, overseas market demand is expected to return to the pace of China’s recovery.

From a price perspective, the panel shows that prices have risen every month through March since the bottom of December 19 reversed. However, according to AVC’s price bulletin of TV panel display in early April, the price of TV panel display in April will decrease slightly, and the price of 32 “, 39.5 “, 43 “, 50 “and 55” panels will all decrease by 1 USD.65 “panel shows price down $2; The 75 “panel shows the price down by $3.The specific reasons have been described above, along with the domestic panel display production line stalling rate recovery, supply-side capacity release; The epidemic spread rapidly in Europe and the United States, sports events were postponed, local blockades were gradually rolled out, and the demand side declined to a certain extent.

Looking ahead to Q2, we think prices will remain under pressure in May, but prices are expected to pick up in June as Samsung’s capacity is being taken out and the outbreak is under control overseas. At the same time, from the perspective of channel inventory, the current all-channel inventory, including the inventory of all panel display factories, has fallen to a historical low. The industry as a whole has more flexibility to cope with market uncertainties. At the same time, low inventory is also the next epidemic warming panel show price foreshadowing.

In terms of valuation level, due to the low concentration and fierce competition in the panel display industry in the past ten years, the performance of sector companies is cyclical to a certain extent. Therefore, PE, PB, and other methods should be comprehensively adopted for valuation. On the other hand, the domestic panel shows that the leading companies in the past years have sustained large-scale capital investment, high depreciation, and a long period of poor profitability, leading to the inflated TTM PE in the first half of 2014 to 2017. Therefore, we will display the valuation level of the sector mainly through the PB-band analysis panel in this paper.

In 2017, due to the combined impact of panel display price rise and OLED production, the valuation of the plate continued to expand, with the highest PB reaching 2.8 times. Then, with the price falling, the panel shows that PB bottomed out at the end of January 2019 at only 1.11 times. From the end of 2019 to February, the panel shows that rising prices have driven PB all the way up, the peak PB reached 2.23 times. Since entering March, affected by the epidemic, in the short term panel prices under pressure, the valuation of the plate once again fell back to 1.62 times. In April, the epidemic situation in the epidemic country was gradually under control, and the valuation of the sector rebounded to 1.68 times.

We believe the sector is still at the bottom of the stage as Samsung accelerates its exit from LCD capacity and industry inventories remain low. Therefore, once the overseas epidemic is under control and the domestic demand picks up, the panel shows that prices will rise sharply. In addition, the plate will also benefit from Ultra HD drive in the long term. Panel display plate medium – and long-term growth logic is still clear. Coupled with the optimization of the competitive pattern, industry volatility will be greatly weakened. The current plate PB compared to the historical high has sufficient space, optimistic about the plate leading company’s investment value.

1). share market, in April in addition to Zhiyun shares, Tiantong shares, Yizhi technology fell, the rest of the stock plate rose, precision test electronics, Lebao high-tech and TCL technology rose larger, reaching 22.38%, 11.45%, and 11.35% respectively.

In the overseas market, benefiting from the control of the epidemic in Japan and South Korea, all stocks except UDC rose. Among them, Innolux Optoelectronics, Finetek, AU Optoelectronics rose more than 10%.

Revenue at Innolux and AU Optronics has been sluggish for several months and improved in March. Since the third quarter of 2017, Innolux’s monthly revenue growth has been negative, while AU Optronics has only experienced revenue growth in a very few months.AU Optronics recorded a record low revenue in January and increased in February and March. Innolux’s revenue returned to growth in March after falling to its lowest in recent years in February. However, because the panel display manufacturers in Taiwan have not put in new production capacity for many years, the production process of the existing production line is relatively backward, and the competitiveness is not strong.

On March 31, Samsung Display China officially sent a notice to customers, deciding to terminate the supply of all LCD products by the end of 2020.LGD had earlier announced that it would close its local LCDTV panel display production by the end of this year. In the following, we will analyze the impact of the accelerated introduction of the Korean factory on the supply pattern of the panel display industry from the perspective of the supply side.

The early market on the panel display plate is controversial, mainly worried about the exit of Korean manufacturers, such as LCD display panel price rise, or will slow down the pace of capacity exit as in 17 years. And we believe that this round of LCD panel prices and 2017 prices are essentially different, the LCD production capacity of South Korean manufacturers exit is an established strategy, will not be transferred because of price warming. Investigating the reasons, we believe that there are mainly the following three factors driving:

(1) Under the localization, scale effect, and aggregation effect, the Chinese panel leader has lower cost and stronger profitability than the Japanese and Korean manufacturers. In terms of cost structure, according to IHS data, material cost accounts for 70% of the cost displayed by the LCD panel, while depreciation accounts for 17%, so the material cost has a significant impact on it. At present, the upstream LCD, polarizer, PCB, mold, and key target material line of the mainland panel display manufacturers are fully imported into the domestic, effectively reducing the material cost. In addition, at the beginning of the factory, manufacturers not only consider the upstream glass and polarizer factory but also consider the synergy between the downstream complete machine factory, so as to reduce the labor cost, transportation cost, etc., forming a certain industrial clustering effect. The growing volume of shipments also makes the economies of scale increasingly obvious. In the long run, the profit gap between the South Korean plant and the mainland plant will become even wider.

(2) The 7 and 8 generation production lines of the Korean plant cannot adapt to the increasing demand for TV in average size. Traditionally, the 8 generation line can only cut the 32 “, 46 “, and 60” panel displays. In order to cut the other size panel displays economically and effectively, the panel display factory has made small adjustments to the 8 generation line size, so there are the 8.5, 8.6, 8.6+, and 8.7 generation lines. But from the cutting scheme, 55 inches and above the size of the panel display only part of the generation can support, and the production efficiency is low, hindering the development of large size TV. Driven by the strong demand for large-size TV, the panel display generation line is also constantly breaking through. In 2018, BOE put into operation the world’s first 10.5 generation line, the Hefei B9 plant, with a designed capacity of 120K/ month. The birth of the 10.5 generation line is epoch-making. It solves the cutting problem of large-size panel displays and lays the foundation for the outbreak of large-size TV. From the cutting method, one 10.5 generation line panel display can effectively cut 18 43 inches, 8 65 inches, 6 75 inches panel display, and can be more efficient in hybrid mode cutting, with half of the panel display 65 inches, the other half of the panel display 75 inches, the yield is also guaranteed. Currently, there are a total of five 10.5 generation lines in the world, including two for domestic panel display companies BOE and Huaxing Optoelectronics. Sharp has a 10.5 generation line in Guangzhou, which is mainly used to produce its own TV. Korean manufacturers do not have the 10.5 generation line. In the context of the increasing size of the TV, Korean manufacturers are obviously at a disadvantage in competitiveness.

(3) As the large-size OLED panel display technology has become increasingly mature, Samsung and LGD hope to transfer production to large-size OLED with better profit prospects as soon as possible. Apart from the price factor, the reason why South Korean manufacturers are exiting LCD production is more because the large-size OLED panel display technology is becoming mature, and Samsung and LGD hope to switch to large-size OLED production as soon as possible, which has better profit prospects. At present, there are three major large-scale OLED solutions including WOLED, QD OLED, and printed OLED, while there is only WOLED with a mass production line at present.

According to statistics, shipments of OLED TVs totaled 2.8 million in 2018 and increased to 3.5 million in 2019, up 25 percent year on year. But it accounted for only 1.58% of global shipments. The capacity gap has greatly limited the volume of OLED TV.LG alone consumes about 47% of the world’s OLED TV panel display capacity, thanks to its own capacity. Other manufacturers can only purchase at a high price. According to the industry chain survey, the current price of a 65-inch OLED panel is around $800-900, while the price of the same size LCD panel is currently only $171.There is a significant price difference between the two.

Samsung and LGD began to shut down LCD production lines in Q3 last year, leading to the recovery of the panel display sector. Entering 2020, the two major South Korean plants have announced further capacity withdrawal planning. In the following section, we will focus on its capacity exit plan and compare it with the original plan. It can be seen that the pace and magnitude of Samsung’s exit this round is much higher than the market expectation:

(1) LGD: LGD currently has three large LCD production lines of P7, P8, and P9 in China, with a designed capacity of 230K, 240K, and 90K respectively. At the CES exhibition at the beginning of this year, the company announced that IT would shut down all TV panel display production capacity in South Korea in 2020, mainly P7 and P8 lines, while P9 is not included in the exit plan because IT supplies IT panel display for Apple.

(2) Samsung: At present, Samsung has L8-1, L8-2, and L7-2 large-size LCD production lines in South Korea, with designed production capacities of 200K, 150K, and 160K respectively. At the same time in Suzhou has a 70K capacity of 8 generation line.

This round of capacity withdrawal of South Korean plants began in June 2019. Based on the global total production capacity in June 2019, Samsung will withdraw 1,386,900 square meters of production capacity in 2019-2020, equivalent to 9.69% of the global production capacity, according to the previous two-year withdrawal expectation. In 2021, 697,200 square meters of production capacity will be withdrawn, which is equivalent to 4.87% of the global production capacity, and a total of 14.56% will be withdrawn in three years. After the implementation of the new plan, Samsung will eliminate 2.422 million square meters of production capacity by the end of 2020, equivalent to 16.92 percent of the global capacity. This round of production plans from the pace and range are far beyond the market expectations.

Global shipments of TV panel displays totaled 281 million in 2019, down 1.06 percent year on year, according to Insight. In fact, TV panel display shipments have been stable since 2015 at between 250 and 300 million units. At the same time, from the perspective of the structure of sales volume, the period from 2005 to 2010 was the period when the size of China’s TV market grew substantially. Third-world sales also leveled off in 2014. We believe that the sales volume of the TV market has stabilized and there is no big fluctuation. The impact of the epidemic on the overall demand may be more optimistic than the market expectation.

In contrast to the change in volume, we believe that the core driver of the growth in TV panel display demand is actually the increase in TV size. According to the data statistics of Group Intelligence Consulting, the average size of TV panel display in 2014 was 0.47 square meters, equivalent to the size of 41 inches screen. In 2019, the average TV panel size is 0.58 square meters, which is about the size of a 46-inch screen. From 2014 to 2019, the average CAGR of TV panel display size is 4.18%. Meanwhile, the shipment of TV in 2019 also increased compared with that in 2014. Therefore, from 2014 to 2019, the compound growth rate of the total area demand for TV panel displays is 6.37%.

It is assumed that 4K screen and 8K screen will accelerate the penetration and gradually become mainstream products in the next 2-3 years. The pace of screen size increase will accelerate. We have learned through industry chain research that the average size growth rate of TV will increase to 6-8% in 2020. Driven by the growth of the average size, the demand area of global TV panel displays is expected to grow even if TV sales decline, and the upward trend of industry demand remains unchanged.

Meanwhile, the global LCDTV panel display demand will increase significantly in 2021, driven by the recovery of terminal demand and the continued growth of the average TV size. In 2021, the whole year panel display will be in a short supply situation, the mainland panel shows that both males will enjoy the price elasticity.

This paper analyzes the competition pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes. Overall, we believe that the current epidemic has a certain impact on demand, and the panel shows that prices may be under short-term pressure in April or May. But as Samsung’s exit from LCD capacity accelerates, industry inventories remain low. So once the overseas epidemic is contained and domestic demand picks up, the panel suggests prices will surge. We are firmly optimistic about the A-share panel display plate investment value, maintain the industry “optimistic” rating. Suggested attention: BOE A, TCL Technology.

The Liquid Crystal Display (LCD)-enabled electronic devices, such as television, mobile phones and others, is creating potential opportunities for the LCD panel market. In the past couple of years, LCD panels have gained popularity owing to their advanced properties that include less power consumption, compact size and low price.

Moreover, over the past two decades, the LCD technology of has made impressive progress. The electronic displays available at present make use of a wide variety of active LCD panels. The LCD panel market is one of the significantly growing markets due to the increasing demand for LCD displays & low power consumption electronic goods, as well as increase in the demand for touch-enabled displays.

An LCD panel is designed to project on-screen information. At present, LCD panels are suited with high-mobility electronic equipment. LCDs with improved video quality are gaining momentum in all developed and developing economies. These factors are projected to propel the global LCD panel market.

The major growth drivers of the LCD panel market include an increase in the demand for energy-efficient electronic products as well as for larger and 4K televisions. Furthermore, growth in the demand for energy-efficient electronic devices is surging the global LCD panel market.

Demand for high-quality screens, coupled with improving standards of living and inflating disposable income, are among key factors boosting the LCD Panel market. In addition, increase in the adoption of consumer electronic devices is projected to drive the global LCD panel market.

However, one of the major challenges of the LCD panel market are the higher cost and thickness of the display of these devices as compared to other modules. The LCD panel market is expected to witness sluggish and unpredictable growth owing to a quantitative decline in the number of LCD displays.

Moreover, financial uncertainty and macroeconomic situations around the world, such as fluctuating currency exchange rates and economic difficulties, are some of the major factors hindering the growth of the LCD panel market. However, increased competition from alternative technologies and LCD panel complex structure is likely to limit the growth of the LCD panel market.

At present, North America holds the largest market share for the LCD panel market due an increase in the demand for consumer electronic devices. Due to the presence of key LCD panel manufacturers in China and Japan, Asia Pacific is expected to become the prominent region for the LCD panel market.

In addition, the unorganized market of LCD panels in China, Japan and India is creating a competitive environment for global LCD panel manufacturers. Moreover, Europe is the fastest-growing market for LCD panels due to an increase in the adoption of consumer electronics devices. The demand for LCD panels has risen dramatically over the past 12 months globally. The usage of LCD displays in various industries in these regions is boosting the LCD panel market.

The report is a compilation of first-hand information, qualitative and quantitative assessment by industry analysts, inputs from industry experts and industry participants across the value chain. The report provides in-depth analysis of parent market trends, macro-economic indicators and governing factors along with market attractiveness as per segments. The report also maps the qualitative impact of various market factors on market segments and geographies.

Due to an increase in the demand for large LCD displays, the large size LCD panel sub-segment is expected to register double-digit growth rate in the global market. In addition, due to an increase in the demand for portable electronic devices, the small size LCD panel sub-segment is projected to be the most attractive market sub-segment of the global LCD panel market.

The smart phones and tablets sub-segment held the largest market share for the LDC panel market in 2017, and the wearable devices sub-segment is expected to grow with a high CAGR during the forecast period.

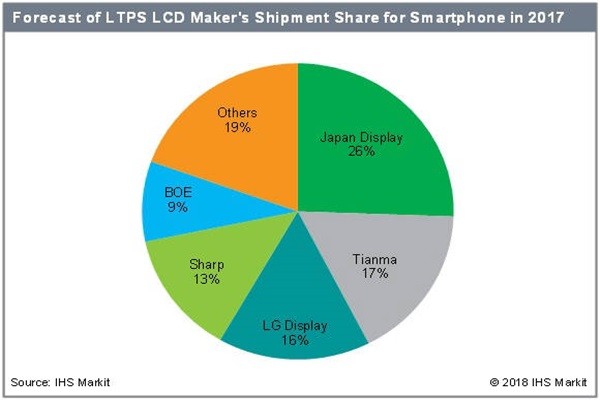

Last year, Chinese display panel maker, Tianma ranked No. 1 in the Low-Temperature Polycrystalline Silicon (LTPS) Liquid Crystal Display (LCD) market share of smart phones. This is the first time that a Chinese display panel maker has taken the lead in the small- and medium- size display market.

According to data provided by IHS Markit, market research company, Tianma recorded a 22% share of the LTPS LCD panel market in 2018. It’s a huge leap of the market share from 16.8% in 2017. The share of Japan-based JDI which ranked No. 1, dropped 25.6% to 18%, and its ranking was pushed back to the second place. Third place was BOE (11%), fourth place was AUO (10%), and fifth place was Sharp (9%).

The reason why Tianma has moved up to the top is because of the Chinese major smartphone makers. Huawei"s Tianma LTPS LCD panel shipments, which stood at 13% in 2015, climbed to 46% in the first half of last year. During the same period, Xiaomi expanded from 30% to 58% and Bibo from 37% to 50%. According to the Counterpoint Research"s data for smartphones sales last year, Huawei shipped 205.3 million units of smartphones increased by 34% YOY, Xiaomi to 121 million units increased by 26% and Bibo to 102.8 million units increased by 3%.

Chinese makers such as Tianma, BOE and AUO have risen to the top of the LTPS LCD panel market, however the Organic Light Emitting Diodes (OLEDs) are more profitable. OLED ($ 6,430.3 million) outperformed LCD ($ 4,195.8 million) in the smartphone display market as of the third quarter of 2018. This is the second time since the fourth quarter of 2017. This result has shown as the smartphone market is stagnant, each company is implementing a premium strategy and the adoption of flexible OLEDs is increasing.

IHS Markit analyzed "the Chinese display industry is investing heavily in OLED" and “Following the increased demand for the premium smartphones, Chinese OLED panel shipment is also increasing.” According to a recent report by Display Supply Chain Consultant (DSCC), the market researcher, BOE"s small- and medium- size OLED panel shipment exceeded 1 million units in every month of the fourth quarter of last year. The yield, which stood at the first digit in the beginning, is expected to exceed 40% in the first quarter of this year.

Meanwhile, the amount of LTPS LCD panel shipment was recorded 689 million units last year. It’s increased by 12% compared to 620 million units last year.

Total shipments of mobile phone displays, including thin-film transistor liquid crystal display (TFT LCD) and active matrix organic light-emitting diode (AMOLED) panels, reached 2.01 billion units in 2017, up 3 percent from 2016, according to preliminary estimate from business information provider IHS Markit (Nasdaq: INFO).

In the growing mobile phone display market, shipments of low-temperature-poly-silicon (LTPS) TFT LCD panels, which realize high-resolution images, increased by 21 percent to 620 million units in 2017 compared to the previous year. Shipments of amorphous silicon (a-Si) TFT LCD mobile phone panels declined 4 percent to 979 million units during the same period. Even though shipments of AMOLED panels jumped in the second half of 2017 thanks to the launch of the iPhone X, combined with the weak demand in the first half, its shipments were up just 3 percent to 402 million units in 2017.

In the smartphone-use LTPS TFT LCD market, Tianma, a leading small and medium panel supplier in China, has shown significant growth, expanding its shipments to Chinese smartphone set brands, such as Huawei and Xiaomi. In 2017, Tianma shipped 105 million LTPS TFT LCD panels for smartphones, almost double its shipments in 2016, with a market share of 17 percent, up 6 percentage points from 2016. It ranked the second largest LTPS TFT LCD supplier for smartphones in 2017, taking over LG Display with 16 percent, down 4 percentage points, and Sharp with 13 percent, down 1 percentage point. In 2017, Japan Display continued its market leader position but shed its share by 10 percentage points to 26 percent in 2017, according to the latest Smartphone Display Intelligent Service report by IHS Markit.

“LTPS TFT is a key technology to produce high-resolution displays for smartphones, and experience is required to optimize highly complex LTPS manufacturing process in each production fab. In terms of experience, Japanese and South Korean panel makers have a competitive advantage compared to Chinese makers,” said Hiroshi Hayase, senior director at IHS Markit. “However, Chinese LCD makers, such as Tianma and BOE, are catching up LTPS technology fast enough to support high demand from Chinese smartphone set makers.”

Due to the COVID-19 pandemic and Russia-Ukraine War Influence, the global market for Product Name estimated at USD million in the year 2022, is projected to reach a revised size of USD million by 2028, growing at a CAGR during the forecast period 2022-2028.

The USA market for LCD Panel is estimated to increase from USD million in 2022 to reach USD million by 2028, at a CAGR during the forecast period of 2023 through 2028.

The China market for LCD Panel is estimated to increase from USD million in 2022 to reach USD million by 2028, at a CAGR during the forecast period of 2023 through 2028.

The Europe market for LCD Panel is estimated to increase from USD million in 2022 to reach USD million by 2028, at a CAGR during the forecast period of 2023 through 2028.

The global key manufacturers of LCD Panel include Samsung, SONY, Sharp, Panasonic, Toshiba, LG, Seiki, Christie and NEC, etc. In 2021, the global top five players had a share approximately in terms of revenue.

This report aims to provide a comprehensive presentation of the global market for LCD Panel, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding LCD Panel.

The LCD Panel market size, estimations, and forecasts are provided in terms of output/shipments (K Tons) and revenue (USD millions), considering 2021 as the base year, with history and forecast data for the period from 2017 to 2028. This report segments the global LCD Panel market comprehensively. Regional market sizes, concerning products by types, by application, and by players, are also provided. The influence of COVID-19 and the Russia-Ukraine War were considered while estimating market sizes.

In this section, the readers will gain an understanding of the key players competing. This report has studied the key growth strategies, such as innovative trends and developments, intensification of product portfolio, mergers and acquisitions, collaborations, new product innovation, and geographical expansion, undertaken by these participants to maintain their presence. Apart from business strategies, the study includes current developments and key financials. The readers will also get access to the data related to global revenue, price, and sales by manufacturers for the period 2017-2022. This all-inclusive report will certainly serve the clients to stay updated and make effective decisions in their businesses.

This section of the report provides key insights regarding various regions and the key players operating in each region. Economic, social, environmental, technological, and political factors have been taken into consideration while assessing the growth of the particular region/country. The readers will also get their hands on the revenue and sales data of each region and country for the period 2017-2028.

The market has been segmented into various major geographies, including North America, Europe, Asia-Pacific, South America. Detailed analysis of major countries such as the USA, Germany, the U.K., Italy, France, China, Japan, South Korea, Southeast Asia, and India will be covered within the regional segment. For market estimates, data are going to be provided for 2021 because of the base year, with estimates for 2022 and forecast value for 2028.

This report will help the readers to understand the competition within the industries and strategies for the competitive environment to enhance the potential profit. The report also focuses on the competitive landscape of the global LCD Panel market, and introduces in detail the market share, industry ranking, competitor ecosystem, market performance, new product development, operation situation, expansion, and acquisition. etc. of the main players, which helps the readers to identify the main competitors and deeply understand the competition pattern of the market.

This report will help stakeholders to understand the global industry status and trends of LCD Panel and provides them with information on key market drivers, restraints, challenges, and opportunities.

Chapter 1: Introduces the report scope of the report, executive summary of different market segments (by region, product type, application, etc), including the market size of each market segment, future development potential, and so on. It offers a high-level view of the current state of the market and its likely evolution in the short to mid-term, and long term.

Chapter 2: Detailed analysis of LCD Panel manufacturers competitive landscape, price, output and revenue market share, latest development plan, merger, and acquisition information, etc.

Chapter 3: Production/output, value of LCD Panel by region/country. It provides a quantitative analysis of the market size and development potential of each region in the next six years.

Chapter 4: Consumption of LCD Panel in regional level and country level. It provides a quantitative analysis of the market size and development potential of each region and its main countries and introduces the market development, future development prospects, market space, and capacity of each country in the world.

Chapter 5: Provides the analysis of various market segments according to product type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments.

Chapter 6: Provides the analysis of various market segments according to application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.

Chapter 7: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product production/output, revenue, , price, gross margin, product introduction, recent development, etc.

Chapter 10: Introduces the market dynamics, latest developments of the market, the driving factors and restrictive factors of the market, the challenges and risks faced by manufacturers in the industry, and the analysis of relevant policies in the industry.

Chapter 13: Forecast by type and by application. It provides a quantitative analysis of the market size and development potential of each market segment in the next six years.

Our Other Reports:Global Cetrimonium Chlorides Market Size 2022 with Company Profile, Sales, Revenue, Average Selling Price, Gross Margin and Forecast to 2025| Research Report by Absolute Reports

Is there a problem with this press release? Contact the source provider Comtex at editorial@comtex.com. You can also contact MarketWatch Customer Service via our Customer Center.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey