lcd panel production 2018 in stock

BOE Technology Group, the Chinese electronic components producer, is expected to be the leader in producing LCD display panels in the coming years, with a forecast capacity share of 24 percent by 2022. China is the country that has the largest LCD capacity, with a 56 percent share in 2020.Read moreLCD panel production capacity share from 2016 to 2022, by manufacturerCharacteristicBOEChina StarInnoluxAUOLGDHKCCEC PandaSharpSDCOther-----------

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2022, by manufacturer [Graph]. In Statista. Retrieved December 16, 2022, from https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "LCD panel production capacity share from 2016 to 2022, by manufacturer." Chart. June 8, 2020. Statista. Accessed December 16, 2022. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. (2020). LCD panel production capacity share from 2016 to 2022, by manufacturer. Statista. Statista Inc.. Accessed: December 16, 2022. https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2022, by Manufacturer." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/

DSCC, LCD panel production capacity share from 2016 to 2022, by manufacturer Statista, https://www.statista.com/statistics/1057455/lcd-panel-production-capacity-manufacturer/ (last visited December 16, 2022)

China is the leader in producing LCD display panels, with a forecast capacity share of 56 percent in 2020. China"s share is expected to increase in the coming years, stabilizing at 69 percent from 2023 onwards.Read moreLCD panel production capacity share from 2016 to 2025, by countryCharacteristicChinaJapanSouth KoreaTaiwan-----

DSCC. (June 8, 2020). LCD panel production capacity share from 2016 to 2025, by country [Graph]. In Statista. Retrieved December 16, 2022, from https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "LCD panel production capacity share from 2016 to 2025, by country." Chart. June 8, 2020. Statista. Accessed December 16, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. (2020). LCD panel production capacity share from 2016 to 2025, by country. Statista. Statista Inc.. Accessed: December 16, 2022. https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC. "Lcd Panel Production Capacity Share from 2016 to 2025, by Country." Statista, Statista Inc., 8 Jun 2020, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/

DSCC, LCD panel production capacity share from 2016 to 2025, by country Statista, https://www.statista.com/statistics/1056470/lcd-panel-production-capacity-country/ (last visited December 16, 2022)

(January 23, 2019) – Global shipments of large thin-film transistor (TFT) liquid crystal display (LCD) panels rose again in 2018 despite concerns of over-supply in the market. In particular, area shipments increased by 10.6 percent to 197.9 million square meters compared to the previous year, driven by TV and monitor panels, according to

Fierce price competition in large 65- and 75-inch display panels was ignited as Chinese panel maker BOE started the mass production of the panels in 2018 at its B9 10.5-generation facility. “With BOE operating the 10.5-generation line, panel makers have become more aggressive on pricing since early 2018 to digest their capacity,” said

Rising demand for gaming-PC and professional-purpose monitors boosted shipments of high-end, large panels. “Some panel makers have allocated more monitor panels to the fab, replacing existing TV panels, to make up for poor performance of that business,” Wu said.

Demand for other applications, which include public, automotive and industrial displays, recorded the highest growth rates of 17.5 percent by area and 28.6 percent by unit. “Panel makers view these applications as a new cash cow that can compensate for the sharp price erosion in main panels for TVs, monitors and notebook PCs,” Wu said.

LG Display led the area shipments of large display panels, with a 21 percent share in 2018, followed by BOE (17 percent) and Samsung Display (16 percent). BOE boasted the largest unit-shipment share of 23 percent, followed by LG Display (20 percent) and Innolux (17 percent), according to the

Large TFT LCD panel shipment growth is expected to continue in 2019. The preliminary forecast for unit shipments of three major products indicates that panel makers will continue to focus on the monitor and notebook PC panel businesses, increasing shipments by 5.3 percent and 6.6 percent, respectively, over the year, while shipments of TV panels are forecast to grow just 2.6 percent.

In 2019, three new 10.5-generation fabs – ChinaStar’s T6, BOE’s second fab and Foxconn/Sharp’s Guangzhou line – are expected to start mass production. All of them are assigned to manufacture TV panels, further boosting TV panel supply. “As the TV panel business is predicted to remain tough, panel makers, who enjoyed relatively better outcomes with monitor and notebook PC panels in 2018, will likely focus on the IT panel businesses,” Wu said.

IHS Markit provides information about the entire range of large display panels shipped worldwide and regionally, including monthly and quarterly revenues and shipments by display area, application, size and aspect ratio for each supplier.

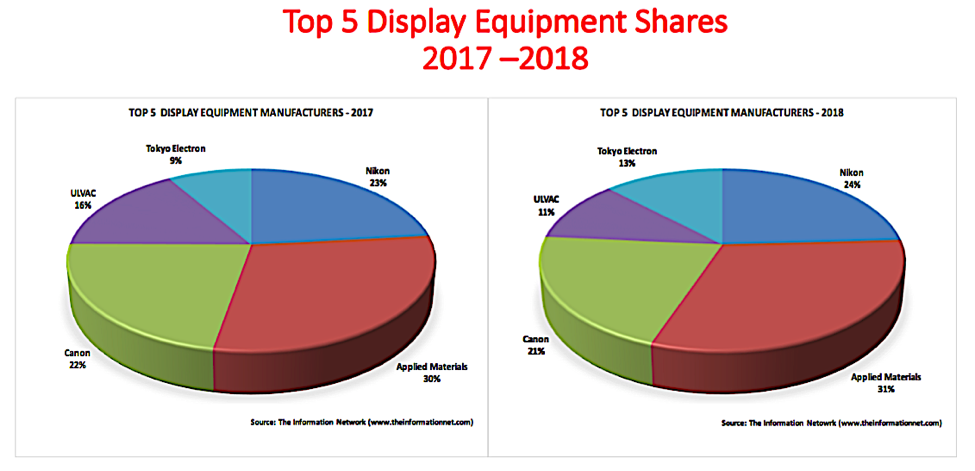

The market for equipment to manufacture LCD and OLED displays for smartphones and TVs grew 28% in 2018 following a growth of 33% in 2017. Applied Materials" (NASDAQ:AMAT) revenues grew 36%. A key driver for AMAT"s strong performance was the sale of equipment to Chinese LCD manufacturers BOE Technology and China Star Optoelectronics Technology to manufacture 10.5G panels for the production of 75-inch LCD TVs.

While the 10.5G market will be strong again in 2019, AMAT will face headwinds in sectors that utilize equipment for the production of smaller displays, primarily smartphones.

During Applied Materials’ recent Q1 earnings call, CEO Gary Dickerson noted: "In display, weakness in emerging markets is also impacting the timing of customers’ investment plans. We see some TV factory projects pushing out of year and into 2020. As a result, we now believe our display equipment revenue in 2019 will decline by about a third from 2018"s record levels. We also expect revenue in the second fiscal quarter to be significantly lower than our average run rate for the year."

Providing more granularity, market share growth ofAMAT and Nikon is primarily attributed to the investments by BOE in its 10.5G LCD. Both equipment companies are the only suppliers of equipment (AMAT for deposition and Nikon for lithography) that can fabricate the large 10.5G panels. So even though AMAT is a deposition company, its tool, acquired about 20 years ago from the acquisition of AKT, is the only one on the market big enough to accommodate 10.5G panels.

The display market can be segmented into three general segments – (1) LCD panels for TVs, (2) OLED panels for smartphones, and (3) LCD panels for Smartphones. Each of these has its own headwinds and tailwinds, which are impacting capital equipment expenditures. These issues I detail below. There are numerous ways to segment this industry, but I am detailing this segmentation for this article.

A driving force for 10.5G plant construction is that a 10.5G mother glass is 1.8 times larger than an 8.5G one in area and can be cut into six 75-inch panels. In comparison, a 7.5G glass substrate can be cut into only two 75-inch TV panels. Thus, there is a significant cost benefit of moving to the larger substrates.

AMAT’s deposition tools are used to form the backplane for LCD displays. The company’s deposition tools are the only ones capable of uniform coating of panels this size, which measure 3370mm x 2940mm. AMAT’s equipment can deposit various materials for the backplane.

Shown in Table 1 are the number of 10.5G panels being manufactured through 2018, with forecasts for panel production in 2019 and 2020, according to The Information Network’s report “OLED and LCD Markets: Technology, Directions and Market Analysis.”

10.5G represented a strong tailwind for AMAT and Nikon in 2018. For example, Nikon sold 13, 10.5G lithography systems in CY2018 representing 18% of systems sold. This compares to only one 10.5G system sold in CY2017.

BOE Technology’s first 10.5G fab, located in Hefei, entered volume production in the first half of 2018. China Star Optoelectronics Technology (CSOT) plans to build to kick off commercial operations of its 10.5G plant in March 2019, having installed equipment in 2018. Capex spends by these companies for these plants provided a significant portion of AMAT"s revenues for 2018.

For 2019, BOE’s second 10.5G line, to be located in Wuhan, is slated for volume production in 2020, with equipment installation in mid-2019. Sharp (OTCPK:SHCAY) will start equipment install at its new 10.5G LCD plant in Guangzhou in early 2019, with plans to kick off the first phase of the facility in Aug 2019 and to begin volume production in October 2019. LG Display (LPL) is building its 10.5G OLED P10 fab in Paju, Korea, but volume production is now scheduled at the beginning of 2021. Originally, the company planned to install equipment in 3Q 2018, but it may be pushed back to the beginning of 2020. With an oversupply of 10.5G panels as a result of BOE and CSOT production, display manufacturers are closely monitoring the market.

In addition to 10.5G mother glass for TVs, most LCD TVs are made using 8G glass. In 2018, LCD panel shipments increased 9% while TV area increased 11%, meaning that the average size of a TV is increasing. While some of the increase was due to shipments from BOE’s 10.5G plant, 8G plants were responsible for most of the growth. LG Display, for example, which makes LCD TVs from 8G mother glass, witnessed a 21% increase in area shipments, whereas Innolux, also without a 10.5G plant, reported an increase of 17% in area shipments. BOE, with both 8G and 10.5G plants, reported an area shipment increase of 17%.

I am neutral on AMAT in the OLED panel for smartphones. There are two issues. One is that AMAT’s equipment used in the production of OLEDs is being supplanted by competitor’s differentiating technology.

A second factor contributing to my neutral stance for AMAT in this OLED market is a sluggish smartphone market – the largest application for 6G OLED panels. Investment was minimal in 2018 as shown in Table 3. Also tied to sluggish smartphone sales is product distinction. Rigid OLED panels are not significantly better than lower-cost LTPS-LCD panels. With the capacity built up through 2018, utilization rates averaged 60%.

Table 4 presents The Information Network’s forecast of 6G OLED panel output to 2020. Again, panel output only increased 32,000 panels per month in 2018, but is expected to increase 138,000 panels per month in 2019, followed by a more moderate growth of 121,000 panels per month in 2020.

Flexible smartphones will drive the 6G market in 2019 and 2020. Samsung Electronics (OTCPK:SSNLF) introduced its Galaxy Fold and Huawei its Mate X in February 2018. Details of the two smartphones are described here. A significant difference between the two is the display.

I am bearish for AMAT on LCD panels for smartphones. Table 2 illustrates the drop in 6G plant expansion in 2018 showing Nikon’s lithography system sales by panel generation in 2017 and 2018. 6G systems dropped from 42 units in 2017 to 18 in 2018

Although flexible OLED has been gaining market share in the smartphone market in the last few years for its thinner form factor, higher performance, and differentiating design, the high utilization rates of 90% is minimizing the need for plant expansion and resulting in an oversupply of 20% for LCDs. Combined, these contribute to a 20% discount in LCD cost per smartphone compared to a rigid OLED display. Tianma is the top supplier of LTPS TFT-LCDs for smartphones with shipments of 149 million units in 2018, an increase of 49% YoY.

High-end smartphones like Apple"s current iPhone XS and iPhone XS Max use OLED screens to deliver better image quality, faster pixel response times. The XR uses an LCD display. It is likely we will see a similar lineup in 2019 - a continuation of both the iPhone XS and XR devices, with rumors suggesting 5.8 and 6.5-inch OLED iPhones along with a 6.1-inch LCD iPhone.

AMAT capitalized on the size of its deposition tools to generate strong revenue growth in the 10.5G market. In the other segments of the display production market (6G and 8G), its deposition tools for backplane and OLED encapsulation do not offer any advantages over competitors. In fact, the company is losing share to better technology.

The primary claim for AMAT"s display tools is its size. If 6G LCD factory expansion is dropping and 10.5G factories make panels with better economies of scale than 8G factories to make TVs, then it is only a matter of time before a competitor makes equipment that can deposit the backplanes on 10.5G panels.

LCD panel prices have risen for 4 months in a row because of your home gaming? Since this year, the whole LCD panel market has smoked. Whether after the outbreak of the epidemic, LCD panel market prices rose for four months, or the panel giants in Japan and South Korea successively sold production lines, or the Chinese mainland listed companies frequently integrated acquisition, investment, and plant construction, all make the industry full of interesting.

LCD panel prices are already a fact. Since May this year, LCD panel prices have risen for four months in a row, making the whole industry chain dynamic. Why are LCD panels going up in price in a volatile 2020? The key factor lies in the imbalance between supply and demand.

The price of LCDS for large-size TVs of 70 inches or more hasn’t budged much. In addition, LTPS screens and AMOLED screens used in high-end phones have seen little or no increase in price.

As for October, LCD panel price increases are expected to moderate. The data shows that in October 32 inches or 2 dollars; Gains of 39.5 to 43 inches will shrink to $3;55 inches will fall back below $10; The 65-inch gain will narrow to $5.

During the epidemic, people stayed at home and had no way to go out for entertainment. They relied on TV sets, PCS, and game consoles for entertainment. After the resumption of economic work and production, the market of traditional home appliances picked up rapidly, and LCD production capacity was quickly digested.

However, due to the shutdown of most factories lasting 1-2 months during the epidemic period, LCD panel production capacity was limited, leading to insufficient production capacity in the face of the market outbreak, which eventually led to the market shortage and price increase for 4 consecutive months.

In fact, the last round of price rise of LCD panels was from 2016 to 2017, and its overall market price has continued to fall since 2018. Even in 2019, individual types have fallen below the material cost, and the whole industry has experienced a general operating loss. As a result, LCD makers have been looking for ways to improve margins since last year.

A return to a reasonable price range is the most talked about topic among panel makers in 2019, according to one practitioner. Some manufacturers for the serious loss of the product made the decision to reduce production or even stop production; Some manufacturers planned to raise the price, but due to the epidemic in 2020, the downstream demand was temporarily suppressed and the price increase was postponed. After the outbreak was contained in April, LCD prices began to rise in mid-to-late May.

In fact, the market price of LCD panels continued to decline in 2018-2019 because of the accelerated rise of China’s LCD industry and the influx of a large number of local manufacturers, which doubled the global LCD panel production capacity within a few years, but there was no suitable application market to absorb it. The result of excess capacity is oversupply, ultimately making LCD panel prices remain depressed.

Against this background, combined with the impact of the epidemic in 2020, the operating burden of LCD companies in Japan and South Korea has been further aggravated, and it is difficult to make profits in the production of LCD panels, so they have to announce the withdrawal of LCD business.

business in June 2022. In August, Sharp bought JDI Baishan, a plant in Ishikawa prefecture that makes liquid crystal display panels for smartphones. In early September, Samsung Display sold a majority stake in its SUZHOU LCD production plant to Starlight Electronics Technology, a unit of TCL Technology Group. LGD has not only pulled out of some of its production capacity but has announced that it will close its local production line in 2020. According to DSCC, a consultancy, the share of LCD production capacity in South Korea alone will fall from 19% to 7% between 2020 and 2021.

It is worth mentioning that in industry analysis, in view of the fact that Korean companies are good at using “dig through old bonus – selling high price – the development of new technology” the cycle of development mode, another 2020 out of the LCD production capacity, the main reason may be: taking the advantage of China’s expanding aggressively LCD manufacturers, Korean companies will own LCD panel production line hot sell, eliminating capacity liquid to extract its final value, and turning to the more profitable advantage of a new generation of display technologies, such as thinner, color display better OLED, etc. Samsung, for example, has captured more than 80% of the OLED market with its first-mover advantage.

From the perspective of production capacity, the launch of LCD tracks by major manufacturers in Japan and South Korea must reduce some production capacity in the short term, which to some extent induces market price fluctuations. In the long run, some of the Japanese and Korean LCD production capacity has been bought by Chinese manufacturers, coupled with frequent investment in recent years, the overall capacity is sure to recover as before, or even more than before. But now it will take time to expand the production layout, which more or less will cause supply imbalance, the industry needs to be cautious.

The LCD panel industry started in the United States and then gradually moved to Japan, South Korea, China, and Taiwan. At present, the proportion of production capacity in The Chinese mainland has reached 52% in 2020, and there are leading LCD panel products in China represented by BOE, Huxing Optoelectronics. Meanwhile, the production capacity layout of BOE, Huike, Huxing Optoelectronics, and other manufacturers has been basically completed, making industrial integration a necessity.

On the one hand, South Korean enterprises out of the LCD track, the domestic factory horse enclosure, plant expansion action. While LCDs may not sell as well as “upstart” flexible screens, respondents believe they are still strong enough in the traditional home appliance market to warrant continued investment. Zhao Bin, general manager of TCL Huaxing Development Center, has said publicly that the next-generation display technology will be mature in four to five years, but the commercialization of products may not take place until a decade later. “LCD will still be the mainstream in this decade,” he said.

On the other hand, there is no risk of neck jam in China’s LCD panel industry, which is generally controllable. In mainland China, there will be 21 production lines capable of producing 32-inch or larger LCD panels by 2021, accounting for about two-thirds of the global total. In terms of the proportion of production capacity, the Chinese mainland accounted for 42% of the global LCD panel in 2019, 51% this year, and will continue to climb to 63% next year.

Of course, building factories and expanding production cannot be accomplished overnight. In the process of production capacity recovery, it is predicted that there will be several price fluctuations, and the cost may be passed on to the downstream LCD panel manufacturers or consumers when the price rises greatly, which requires continuous attention.

[Introduction]: This paper analyzes the competitive pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes.

Since April 2020, the display device sector rose 4.81%, ranking 11th in the electronic subsectors, 3.39 percentage points behind the SW electronic sector, 0.65 percentage points ahead of the Shanghai and Shenzhen 300 Index. Of the top two domestic panel display companies, TCL Technology is up 11.35 percent in April and BOE is up 4.85 percent.

Specific to the panel display plate, we still do the analysis from both ends of supply and demand: supply-side: February operating rate is insufficient, especially panel display module segment grain rate is not good, limited capacity to boost the panel display price. Since March, effective progress has been made in the prevention and control of the epidemic in China. Except for some production lines in Wuhan that have been delayed, other domestic panels show that the production lines have returned to normal. In South Korea, Samsung announced recently that it would accelerate its withdrawal from all LCD production lines. This round of output withdrawal exceeded market expectations both in terms of pace and amplitude. We will make a detailed analysis of it in Chapter 2.

Demand-side: We believe that people spend more time at home under the epidemic situation, and TV, as an important facility for family entertainment, has strong demand resilience. In our preliminary report, we have interpreted the pick-up trend of domestic TV market demand in February, which also showed a good performance in March. At present, the online market in China maintains a year-on-year growth of about 30% every week, while the offline market is still weak, but its proportion has been greatly reduced. At present, people are more concerned about the impact of the epidemic overseas. According to the research of Cinda Electronics Industry Chain, in the first week, after Italy was closed down, local TV sales dropped by about 45% from the previous week. In addition, Media Markt, Europe’s largest offline consumer electronics chain, also closed in mid-March, which will affect terminal sales to some extent, and panel display prices will continue to be under pressure in April and May. However, we believe that as the epidemic is brought under control, overseas market demand is expected to return to the pace of China’s recovery.

From a price perspective, the panel shows that prices have risen every month through March since the bottom of December 19 reversed. However, according to AVC’s price bulletin of TV panel display in early April, the price of TV panel display in April will decrease slightly, and the price of 32 “, 39.5 “, 43 “, 50 “and 55” panels will all decrease by 1 USD.65 “panel shows price down $2; The 75 “panel shows the price down by $3.The specific reasons have been described above, along with the domestic panel display production line stalling rate recovery, supply-side capacity release; The epidemic spread rapidly in Europe and the United States, sports events were postponed, local blockades were gradually rolled out, and the demand side declined to a certain extent.

Looking ahead to Q2, we think prices will remain under pressure in May, but prices are expected to pick up in June as Samsung’s capacity is being taken out and the outbreak is under control overseas. At the same time, from the perspective of channel inventory, the current all-channel inventory, including the inventory of all panel display factories, has fallen to a historical low. The industry as a whole has more flexibility to cope with market uncertainties. At the same time, low inventory is also the next epidemic warming panel show price foreshadowing.

In terms of valuation level, due to the low concentration and fierce competition in the panel display industry in the past ten years, the performance of sector companies is cyclical to a certain extent. Therefore, PE, PB, and other methods should be comprehensively adopted for valuation. On the other hand, the domestic panel shows that the leading companies in the past years have sustained large-scale capital investment, high depreciation, and a long period of poor profitability, leading to the inflated TTM PE in the first half of 2014 to 2017. Therefore, we will display the valuation level of the sector mainly through the PB-band analysis panel in this paper.

In 2017, due to the combined impact of panel display price rise and OLED production, the valuation of the plate continued to expand, with the highest PB reaching 2.8 times. Then, with the price falling, the panel shows that PB bottomed out at the end of January 2019 at only 1.11 times. From the end of 2019 to February, the panel shows that rising prices have driven PB all the way up, the peak PB reached 2.23 times. Since entering March, affected by the epidemic, in the short term panel prices under pressure, the valuation of the plate once again fell back to 1.62 times. In April, the epidemic situation in the epidemic country was gradually under control, and the valuation of the sector rebounded to 1.68 times.

We believe the sector is still at the bottom of the stage as Samsung accelerates its exit from LCD capacity and industry inventories remain low. Therefore, once the overseas epidemic is under control and the domestic demand picks up, the panel shows that prices will rise sharply. In addition, the plate will also benefit from Ultra HD drive in the long term. Panel display plate medium – and long-term growth logic is still clear. Coupled with the optimization of the competitive pattern, industry volatility will be greatly weakened. The current plate PB compared to the historical high has sufficient space, optimistic about the plate leading company’s investment value.

Revenue at Innolux and AU Optronics has been sluggish for several months and improved in March. Since the third quarter of 2017, Innolux’s monthly revenue growth has been negative, while AU Optronics has only experienced revenue growth in a very few months.AU Optronics recorded a record low revenue in January and increased in February and March. Innolux’s revenue returned to growth in March after falling to its lowest in recent years in February. However, because the panel display manufacturers in Taiwan have not put in new production capacity for many years, the production process of the existing production line is relatively backward, and the competitiveness is not strong.

On March 31, Samsung Display China officially sent a notice to customers, deciding to terminate the supply of all LCD products by the end of 2020.LGD had earlier announced that it would close its local LCDTV panel display production by the end of this year. In the following, we will analyze the impact of the accelerated introduction of the Korean factory on the supply pattern of the panel display industry from the perspective of the supply side.

The early market on the panel display plate is controversial, mainly worried about the exit of Korean manufacturers, such as LCD display panel price rise, or will slow down the pace of capacity exit as in 17 years. And we believe that this round of LCD panel prices and 2017 prices are essentially different, the LCD production capacity of South Korean manufacturers exit is an established strategy, will not be transferred because of price warming. Investigating the reasons, we believe that there are mainly the following three factors driving:

(1) Under the localization, scale effect, and aggregation effect, the Chinese panel leader has lower cost and stronger profitability than the Japanese and Korean manufacturers. In terms of cost structure, according to IHS data, material cost accounts for 70% of the cost displayed by the LCD panel, while depreciation accounts for 17%, so the material cost has a significant impact on it. At present, the upstream LCD, polarizer, PCB, mold, and key target material line of the mainland panel display manufacturers are fully imported into the domestic, effectively reducing the material cost. In addition, at the beginning of the factory, manufacturers not only consider the upstream glass and polarizer factory but also consider the synergy between the downstream complete machine factory, so as to reduce the labor cost, transportation cost, etc., forming a certain industrial clustering effect. The growing volume of shipments also makes the economies of scale increasingly obvious. In the long run, the profit gap between the South Korean plant and the mainland plant will become even wider.

(2) The 7 and 8 generation production lines of the Korean plant cannot adapt to the increasing demand for TV in average size. Traditionally, the 8 generation line can only cut the 32 “, 46 “, and 60” panel displays. In order to cut the other size panel displays economically and effectively, the panel display factory has made small adjustments to the 8 generation line size, so there are the 8.5, 8.6, 8.6+, and 8.7 generation lines. But from the cutting scheme, 55 inches and above the size of the panel display only part of the generation can support, and the production efficiency is low, hindering the development of large size TV. Driven by the strong demand for large-size TV, the panel display generation line is also constantly breaking through. In 2018, BOE put into operation the world’s first 10.5 generation line, the Hefei B9 plant, with a designed capacity of 120K/ month. The birth of the 10.5 generation line is epoch-making. It solves the cutting problem of large-size panel displays and lays the foundation for the outbreak of large-size TV. From the cutting method, one 10.5 generation line panel display can effectively cut 18 43 inches, 8 65 inches, 6 75 inches panel display, and can be more efficient in hybrid mode cutting, with half of the panel display 65 inches, the other half of the panel display 75 inches, the yield is also guaranteed. Currently, there are a total of five 10.5 generation lines in the world, including two for domestic panel display companies BOE and Huaxing Optoelectronics. Sharp has a 10.5 generation line in Guangzhou, which is mainly used to produce its own TV. Korean manufacturers do not have the 10.5 generation line. In the context of the increasing size of the TV, Korean manufacturers are obviously at a disadvantage in competitiveness.

(3) As the large-size OLED panel display technology has become increasingly mature, Samsung and LGD hope to transfer production to large-size OLED with better profit prospects as soon as possible. Apart from the price factor, the reason why South Korean manufacturers are exiting LCD production is more because the large-size OLED panel display technology is becoming mature, and Samsung and LGD hope to switch to large-size OLED production as soon as possible, which has better profit prospects. At present, there are three major large-scale OLED solutions including WOLED, QD OLED, and printed OLED, while there is only WOLED with a mass production line at present.

According to statistics, shipments of OLED TVs totaled 2.8 million in 2018 and increased to 3.5 million in 2019, up 25 percent year on year. But it accounted for only 1.58% of global shipments. The capacity gap has greatly limited the volume of OLED TV.LG alone consumes about 47% of the world’s OLED TV panel display capacity, thanks to its own capacity. Other manufacturers can only purchase at a high price. According to the industry chain survey, the current price of a 65-inch OLED panel is around $800-900, while the price of the same size LCD panel is currently only $171.There is a significant price difference between the two.

Samsung and LGD began to shut down LCD production lines in Q3 last year, leading to the recovery of the panel display sector. Entering 2020, the two major South Korean plants have announced further capacity withdrawal planning. In the following section, we will focus on its capacity exit plan and compare it with the original plan. It can be seen that the pace and magnitude of Samsung’s exit this round is much higher than the market expectation:

(1) LGD: LGD currently has three large LCD production lines of P7, P8, and P9 in China, with a designed capacity of 230K, 240K, and 90K respectively. At the CES exhibition at the beginning of this year, the company announced that IT would shut down all TV panel display production capacity in South Korea in 2020, mainly P7 and P8 lines, while P9 is not included in the exit plan because IT supplies IT panel display for Apple.

According to our latest industry chain survey, by the end of Q1 in 2020, P7 production capacity remains 140K; P8 has 100K of capacity left.P7 is expected to shut down by the end of the year, and P8 will shut down all TV production capacity at the end of the year, but there is still 40KIT production capacity to continue.

(2) Samsung: At present, Samsung has L8-1, L8-2, and L7-2 large-size LCD production lines in South Korea, with designed production capacities of 200K, 150K, and 160K respectively. At the same time in Suzhou has a 70K capacity of 8 generation line.

Samsung had planned to retire all L8-1 and L8-2 capacity by the end of 2021, while L7-2 would retain 50K of IT capacity. This time, it is planned to withdraw all production capacity by the end of 2020, among which the production line in South Korea will be converted to Qdoled, and the production line in Suzhou will be sold.

This round of capacity withdrawal of South Korean plants began in June 2019. Based on the global total production capacity in June 2019, Samsung will withdraw 1,386,900 square meters of production capacity in 2019-2020, equivalent to 9.69% of the global production capacity, according to the previous two-year withdrawal expectation. In 2021, 697,200 square meters of production capacity will be withdrawn, which is equivalent to 4.87% of the global production capacity, and a total of 14.56% will be withdrawn in three years. After the implementation of the new plan, Samsung will eliminate 2.422 million square meters of production capacity by the end of 2020, equivalent to 16.92 percent of the global capacity. This round of production plans from the pace and range are far beyond the market expectations.

Global shipments of TV panel displays totaled 281 million in 2019, down 1.06 percent year on year, according to Insight. In fact, TV panel display shipments have been stable since 2015 at between 250 and 300 million units. At the same time, from the perspective of the structure of sales volume, the period from 2005 to 2010 was the period when the size of China’s TV market grew substantially. Third-world sales also leveled off in 2014. We believe that the sales volume of the TV market has stabilized and there is no big fluctuation. The impact of the epidemic on the overall demand may be more optimistic than the market expectation.

In contrast to the change in volume, we believe that the core driver of the growth in TV panel display demand is actually the increase in TV size. According to the data statistics of Group Intelligence Consulting, the average size of TV panel display in 2014 was 0.47 square meters, equivalent to the size of 41 inches screen. In 2019, the average TV panel size is 0.58 square meters, which is about the size of a 46-inch screen. From 2014 to 2019, the average CAGR of TV panel display size is 4.18%. Meanwhile, the shipment of TV in 2019 also increased compared with that in 2014. Therefore, from 2014 to 2019, the compound growth rate of the total area demand for TV panel displays is 6.37%.

It is assumed that 4K screen and 8K screen will accelerate the penetration and gradually become mainstream products in the next 2-3 years. The pace of screen size increase will accelerate. We have learned through industry chain research that the average size growth rate of TV will increase to 6-8% in 2020. Driven by the growth of the average size, the demand area of global TV panel displays is expected to grow even if TV sales decline, and the upward trend of industry demand remains unchanged.

Meanwhile, the global LCDTV panel display demand will increase significantly in 2021, driven by the recovery of terminal demand and the continued growth of the average TV size. In 2021, the whole year panel display will be in a short supply situation, the mainland panel shows that both males will enjoy the price elasticity.

This paper analyzes the competition pattern of the panel display industry from both supply and demand sides. On the supply side, the optimization of the industry competition pattern by accelerating the withdrawal of Samsung’s production capacity is deeply discussed. Demand-side focuses on tracking global sales data and industry inventory changes. Overall, we believe that the current epidemic has a certain impact on demand, and the panel shows that prices may be under short-term pressure in April or May. But as Samsung’s exit from LCD capacity accelerates, industry inventories remain low. So once the overseas epidemic is contained and domestic demand picks up, the panel suggests prices will surge. We are firmly optimistic about the A-share panel display plate investment value, maintain the industry “optimistic” rating. Suggested attention: BOE A, TCL Technology.

Sigmaintell Research of China has released its summary of the global LCD TV panel market in the first half of 2018. Trade friction between big countries and political and economic upheaval is on the rise, while Chinese economic growth is slowing down.

In addition, the fluctuation of the exchange rate has impacted the performance of the major TV markets. Sell-in was lower than expected but the volume of shipments pushed by panel manufacturers still increased considerably compared with the same period last year.

In the first half of 2018, shipments of LCD TV panels reached 135 million units, a decrease of 3.7% compared to the second half of 2017 but an increase of 10.6% from the first half of 2017. Analysts also say that the trend to larger sizes continues to slow.

Driven by the World Cup, overseas market demand continues to strengthen, which has led to a significant increase in small and medium-size panel shipments. According to Sigmaintell, in the first half of 2018, 32" panel sell-in grew by 25% over the same period in 2017, accounting for 32% of total global LCD TV panel sales.

Sell-in of 39" - 45" sizes increased by 11% year-on-year, accounting for 24.4% of the total. In contrast, sell-in of 65" panels decreased by 4%. While the proportion of small-size products increased, the proportion of large sizes was not significantly improved. In the first half of the year, the global average size of LCD TV panels actually dropped to 43.6", a decrease of 0.1". In the second quarter of 2018, it dropped further to 43.3".

Therefore, the growth of average panel size is lower than expected, which analysts say is one of the important factors in the imbalance of supply and demand within the LCD market during the first half of the year.

As a result of their continuous expansion of production capacity, the overall competitiveness and market share of Chinese manufacturers has increased significantly. In the first half of 2018, BOE, LG and Innolux were the top-three panel makers respectively, with Samsung fourth and CSOT fifth.

In the first half of 2018, BOE shipped 25.84 million units. This year, the company"s 8.5G line in Fuqing, China reached full capacity and the world"s first 10.5G line commenced mass production.

LG shipped 23.72 million LCD TV panels in the first half of 2018, a decrease of 3.4% over the same period in 2017. However, it ranked first in terms of shipment size. The company continues to drive large-sizes and maintains a leading position in large and high-end products in sizes such as 55”, 65” and 75”.

Due to the declining profitability of LCD TV panels, LG has accelerated investment in OLED TV panels. Its OLED production line in Guangzhou, China was officially approved and its Paju P10 facility in South Korea is exclusively producing OLED TV panels. At the same time, the repurposing of 8.5G LCD capacity to OLED is also being accelerated.

Samsung is focusing on large-size, high-end products. The scale of 65" panel production continues to expand and the company also commenced mass production of 8K TV panel during the second quarter. Its overall shipments were relatively stable, ranking fourth, while the company ranked second after LG in terms of shipment by area.

CSOT"s total shipment volume reached 19.1 million in the first half, an increase of 5.6% year-on-year, ranking fifth in terms of amount and area of shipments. In the second quarter, the company"s product structure was adjusted, with output of 32” panels reduced and supply of 43” panels increased.

Affected by the capacity expansion of Chinese manufacturers, AU Optronics" market share has dropped to less than 10% and the company"s investment is relatively conservative. In the second half of this year, 8.5G capacity expansion will usher in mass production.

Among other panel makers, HKC"s 8.6G line is almost operating at full capacity. Shipments have been maintained steadily, with a focus on 32" panels. CEC"s two new 8.6G lines have begun mass production, but shipment growth is slow. Meanwhile, Sharp"s panel production line maintained high productivity.

Since the second quarter of 2017, panel prices have dropped. In the first half of this year, the TV market was not performing well and panel prices continued to decline in June, with prices coming close to cost, which caused panel factories to suffer.

Prices of 32" panels have fallen, opening up the price difference between adjacent sizes. The supply and demand imbalance in the second quarter of this year caused 32" panel prices to plummet rapidly. According to Sigmaintell, in the first half of 2018, the price of 32” panels decreased by 31%, or almost 40% compared to their peak price point in 2017.

For 39.5" - 43" sizes, promotion isn"t active and demand is weak. BOE"s 8.5G line in Fuqing, China has led to an increase in the supply of 43" panels and a substantial decline in their price. As for 49" - 50", new 8.6G lines have greatly enriched 50" panel supply resources. Price is relatively positive, even with the 49" price inversion, causing demand to shift from 49” to 50”.

55” is still the "golden child" of the large sizes. Demand continues to be strong and price declines are smaller than those of other sizes. According to Sigmaintell, in the first half of 2018, the price of 55” panels decreased by 16.1%, and nearly 30.5% compared to their peak price point in 2017.

As for 65”, prices began to fall in June 2017. Thanks in part to the smooth production of BOE"s 10.5G line, supply of 65” panels has been greatly increased. In the second quarter of 2018, 65" panel prices declined by about 25%.

Panel prices rapidly fell below total cost in the second quarter of 2018, causing panel makers to face severe profitability challenges. However, through positive price strategies, panel manufacturers have increased shipment growth and reduced inventory.

Panel makers will have the opportunity to achieve phased business improvement through strategic adjustment but with the continued release of new production capacity, they will face serious competition in the future.

Sigmaintell says panel manufacturers should actively seek to reduce costs, but with the tight supply of key components such as ICs, the scope for product cost reduction is limited. Therefore, it is more important to continuously upgrade technology to enhance overall competitiveness and reduce risk.

LCD panel market is expecting several new large generation fabs in 2018. BOE has launched the world’s first Gen 10.5 fab, while CEC-CHOT’s Gen 8.6 fab and Gen 8.6+ fab of CEC-Panda Chengdu will also go into operation this year. WitsView, a division of TrendForce, says that there was a 20-40% downward correction in TV panel prices during 2017. While the price decline in the TV panel market will be easing in this year"s first half, this first quarter will still see the price trend on a gradual downward slope.

Falling panel prices will spur promotions in the end product market. Therefore, stock-up demand from TV brands will be warmer in this year’s second half compared with the second half of 2017. The supply and demand of TV panels are also expected to reach a more balanced state. Our latest analysis indicates that the risk of serious oversupply in the TV panel market will most likely to happen later in 2019.

Anita Wang, senior research manager of WitsView, points out that the new fab will have limited input in early stages, and will need time to improve field rate and production capacity. Therefore, Wang estimates that they will only contribute to 3% of the global glass input for large-size LCD panels. And the figure is expected to raise to 6-8% in 2019.

Going into operation on December 20th, 2017, BOE’s Gen 10.5 fab in Hefei is expected to enter mass production in March 2018. The major products will be large-size TV panels of 65" UHD 60Hz and 75" UHD 60Hz, intensifying the competition in large-size (65" or greater) TV panel market.

In the production of 65" TV panels, for instance, current Gen 6 fab cuts per glass substrate into 2 panels, while Gen 8.5 fab cuts into 3. In Gen 10.5 fab, however, the number rises to 8, increasing the productivity of 65" TV panels significantly.

WitsView forecasts that BOE’s Gen 10.5 fab will target at more than 2 million pieces for the production of 65" panels, but whether this goal can be achieved still depends on the improvement in yield rate. The Gen 10.5 fab will not have large-scale influences on the overall supply in the industry this year, but BOE will impact the market in 2019 with its shipments expected to reach 3 to 4 million pieces. In 2020, BOE is even predicted to surpass panel makers in South Korea and record the highest shipments for 65" panels, with its market share reaching around 37%. In comparison, the market share of Taiwanese panel makers for 65" panels will drop to 18% in 2020 without any capacity expansion.

Increases in both new-generation fabs’ yield rate and production capacity will create a reshaping of the LCD TV panel market through to 2019, says research company WitsView.

BOE’s fab in Hefei is expected to enter mass production by March 2018. The major products will be large-size TV panels of 65” Ultra HD 60Hz and 75” Ultra HD 60Hz, intensifying, said the analyst, competition in large-size TV panel market. In the production of 65” TV panels, for instance, current Gen 6 fab cuts per glass substrate into 2 panels, while Gen 8.5 fab cuts into 3. In Gen 10.5 fab, however, the number rises to 8, increasing the productivity of 65” TV panels significantly.

Ultimately, WitsView says that falling panel prices will spur promotions in the end product market and that a stock-up demand from TV brands will be warmer in this year’s second half compared with the second half of 2017. The supply and demand of TV panels are also expected to reach a more balanced state. The research indicates that the risk of serious oversupply in the TV panel market will most likely to happen later in 2019.

Anita Wang, senior research manager of WitsView, noted out that the new fab will have limited input in early stages, and will need time to improve field rate and production capacity. She estimates that they will only contribute to 3% of the global glass input for large-size LCD panels. And the figure is expected to raise to 6-8% in 2019.

WitsView forecasts that even though BOE’s Gen 10.5 fab will target at more than two million pieces for the production of 65” panels, it is questionable whether this goal can be achieved as it still depends on the improvement in yield rate. It believes that the Gen 10.5 fab will not have large-scale influences on the overall supply in the industry this year, but that BOE will impact the market in 2019 with its shipments expected to reach 3–4 million pieces. WitsView predicts that by 2020 BOE is will surpass panel makers in South Korea and record the highest shipments for 65” panels, with its market share reaching around 37%. In comparison, the market share of Taiwanese panel makers for 65” panels is projected to drop to 18% in 2020 without any capacity expansion.

On August 31, 2011, Sony, Toshiba, and Hitachi agreed to a merger of their respective small-to-medium-sized LCD businesses, supported by an investment of two hundred billion yen from INCJ. Soon after, INCJ and Panasonic also began talks on the acquisition of one of Panasonic"s factories.

JDI had accumulated consecutive losses since its IPO, a restructuring plan was announced in 2017, including closing down a production line in Japan and layoffs of approximately a third of its workforce.

A newly-created entity INCJ, Ltd. had become the largest shareholder of JDI with 25,29 % of total shares since September 21, 2018 as a result of a corporate split of the old INCJ.

Due to the financial trouble caused by its late decision to manufacture OLED displays and the loan from Apple, the company"s OLED affiliate, JOLED, has not yet been able to compete with other manufacturers, whilst more than half of JDI"s revenue still came from the shrinking IPS LCD panel sales to Apple.

In April 2020, in accordance with the talks held in December, JDI began to sell LCD production equipment valued at US$200 million to Apple, with plans to sell the real estate of the Hakusan plant to Sharp. This will allow JDI to focus on its remaining product demand and factories. The sales have been completed by October.

In July 2020, the CEO of JDI revealed the company"s plan to start mass production of OLED display panels for smartphones "as early as 2022" with a novel manufacturing technology, adding that it would require new funding.

Its "Pixel Eyes" technology incorporates the touch function into the LCD panel itself; combined with the company"s transparent display technology, a transparent fingerprint reader that could be featured in smartphones was announced in 2018.

For reflective LCDs without backlighting, JDI has developed an addressing technique using a thin-film memory device SRAM in addition to the conventional TFT for each pixel, so that a still image can be stored consuming a low amount of energy.

As a Zhongguancun enterprise, BOE has always adhered to technology-driven innovation. According to statistics, BOE"s 2018 shipments of LCD TV panels exceeded that of,LG Display Co, one of the world"s biggest manufacturers of display panels used in smartphones and televisions, ranking first in the world that year.

"The display shipments of BOE increased by 24 percent year-on-year in 2018, and its dispatch area increased by 45 percent year-on-year, which is the highest growth among the top five panel makers in the world," According to Sigmaintell Consulting analysts, who added that BOE achieved remarkable results in 2018: the world"s first 10.5 generation TFT-LCD mass production line was put into operation, and its TV panel production capacity increased by over 40 percent.

Meanwhile, BOE"s product structure continues to optimize production of large TV displays. Screens of 55, 65 and 75 inches increased sharply, and BOE"s market share of 75-inch TV displays tops in the world.

Global shipments of LCD TV panels in the first quarter of 2018 [Photo provided to chinadaily.com.cn]BOE accelerated its technology upgrading and achieved a new breakthrough in liquid crystal display technology in 2018. By applying megapixel partitioning technology, BOE 4K display achieved a 100,000-level ultra-high dynamic contrast ratio, with a color depth up to 12bits, so that the LCD display perfectly shows the ultra high definition display effect.

Recently, the US patent service agency IFI Claims released the 2018 US statistics report on patent authorization. BOE"s global ranking had jumped to 17th, with patents granted in America reaching 1,634, an increase of 16 percent. BOE is now the fastest-growing company among the TOP 20 enterprises listed by IFI Claims.

The 2018 US statistics report on patent authorization released by IFI Claims. [Source: IFI CLAIMS official website]Innovation is the only path on which companies can survive and succeed. Since its founding, BOE has always maintained its respect for technology and innovation and has ranked first in the industry for patent applications for consecutive years.

In 2018, BOE added 9,958 new patent applications, 90 percent of them invention patents and 38 percent overseas patents covering the United States, Europe, Japan, South Korea and other countries and regions. The total number of patents held by the company exceeds 70,000.

The "4317 full-spine flat-panel detector" is the world"s first and largest flat-panel detector for full-body scanning. It takes a one-time shot to obtain a complete human spine image, which avoids the patient"s exposure to accumulated X-ray doses and greatly reduces radiation damage.

Over a decade ago, due to the lack of core technologies in the field of semiconductor displays, China"s electronic information industry was shrouded in the shadow of the "lack of LCD screens", and was even unable to independently manufacture a complete LCD TV.

Acquisition of Hyundai Electronics" LCD panel businesses gave Chinese semiconductor companies a chance to break through technological limitations. [Photo provided to chinadaily.com.cn]A group of semiconductor companies like BOE seized the opportunity to acquire Hyundai Electronics" LCD panel businesses. After digesting, absorbing and re-innovating, the companies mastered liquid crystal display technology and ended the dependence on imports in the Chinese semiconductor and display industries.

TOKYO, Oct 1 (Reuters) - Toshiba Corpsaid on Friday it is scrapping plans to mass-produce organic electroluminescence (OLED) panels and will focus more on mid-to-small sized LCD panels amid strong demand.

OLED panels were touted as the next-generation technology in flat panels but saw a slow take-off due to competition with other technologies and the improved quality of LCD panels. The global OLED display market is currently dominated by Samsung Mobile Display.

“The plan (for mass-production) is currently frozen. We’ll review the production plan again from scratch,” Toshiba Mobile Display spokesman Masahiro Kume said.

Toshiba Mobile Display invested some 16 billion yen ($197 million) in 2008, when it was a joint venture between Toshiba and Panasonic Corp, on installing an OLED production line in Japan, but the start of mass-production was delayed.

The company will transfer the few dozen engineers involved in research and development to the LCD panel division, the Nikkei business daily reported earlier.

Ms.Josey

Ms.Josey

Ms.Josey

Ms.Josey