lcd panel market share pricelist

Prices for all TV panel sizes fluctuated and are forecast to fluctuate between 2020 and 2022. The period from March 2020 to July 2021 saw the biggest price increases, when a 65" UHD panel cost between 171 and 288 U.S. dollars. In the fourth quarter of 2021, such prices fell and are expected to drop to an even lower amount by March 2022.Read moreLCD TV panel prices worldwide from January 2020 to March 2022, by size(in U.S. dollars)Characteristic32" HD43" FHD49"/50" UHD55" UHD65" UHD------

DSCC. (January 10, 2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) [Graph]. In Statista. Retrieved December 20, 2022, from https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars)." Chart. January 10, 2022. Statista. Accessed December 20, 2022. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. (2022). LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars). Statista. Statista Inc.. Accessed: December 20, 2022. https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC. "Lcd Tv Panel Prices Worldwide from January 2020 to March 2022, by Size (in U.S. Dollars)." Statista, Statista Inc., 10 Jan 2022, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/

DSCC, LCD TV panel prices worldwide from January 2020 to March 2022, by size (in U.S. dollars) Statista, https://www.statista.com/statistics/1288400/lcd-tv-panel-price-by-size/ (last visited December 20, 2022)

The price of LCD display panels for TVs is still falling in November and is on the verge of falling back to the level at which it initially rose two years ago (in June 2020). Liu Yushi, a senior analyst at CINNO Research, told China State Grid reporters that the wave of “falling tide” may last until June this year. For related panel companies, after the performance surge in the past year, they will face pressure in 2022.

LCD display panel prices for TVs will remain at a high level throughout 2021 due to the high base of 13 consecutive months of increase, although the price of LCD display panels peaked in June last year and began to decline rapidly. Thanks to this, under the tight demand related to panel enterprises last year achieved substantial profit growth.

According to China State Grid, the annual revenue growth of major LCD display panel manufacturers in China (Shentianma A, TCL Technology, Peking Oriental A, Caihong Shares, Longteng Optoelectronics, AU, Inolux Optoelectronics, Hanyu Color Crystal) in 2021 is basically above double digits, and the net profit growth is also very obvious. Some small and medium-sized enterprises directly turn losses into profits. Leading enterprises such as BOE and TCL Technology more than doubled their net profit.

Take BOE as an example. According to the 2021 financial report released by BOE A, BOE achieved annual revenue of 219.31 billion yuan, with a year-on-year growth of 61.79%; Net profit attributable to shareholders of listed companies reached 25.831 billion yuan, up 412.96% year on year. “The growth is mainly due to the overall high economic performance of the panel industry throughout the year, and the acquisition of the CLP Panda Nanjing and Chengdu lines,” said Xu Tao, chief electronics analyst at Citic Securities.

In his opinion, as BOE dynamically optimizes its product structure, and its flexible OLED continues to enter the supply chain of major customers, BOE‘s market share as the panel leader is expected to increase further and extend to the Internet of Things, which is optimistic about the company’s development in the medium and long term.

According to the performance report of TCL Technology, the revenue of TCL Technology reached 163.5 billion yuan last year, with a year-on-year growth of 112.8%; Net profit attributable to shareholders of listed companies reached 10.06 billion yuan, up 129.3% year on year.

“There are two main reasons for the ideal performance of domestic display panel enterprises.” A color TV industry analyst believes that, on the one hand, under the effect of the epidemic, the demand for color TV and other electronic products surges, and the upstream raw materials are in shortage, which leads to the short supply of the panel industry, the price rises, and the corporate profits increase accordingly. In addition, as Samsung and LG, the two-panel giants, gradually withdrew from the LCD panel field, they put most of their energy and funds into the OLED(organic light-emitting diode) display panel industry, resulting in a serious shortage of LCD display panels, which objectively benefited China’s local LCD display panel manufacturers such as BOE and TCL China Star Optoelectronics.

Liu Yushi analyzed to reporters that relevant TV panel enterprises made outstanding achievements in 2021, and panel price rise is a very important contributing factor. In addition, three enterprises, such as BOE(BOE), CSOT(TCL China Star Optoelectronics) and HKC(Huike), accounted for 55% of the total shipments of LCD TV panels in 2021. It will be further raised to 60% in the first quarter of 2022. In other words, “simultaneous release of production capacity, expand market share, rising volume and price” is also one of the main reasons for the growth of these enterprises. However, entering the low demand in 2022, LCD TV panel prices continue to fall, and there is some uncertainty about whether the relevant panel companies can continue to grow.

According to Media data, in February this year, the monthly revenue of global large LCD panels has been a double decline of 6.80% month-on-month and 6.18% year-on-year, reaching $6.089 billion. Among them, TCL China Star and AU large-size LCD panel revenue maintained year-on-year growth, while BOE, Innolux, and LG large-size LCD panel monthly revenue decreased by 16.83%, 14.10%, and 5.51% respectively.

Throughout Q1, according to WitsView data, the average LCD TV panel price has been close to or below the average cost, and cash cost level, among which 32-inch LCD TV panel prices are 4.03% and 5.06% below cash cost, respectively; The prices of 43 and 65 inch LCD TV panels are only 0.46% and 3.42% higher than the cash cost, respectively.

The market decline trend is continuing, the reporter queried Omdia, WitsView, Sigmaintel(group intelligence consulting), Oviriwo, CINNO Research, and other institutions regarding the latest forecast data, the analysis results show that the price of the TV LCD panels is expected to continue to decline in April. According to CINNO Research, for example, prices for 32 -, 43 – and 55-inch LCD TV panels in April are expected to fall $1- $3 per screen from March to $37, $65, and $100, respectively. Prices of 65 – and 75-inch LCD TV panels will drop by $8 per screen to $152 and $242, respectively.

“In the face of weak overall demand, major end brands requested panel factories to reduce purchase volumes in March due to high inventory pressure, which led to the continued decline in panel prices in April.” Beijing Di Xian Information Consulting Co., LTD. Vice general manager Yi Xianjing so analysis said.

“Since 2021, international logistics capacity continues to be tight, international customers have a long delivery cycle, some orders in the second half of the year were transferred to the first half of the year, pushing up the panel price in the first half of the year but also overdraft the demand in the second half of the year, resulting in the panel price began to decline from June last year,” Liu Yush told reporters, and the situation between Russia and Ukraine has suddenly escalated this year. It also further affected the recovery of demand in Europe, thus prolonging the downward trend in prices. Based on the current situation, Liu predicted that the bottom of TV panel prices will come in June 2022, but the inflection point will be delayed if further factors affect global demand and lead to additional cuts by brands.

With the price of TV panels falling to the cash cost line, in Liu’s opinion, some overseas production capacity with old equipment and poor profitability will gradually cut production. The corresponding profits of mainland panel manufacturers will inevitably be affected. However, due to the advantages in scale and cost, there is no urgent need for mainland panel manufacturers to reduce the dynamic rate. It is estimated that Q2’s dynamic level is only 3%-4% lower than Q1’s. “We don’t have much room to switch production because the prices of IT panels are dropping rapidly.”

Ovirivo analysts also pointed out that the current TV panel factory shipment pressure and inventory pressure may increase. “In the first quarter, the production line activity rate is at a high level, and the panel factory has entered the stage of loss. If the capacity is not adjusted, the panel factory will face the pressure of further decline in panel prices and increased losses.”

In the first quarter of this year, the retail volume of China’s color TV market was 9.03 million units, down 8.8% year on year. Retail sales totaled 28 billion yuan, down 10.1 percent year on year. Under the situation of volume drop, the industry expects this year color TV manufacturers will also set off a new round of LCD display panel prices war.

According to TrendForce"s latest panel price report, TV panel pricing is expected to arrest its fall in October after five consecutive quarters of decline and the prices of certain panel sizes may even be poised to move up. The price decline of IT panels, whether notebook panels or LCD monitor panels, has also begun showing signs of easing and overall pricing of large-size panels is developing towards bottoming out.

TrendForce indicates, with panel makers actively implementing production reduction plans, TV inventories have also experienced a period of adjustment, with pressure gradually being alleviated. At the same time, the arrival of peak sales season at year’s end has also boosted demand marginally. In particular, Chinese brands are still holding out hope for Double Eleven (Singles’ Day) Shopping Festival promotions and have begun to increase their stocking momentum in turn. Under the influence of strictly controlled utilization rate and marginally stronger demand, TV panel pricing, which are approaching the limit of material costs, is expected to halt its decline in October. Prices of panels below 75 inches (inclusive) are expected to cease their declines. The strength of demand for 32-inch products is the most obvious and prices are expected to increase by US$1. As for other sizes, it is currently understood that PO (Purchase Order) quotations given by panel manufacturers in October have are all increased by US$3~5. Currently China"s Golden Week holiday is ongoing but, after the holiday, panel manufacturers and brands are expected to wrestle with pricing. Based on prices stabilizing, whether pricing can actually be increased still depends on the intensity of demand generated by branded manufacturers for different sized products.

TrendForce observes that current demand for monitor panels is weak, and brands are poorly motivated to stock goods. At the same time, the implementation of production cuts by panel manufacturers has played a role and room for price negotiation has gradually narrowed. At present, the decline in panel pricing has slowed. Prices of small-size TN panels below 21.5 inches (inclusive) are expected to cease declining in October due to reduced supply and flat demand. As for mainstream sizes such as 23.8 and 27-inch, price declines are expected to be within US$1.5. The current demand for notebook panels is also weak and customers must still face high inventory issues and are relatively unwilling to buy panels. Panel makers are also trying to slow the decline in panel prices through their implementation of production reduction plans. Declining panel prices are currently expected to continue abating in October. Pricing for 14-inch and 15.6-inch HD TN panels are expected to drop by US$0.2~0.3, falling from a 1.8% drop in September to 0.7%, while pricing for 14-inch and 15.6-inch FHD IPS panels are expected to fall by US$1~1.2, falling from a 3.4% drop in September to 2.4%.

Compared with past instances when TV panels drove a supply/demand reversal through a sharp increase in demand and spiking prices, this current period of lagging TV panel pricing has been halted and reversed through active control of utilization rates by panel manufacturers and a slight increase in demand momentum. The basis for this break in decline and subsequent price increase is relatively weak. Therefore, in order to maintain the strength of this price backstop and eventual escalation and move towards a healthier supply/demand situation, panel manufacturers must continue to strictly and prudently control the utilization rate of TV production lines, in addition to observing whether sales performance from the forthcoming Chinese festivals beat expectations, allowing stocking momentum to continue, and laying a solid foundation for TV panels to completely escape sluggish market conditions.

The price of IT panels has also adhered to the effect of production reduction and the magnitude of its price drops has gradually eased. TrendForce believes, since the capacity for supplying IT panels is still expanding into the future, it is difficult to see declines in mainstream panel prices halt completely when demand remains weak. Even if new production capacity from Chinese panel factories is gradually completed starting from 2023, price competition in the IT panel market will intensify once products are verified by branded clients, so potential downward pressure in pricing still exists.

For more information on reports and market data from TrendForce’s Department of Display Research, please click here, or email Ms. Vivie Liu from the Sales Department at vivieliu@trendforce.com

Large LCD panels have seen dramatic increase in prices in the first half of 2021 due to unprecedented tight supply that was impacted by component shortages. Panel prices have been increasing for more than a year starting from mid-2020 due to strong demand both in TV and IT market.

Tight supply and extremely high panel prices have resulted in LCD TV set price increases. Softness in demand (due to higher set prices and changes in the COVID 19 situation globally) combined with supply expansion will lead to panel price reductions in 2H 2021.

An increase in demand for larger size TVs in the second half (2H) 2020 combined with component shortage (glass, driver ICs, Polarizers and other components) has pushed the market to unprecedented supply constraint and continuous panel price increase from end of Q2 2020 to 1H 2021 according to DSCC"s blog in August this year,

“Prices increased in Q2 2021 by a double-digit percentage for all sizes of TV panels, with increases ranging from 11% to 22%. Also according to the company, “Comparing our forecast for peak panel prices (in June or July 2021) with the prices in May 2020, we see trough-to-peak increases from 32% for 75” to 175% for 32”, with an average of 106%. In comparison, the average trough-to-peak increase of the 2016 to 2017 cycle was 48%, and prior cycles saw smaller increases.”

Market demand for tablets, notebooks, monitors and TVs increased in 2020 especially in the second half of the year due to the "stay at home" impact, when work from home, education from home and more focus on home entertainment pushed the demand to a higher level. With "stay at home" continuing in the first half of 2021 and UEFA European Championship soccer and Olympics in Japan, TV brands continued to see strong panel demand in that period.

Dramatic panel price increases have resulted in higher costs for TV brands reducing profitability. Brands have increased set prices for their TVs. TV brands have also focused more on larger size higher specs products for better profitability moving away from small and medium sizes, which will impact shipments volume. Lower priced brands (Tier2/3) had a difficult time acquiring enough panels to offer lower priced TVs. Panel suppliers are also giving priority to top brands with larger orders during the supply constraint. In recent quarters, the top five TV brands including Samsung, LG, and TCL, have been gaining higher market share.

While LCD TV faced extreme tight supply and panel price increases, OLED TV has made capacity expansions and cost reductions as LG Display added additional capacity in its 8.5 Gen fab in Guangzhou (increasing to 90K/m up from 60K/m). Also TV brands are more focused on expanding their OLED TV product line as the cost gap between equivalent LCD and OLED panels has reduced significantly. OLED TV is also providing higher profitability for brands. OLED TV has gained higher market share.

“While OLED TV share of all Advanced TV had declined during 2018-2020, the additional capacity from LG Display’s Guangzhou fab combined with rising LCD TV panel prices has helped OLED TV regain share in the premium category. OLED TV shipments increased by 169% Y/Y in Q2 2021, while Advanced LCD TV shipments increased by a more modest 36% Y/Y, and OLED TV share increased from 25% in Q2 2020 to 40% in Q2 2021.”

“OLED panels expected to reach 3% penetration in TV panel market in 2021 owing to persistently narrowing price gap with LCD panels. The company also reported that high-end OLED TV panels and 8K LCD TV panels showed dramatically opposed movements in 1H21, while OLED TV panel increased market shares to 2.6%, 8K LCD shares fell to a mere 0.2%”. This is because as the company reported “panel suppliers’ concerns about profit and yield maximization resulted in their relatively low willingness to manufacture these products. On the demand side, clients were also unwilling to procure these panels due to persistently high quotes from suppliers.”

OLEDs are expected to enjoy continuous growth, as they take higher market share from TVs and smartphones as well as the IT market, benefiting from supply expansion and cost reduction.

“tight supply, high factory utilization rates, and high profitability are encouraging many panel makers to increase their capacities. There were already multiple Gen 8.6 and Gen 10.5 factories in China that were accelerating capacity ramp-ups in 2021 and 2022 after COVID-19 delayed them in 2020”.

Chinese panel makers are incrementally increasing the capacity of their current factories through productivity enhancements and new equipment purchased for de-bottlenecking or creating capacity expansion according to Omdia.

“Chinese panel suppliers were able to achieve a 58.3% share in the TV panel market, which was nearly 5 percentage points higher than their 1H20 market shares, thanks to their growing number of production lines. Conversely, Taiwanese suppliers saw their market share drop by 2.2 percentage points from 1H20 levels to 21.1% in 1H21… Korean suppliers experienced a decline in market shares to 14.3% while Japanese suppliers’ market shares increased to 6.3% as a result of SDP’s Gen 10.5 capacity expansion”.

BOE and CSOT (China Star) have been the top two panel suppliers for LCD TV. They are expanding their production capacity. At the same time HKC is currently increasing its production capacity (4 Gen 8.6 fabs) and is expected to enter the top three rank of TV panel suppliers for the first time with 33.7% YoY increase in TV panel shipments in 2021, according to TrendForce.

The capacity ramp-up by panel suppliers in China and their strong dominance in the TV panel market combined with higher profitability and the need for new suppliers to increase their market share will result in supply expansion in the second half of 2021.

The industry is already reporting some price reduction for TV panels. TrendForce reported in the beginning of August: 7.5% MoM decline for 55’ W UHD open cell TV panels in July. The Display Supply Chain Consultants LCD TV Panel Price Update in August 2021 confirmed LCD panel pricing peaking in June/July and starting to go down. DSCC forecasts price declines for LCD TV throughout the second half of 2021.

It seems that market has reached the end of the “up cycle” of the LCD crystal cycle ending the tight supply situation. The LCD crystal cycle generally creates a multiplier effect with each “up and down” cycle. During the “up cycle” with tight supply and panel price increases, panel buyers buy more, keep higher inventories and sometimes place orders with double bookings to ensure future supply, thereby pushing the market to an even tighter situation. In the “down cycle” when prices decline, panel buyers delay purchases and keep lower inventories to avoid holding higher cost inventory, resulting in a further reduction in demand. With the start of the down cycle, LCD TV panel prices will decline in the second half of 2021. (SD)

Sweta Dash is the founding president of Dash-Insights, a market research and consulting company specializing in the display industry. For more information, contact This email address is being protected from spambots. You need JavaScript enabled to view it. or visitwww.dash-insights.com

Large LCD panel prices have been continuously increasing for last 10 months due to an increase in demand and tight supply. This has helped the LCD industry to recover from drastic panel price reductions, revenue and profit loss in 2019. It has also contributed to the growth of Quantum Dot and MiniLED LCD TV.

Strong LCD TV panel demand is expected to continue in 2021, but component shortages, supply constraints and very high panel price increase can still create uncertainties.

LCD TV panel capacity increased substantially in 2019 due to the expansion in the number of Gen 10.5 fabs. After growth in 2018, LCD TV demand weakened in 2019 caused by slower economic growth, trade war and tariff rate increases. Capacity expansion and higher production combined with weaker demand resulted in considerable oversupply of LCD TV panels in 2019 leading to drastic panel price reductions. Some panel prices went below cash cost, forcing suppliers to cut production and delay expansion plans to reduce losses.

Panel over-supply also brought down panel prices to way lower level than what was possible through cost improvement. Massive 10.5 Gen capacity that can produce 8-up 65" and 6-up 75" panels from a single mother glass substrate helped to reduce larger size LCD TV panel costs. Also extremely low panel price in 2019 helped TV brands to offer larger size LCD TV (>60-inch size) with better specs and technology (Quantum Dot & MiniLED) at more competitive prices, driving higher shipments and adoption rates in 2019 and 2020.

While WOLED TV had higher shipment share in 2018, Quantum Dot and MiniLED based LCD TV gained higher unit shares both in 2019 and 2020 according to Omdia published data. This trend is expected to continue in 2021 and in the next few years with more proliferation of Quantum Dot and MiniLED TVs.

Panel suppliers’ financial results suffered in 2019 as they lost money. Suppliers from China, Korea and Taiwan all lowered their utilization rates in the second half of 2019 to reduce over-supply. Very low prices combined with lower utilization rates made the revenue and profitability situation for panel suppliers difficult in 2019. BOE and China Star cut the utilization rates of their Gen 10.5 fabs. Sharp delayed the start of production at its 10.5 Gen fab in China. LGD and Samsung display decided to shift away from LCD more towards OLED and QDOLED respectively. Both companies cut utilization rates in their 7, 7.5 and 8.5 Gen fabs. Taiwanese suppliers also cut their 8.5 Gen fab utilization rates.

An increase in demand for larger size TVs in the second half of 2020 combined with component shortages has pushed the market to supply constraint and caused continuous panel price increases from June 2020 to March 2021. Market demand for tablets, notebooks, monitors and TVs increased in 2020 especially in the second half of the year due to the impact of "stay at home" regulations, when work from home, education from home and more focus on home entertainment pushed the demand to higher level.

With stay at home continuing in the firts half of 2021 and expected UEFA Europe football tournaments and the Olympic in Japan (July 23), TV brands are expecting stronger demand in 2021. The panel price increase resulting in higher costs for TV brands. It has also made it difficult for lower priced brands (Tier2/3) to acquire enough panels to offer lower priced TVs. Further, panel suppliers are giving priority to top brands with larger orders during supply constraint. In recent quarters, the top five TV brands including Samsung, LG, and TCL have been gaining higher market share.

From June 2020 to January 2021, the 32" TV panel price has increased more than 100%, whereas 55" TV panel prices have increased more than 75% and the 65" TV panel price has increased more than 38% on average according to DSCC data. Panel prices continued to increase through Q1 and the trend is expected to continue in Q2 2021 due to component shortages.

Major increases in panel prices from June 2020, have increased costs and reduced profits for TV brand manufacturers. TV brands are starting to increase TV set prices slowly in certain segments. Notebook brands are also planning to raise prices for new products to reflect increasing costs. Monitor prices are starting to increase in some segments. Despite this, buyers are still unable to fullfill orders due to supply issues.

TV panel prices increased in Q4 2020 and are also expected to increase in the first half of 2021. This can create challenges for brand manufacturers as it reduces their ability to offer more attractive prices in coming months to drive demand. Still, set-price increases up to March have been very mild and only in certain segments. Some brands are still offering price incentives to consumers in spite of the cost increases. For example, in the US market retailers cut prices of big screen LCD and OLED TV to entice basketball fans in March.

Higher LCD price and tight supply helped LCD suppliers to improve their financial performance in the second half of 2020. This caused a number of LCD suppliers especially in China to decide to expand production and increase their investment in 2021.

New opportunities for MiniLED based products that reduce the performance gap with OLED, enabling higher specs and higher prices are also driving higher investment in LCD production. Suppliers from China already have achieved a majority share of TFT-LCD capacity.

BOE has acquired Gen 8.5/8.6 fabs from CEC Panda. ChinaStar has acquired a Gen 8.5 fab in Suzhou from Samsung Display. Recent panel price increases have also resulted in Samsung and LGD delaying their plans to shut down LCD production. These developments can all help to improve supply in the second half of 2021. Fab utilization rates in Taiwan and China stayed high in the second half of 2020 and are expected to stay high in the first half of 2021.

QLED and MiniLED gained share in the premium TV market in 2019, impacting OLED shares and aided by low panel prices. With the LCD panel price increases in 2020 the cost gap between OLED TV and LCD has gone down in recent quarters.

OLED TV also gained higher market share in the premium TV market especially sets from LG and Sony in the last quarter of 2020, according to industry data. LG Display is implimenting major capacity expansion of its OLED TV panels with its Gen 8.5 fab in China.Strong sales in Q4 2020 and new product sizes such as 48-inch and 88-inch have helped LG Display’s OLED TV fabs to have higher utilization rates.

Samsung is also planning to start production of QDOLED in 2021. Higher production and cost reductions for OLED TV may help OLED to gain shares in the premium TV market if the price gap continues to reduce with LCD.

Lower tier brands are not able to offer aggressive prices due to the supply constraint and panel price increases. If these conditions continue for too long, TV demand could be impacted.

Strong LCD TV demand especially for Quantum Dot and MiniLED TV is expected to continue in 2021. The economic recovery and sports events (UEFA Europe footbal and the Olympics in Japan) are expected to drive demand for TV, but component shortages, supply constraints and too big a price increase could create uncertainties. Panel suppliers have to navigate a delicate balance of capacity management and panel prices to capture the opportunity for higher TV demand. (SD)

Sweta Dash, President, Dash-InsightsSweta Dash is the founding president of Dash-Insights, a market research and consulting company specializing in the display industry. For more information, contact This email address is being protected from spambots. You need JavaScript enabled to view it. or visitwww.dash-insights.com

In 2021, LCD panel prices are expected to climb in 1Q, remain flat in 2Q, and decline from 3Q. Backed by ongoing facility expansions, Chinese LCD panel makers should see a continuing rise in M/S. In addition, a recent blackout at the Japanese factory of NEG, a glass substrate maker, should also benefit Chinese firms.

LCD panel prices, which ended high in 2020, are expected to continue rising in 1Q21 on an anticipated decrease in glass substrate supply. On Dec 10, a power outage occurred at NEG’s Takatsuki plant in Japan. With normalization at the Takatsuki plant expected in 1Q21, domestic and Taiwanese panel makers’ sourcing of glass substrate is unlikely to proceed smoothly in the near future. In 2Q21, an acceleration in panel production alongside normalized supply of glass substrate should prevent LCD panel price growth. The rate of glass substrate supply excess is forecast to widen from 0.5% in 1Q21 to 3.6% in 2Q21.

LCD panel prices are forecast to decline from 3Q21, as supply should exceed demand. We expect supply excess for LCD panels to reach 3.2% in 3Q21 and 3.4% in 4Q21 on the back of ongoing production expansion at Chinese manufacturers.

Chinese LCD panel makers are to continue expanding their production capacity, centering on 8G-and-above facilities, in a bid to increase M/S. Given Korea’s withdrawal from the LCD arena, we expect the global number of LCD production facilities (8G or higher) to fall from 32 in 2020 to 31 in 2021 to 30 in 2022. On the other hand, with Chinese panel makers ramping up investment, the portion of Chinese manufacturers is to increase from 63% in 2020 to 68% in 2021 to 78% in 2022, with China coming to claim a market-leading position.

Of note, Chinese panel makers are highly likely to see M/S expansion in 1Q21, as they are insulated from the effects of NEG’s Takatsuki power outage. Chinese companies’ glass substrate supply chain has diversified to encompass Corning, AGC, and NEG (China, Xiamen plant).

We believe that panel prices will close this year on a decline, expecting LCD panel prices to slip from the start of the holiday shopping season in November. China’s LCD industry appears to now be entering its heyday. Going forward, Chinese panel makers are likely to offer low panel prices to set makers as it is essential to establish an entry barrier as they enter the oligopoly stage.

In 3Q20, LCD panel prices rose as set makers increased their panel purchases in preparation for end-year holiday shopping (Black Friday in the US, the Gwanggun Festival in China, etc). We estimate that major TV set makers’ panel purchases climbed 34% q-q during the quarter, exceeding 50mn units. In 3Q20, we believe that on an area basis, LCD demand expanded around 10% q-q, exceeding supply growth of about 8% q-q. However, with low seasonality to be in play on both the supply side and the demand side, the uptrend in LCD panel prices is unlikely to sustain in 4Q20. Although it is difficult to predict the exact timing of the decline in panel prices, they are highly likely to begin falling from the start of the holiday shopping season in November. Expecting the likely 4Q20 drop in LCD demand to surpass the decrease in supply, we estimate that LCD demand will fall around 5% q-q, with supply growth to narrow 2% q-q.

The global LCD industry appears to have entered an oligopolistic phase centered upon China. This oligopoly is being accompanied by a decrease in the number of LCD makers. In fact, China Star acquired Samsung Display’s Suzhou LCD facility in Aug 2020, and BOE acquired CEC Panda in Sep 2020. Moreover, Chinese players are known to be planning to continue expanding capacity and making new investments with the aim of increasing their M/Ss. Of particular note, the combined global market share (by production capacity) of China Star and BOE is projected to climb from 34% this year to 40% in 2021.

In addition, Chinese makers are expected to lower their LCD panel prices, in turn leading to set makers’ appetite for Chinese-made LCDs. We view such price cuts as being essential for Chinese makers if they are to build high entry barriers now that they have reached the oligopoly stage.

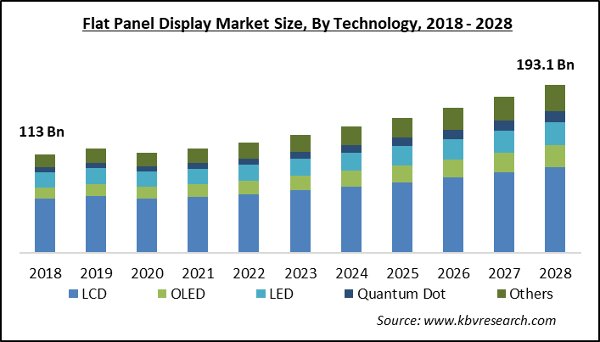

The global display device market reached a value of about USD 131.78 billion in 2021. The industry is further expected to grow at a CAGR of 5.2% in the forecast period of 2023-2028.

The Asia Pacific is expected to emerge as one of the world"s leading markets for display devices. Factors like the growth in the number of tech giants in the region and the availability of manufacturing resources at low cost contribute to the development of the display device industry in the Asia Pacific region.

The residential sector is projected to hold a significant market share in the coming years. The demand for electronic goods, including television, smartphones, laptops, tablets, as well as smart watches, has risen as technological developments continue, which is aiding the growth of the display device industry in the residential sector. Key players are now shifting to implement effective and luminous displays, leading to growth of microdisplay technology, which is expected to aid the global market growth in the coming years.

The remarkable rise in the usage of various consumer electronic products using state-of-the-art technologies is the main driving force behind the industry growth. The rising demand in the gaming and entertainment sector for high-quality displays as well as the increasing popularity of OLED-based technologies are notable factors that are boosting the market growth. The widespread adoption of flexible OLED display technologies is also increasing the demand for display devices. It is also anticipated that the advanced functions of display device will propel the market growth further in the coming years. Other factors boosting the market growth are the rising urbanisation, rising economies, as well as the rising disposable incomes of the consumers.

The report gives a detailed analysis of the following key players in the global display device market, covering their competitive landscape, capacity, and latest developments like mergers, acquisitions, and investments, expansions of capacity, and plant turnarounds:

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Display Type, Technology, Application, End Use, Region

*At Expert Market Research, we strive to always give you current and accurate information. The numbers depicted in the description are indicative and may differ from the actual numbers in the final EMR report.

In the recently released Quarterly OLED Shipment Report , DSCC reveals that 2023 OLED panel revenues are expected to increase 2% Y/Y to $42B after declining 2% Y/Y in 2022. This recovery is the result of expected triple digit growth for monitors, AR/VR and automotive applications and double-digit growth for notebook PCs, TVs and tablets.

As reported by Italian newspaper DDay, the EU Commission has confirmed that its much stricter Energy Efficiency Index (EEI) will be implemented as planned in March 2023 without revision. The new EEI will make it much more challenging to sell 8K TVs in Europe in 2023; all 8K TVs on the market there currently fail to meet the requirements.

After upgrading display capacity for six straight issues on improved market conditions in LCDs, DSCC has now lowered its display capacity forecast for four consecutive quarters on delays and cancellations as conditions worsen and remain weak. Prices were recently at marginal costs for LCD TV panels and it is projected that it will take until 2H’23 for prices to rise above cash costs.

After a weak Q2’22, the combination of macroeconomic and geopolitical events continued to hinder growth for the Advanced TV market, according to the latest update of DSCC’s Quarterly Advanced TV Shipment and Forecast Report, now available to subscribers. Samsung struggled through a difficult quarter, losing both unit and revenue share while its three biggest competitors – LG, Sony and TCL – all gained share.

Panel suppliers are mostly delaying new capacity decisions given the weak market conditions in the display market. The situation is particularly dire in LCDs where LCD TV panel prices approached marginal cost levels and BOE’s Chairman indicated they won’t build any more LCD TV fabs, resulting in the cancellation of B17+ and its removal from our forecast. The weakness in LCDs also spread to OLED spending since there is an oversupply there also and most OLED manufacturers also produce LCDs and are currently losing money. Samsung Display is the exception as it earned record OLED operating profits and operating margins in Q4’22 helped by strong iPhone 14 Pro/Pro Max demand and LG Display’s challenges getting qualified for the 14 Pro Max.

The central promotional event of the holiday season happens this week, and retailers will be offering all-time low prices for TVs during Black Friday. The unprecedented decline in LCD TV panel prices continues to flow through to retail prices in the US, and the competition from LCD is also pulling down OLED TV prices, which are also hitting all-time lows.

Now that all of the industry’s flat panel display makers have reported their Q3’22 financial results, we update our industry profile. The third quarter showed a gaping chasm between OLED-focused display makers, especially Samsung Display, and the companies focused on LCD technology. For LCD makers, it was the worst quarter in years and perhaps the worst ever. Meanwhile, Samsung Display recorded its highest profits ever in the first quarter after it discontinued LCD production.

As revealed in DSCC’s latest release of the OLED Shipment Report – Flash Edition, OLED panel revenues decreased 11% Y/Y on a 17% Y/Y decline in panel shipments. Smartphones, tablets and TVs, which have a combined 70% unit share and 85% panel revenue share, decline while other categories had Y/Y unit growth.

A string of new LCD factories being built, combined with slow demand for notebook and desktop PC screens, caused LCD prices to fall during the first three months of the year, and the downward trend is expected to continue, vendors and analysts said.

Falling prices for LCD (liquid crystal display) screens should help ensure that users find bargains for new monitors, laptops and LCD TVs this year, since the screen is among the most-expensive components in those products. The price declines are also causing vendors to improve picture quality to catch users" eyes and draw them away from competitors.

Makers such as LG.Philips and Samsung Electronics, the world"s two largest LCD producers, are ramping up production at state-of-the-art factories, while rivals continue to add lines at existing plants. Other big players, such as AU Optronics in Taiwan, expect to add plants later this year, which should help keep LCD prices tame.

"The biggest impact from the new plants will be in the first part of this year, but there will be some impact throughout the year," said Frank Lee, an LCD industry analyst for Deutsche Securities Asia in Taipei.

The new LCD plants were built largely to keep pace with demand for LCD TVs, which have been among the hottest-selling items this year. Cutthroat competition among LCD makers also has been a boon to users, ensuring steadily falling prices for the past few years, as screen sizes increase.

For example, prices for 42-inch LCD screens that will be delivered to TV makers in the second half of April fell by $35 each since the end of March, to an average of $890, according to WitsView Technology Co., an industry researcher. Prices for 19-inch panels for PC monitors fell $5 to an average $160.

Average selling prices for LCD panels at AU Optronics fell nearly 12% quarter-on-quarter by the end of March, and the company forecast continued declines into the second quarter, according to executives at its first quarter earnings conference Thursday.

The company expects the price of screens used in desktops and laptops to drop by about 10% quarter-on-quarter during the April to June period, while LCD-TV screen prices will decline by a smaller percentage, in the mid single digits, it said.

LG.Philips said its sales declined in the first quarter compared to the fourth, because of a decline in the average selling prices in LCDs destined for laptops and desktop monitors, with an overall price decline of around 10% for all LCD screen products.

The company is increasing production at a state-of-the-art LCD factory in Korea, as is rival Samsung. AU is building a similar plant in Taiwan that it expects to be in production by the third quarter of this year. LG said it would produce mainly 42-inch and 47-inch screens at the plant, aimed at the LCD-TV market.

Other LCD industry competitors are also increasing production to keep up with demand for LCD-TVS. On Wednesday, S-LCD Corp., the LCD-panel manufacturing joint venture of Sony and Samsung, said it plans to invest $238 million to expand production at its factory in Tangjeong, South Korea.

1.1. THE POLICY COVERS THE HANDLING OF THE PRIVATE INFORMATION EACH USER SHARES WITH TRENDFORCE WHILE VISITING OUR WEBSITES. IF A DIFFERENT PRIVATE POLICY HAS BEEN REFERED TO FOR SPECIFIC TRENDFORCE WEBSITES AND SERVICES, THAT POLICY WILL REPLACE OR SUPPLEMENT THE PRIVACY POLICY MENTIONED IN THIS DOCUMENT. THIS POLICY ALSO COVERS INDIVIDUALS LEGALLY RESIDING IN OR ORGANIZATIONS LEGALLY BASED IN MEMBER COUNTRIES OF THE EUROPEAN UNION (EU) AND ARE SUBJECTED TO EU GENERAL DATA PROTECTION REGULATION (GDPR) WITH REGARD TO PROVISION OF SERVICES AND PERSONAL DATA PROTECTION.

2.1 THE WEBSITE WILL COLLECT AND USE USER INFORMATION FOR PURPOSES SUCH AS MARKETING, CONSUMER PROTECTION, CONSUMER/CLIENT MANAGEMENT, E-COMMERCE SERVICES, FINANCIAL ACCOUNTING, CONTRACTUAL MATTERS, RESEARCH ANALYSIS, AND DATA PROCESSING. WHEN REQUIRED BY LAW, THE WEBSITE MAY ALSO PROVIDE PERSONAL INFORMATION TO NON-GOVERNMENT AGENCIES.

THE WEBSITE WILL NOT DISCLOSE OR SHARE ANY PERSONAL INFORMATION EXCPET PER SPECIAL REQUEST OR WHEN PERMISSION IS RECEIVED FROM THE USER. OTHER EXCEPTIONS INCLUDE:

IN ACCORDANCE WITH ARTICLE 3 OF THE PERSONAL INFORMATION PROTECTION LAW, YOU WILL HAVE THE OPTION TO EXERCISE THE FOLLOWING RIGHTS WITH REGARD TO THE PERSONAL INFORMATION SHARED WITH THE WEBSITE:

a. TO PREVENT UNAUTHORIZED PARTIES FROM ACCESSING, MODIFYING, OR LEAKING PERSONAL USER DATA, THE WEBSITE WILL TAKE STEPS TO IMPLEMENT PROPER SAFETY MEASURES. THE DATA SEARCHED AND RECORDED ON THE WEBSITE AND THE APPROPRIATE SAFETY MEASURES CHOSEN WILL ALL BE REVIEWED CAREFULLY. CONSIDERING HOW THE SAFETY OF TRANSMITTING DATA ON THE INTERNET CAN NEVER BE GUARANTEED COMPLETELY, USERS SHOULD KEEP IN MIND ALL POSSIBLE RISKS ASSOCIATED WITH ONLINE DATA TRANSFERS AND TAKE RESPONSIBILITY FOR ANY INFORMATION SHARED WITH OR OBTAINED FROM THE WEBSITE.

BE SURE TO PROTECT ALL PASSWORDS AND PERSONAL INFORMATION, REFRAIN FROM DISCLOSING PRIVATE USER INFORMATION TO ANY THIRD PARTY, AND REGISTER WITH THE WEBSITE UPON COMPLETING ALL NECESSARY MEMBERSHIP PROCEDURES. WHEN USING A SHARED OR PUBLIC COMPUTER, PLEASE MAKE SURE TO PROPERLY CLOSE ALL RELEVANT BROWSERS TO PREVENT OTHERS FROM READING YOUR PERSONAL E-MAILS OR INFORMATION.

Large-area TFT LCD panel shipments decreased by 10% Month on Month (MoM) and 5% Year on Year (YoY) in April, to 74.1million units, representing historically low shipment performance since May 2020. Omdia defines large-area TFT LCD displays as larger than 9 inches.

"With continued ramifications from the pandemic, demand for IT panels for monitors and notebook PCs remained strong in 4Q21. But as the market became saturated starting in 2022, IT panel shipments started slowing in 1Q22 and early 2Q22," said Robin Wu, Principal Analyst for Large Area Display & Production, Omdia.

Wu said that notebook panel shipments decreased 21% MoM in April, to 18.2 million units, or a 33% decrease from a peak of 27.3 million units in November 2021.

While TV panel prices have decreased noticeably since 3Q21, TV LCD panel shipments increased to a peak of 23.4 million in December 2021, driven by low prices. But rising inflation, the Ukraine crisis and continued lockdowns in China have slowed demand. As a result, TV panel shipments posted a 9% MoM decline in April, to 21.7million units.

Many TV panel prices have fallen below manufacturing cost, and panel makers began to lose money in their TV panel business starting in 4Q21. But Chinese panel makers, the biggest capacity owners, still haven"t reduced their fab utilization. With no sign of demand recovery in 2Q22 or even 3Q22, the supply/demand situation is unlikely to see improvement, Wu said.

"IT LCD panels could still deliver positive cash flow for panel makers. But with prices dropping dramatically, panel makers will soon start to lose money in their IT panel business," Wu said. "Maybe only then will panel makers reduce their glass input and the overall supply/demand situation will return to balance."

About OmdiaOmdia is a leading research and advisory group focused on the technology industry. With clients operating in over 120 countries, Omdia provides market-critical data, analysis, advice, and custom consulting.

As people emerge from their Covid-19 hideouts, demand for screens is likely to drop, and this is happening as Chinese makers dominate the business and threaten to dump screens and wreck the market.

For LCD panels for 65-inch UHD TVs, the average price has increased 4 percent from $274 to $285 month-on-month. When compared to a year ago, that price surged 72 percent from $165.

According to market research company DSCC, the first quarter revenue of 13 LCD companies globally is estimated at $34.8 billion. That’s a 52 percent increase over the same period in 2020.

The possibility of a drop coming with the end of the pandemic brings back memories of the nightmare of two years ago, when the average price of LCD panels dropped from $143 to $100 in nine months as Chinese makers dumped product into the market.

“Because of Covid-19, LCD panels unexpectedly became a hot item,” said an industry official, who requested anonymity. “But as more people are inoculated and spending time outdoors, TV demand is dropping, and this could result in supply exceeding demand.”

Samsung Display CEO Choi Joo-sun said the company is currently reviewing whether to continued LCD production in an e-mail recently sent to employees in the LCD department.

LG Display, which initially planned to fold its LCD TV panel business by end of 2020, is currently running the production plant but without any additional investment or new equipment being installed.

“Already LCD prices when compared to a year ago have more than doubled,” said an industry insider, who wished to remain anonymous. “With China already completely dominating the market, it is unlikely they would repeat low-cost mass production similar to 2019.”

“It is possible that the LCD panel price could fall between the second half of this year and through the first half of next year as demand falls,” said Kim Hyun-soo, Hana Financial Investment analyst. “But as the likelihood of Chinese companies playing a game of chicken is reduced, the prices will likely stabilize in the second half of next year.”

It may seem odd in the face of stalled economies and stalled AV projects, but the costs of LCD display products are on the rise, according to a report from Digital Supply Chain Consulting, or DSCC.

Demand for LCD products remains strong , says DSCC, at the same time as shortages are deepening for glass substrates and driver integrated circuits. Announcements by the Korean panel makers that they will maintain production of LCDs and delay their planned shutdown of LCD lines has not prevented prices from continuing to rise.

I assume, but absolutely don’t know for sure, that panel pricing that affects the much larger consumer market must have a similar impact on commercial displays, or what researchers seem to term public information displays.

Panel prices increased more than 20% for selected TV sizes in Q3 2020 compared to Q2, and by 27% in Q4 2020 compared to Q3, we now expect that average LCD TV panel prices in Q1 2021 will increase by another 12%.

The first chart shows our latest TV panel price update, with prices increasing across the board from a low in May 2020 to an expected peak in May/June of this year. Last month’s update predicted a peak in February/March. However, our forecast for the peak has been increased and pushed out after AGC reported a major accident at a glass plant in Korea and amid continuing problems with driver IC shortages.

Prices increased in Q4 for all sizes of TV panels, with massive percentage increases in sizes from 32” to 55” ranging from 28% to 38%. Prices for 65” and 75” increased at a slower rate, by 19% and 8% respectively, as capacity has continued to increase on those sizes with Gen 10.5 expansions.

Prices for every size of TV panel will increase in Q1 at a slower rate, ranging from 5% for 75” to 16% for 43”, and we now expect that prices will continue to increase in Q2, with the increases ranging from 3% to 6% on a Q/Q basis. We now expect that prices will peak in Q2 and will start to decline in Q3, but the situation remains fluid.

All that said, LCD panels are way less costly, way lighter and slimmer, and generally look way better than the ones being used 10 years ago, so prices is a relative problem.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey